In my previous Ecosystm Insights, I covered how to choose the right database for the success of any application or project. Often organisations select cloud-based databases for the scalability, flexibility, and cost-effectiveness.

Here’s a look at some prominent cloud-based databases and guidance on the right cloud-based database for your organisational needs.

Click here to download ‘Databases Demystified. Cloud-Based Databases’ as a PDF.

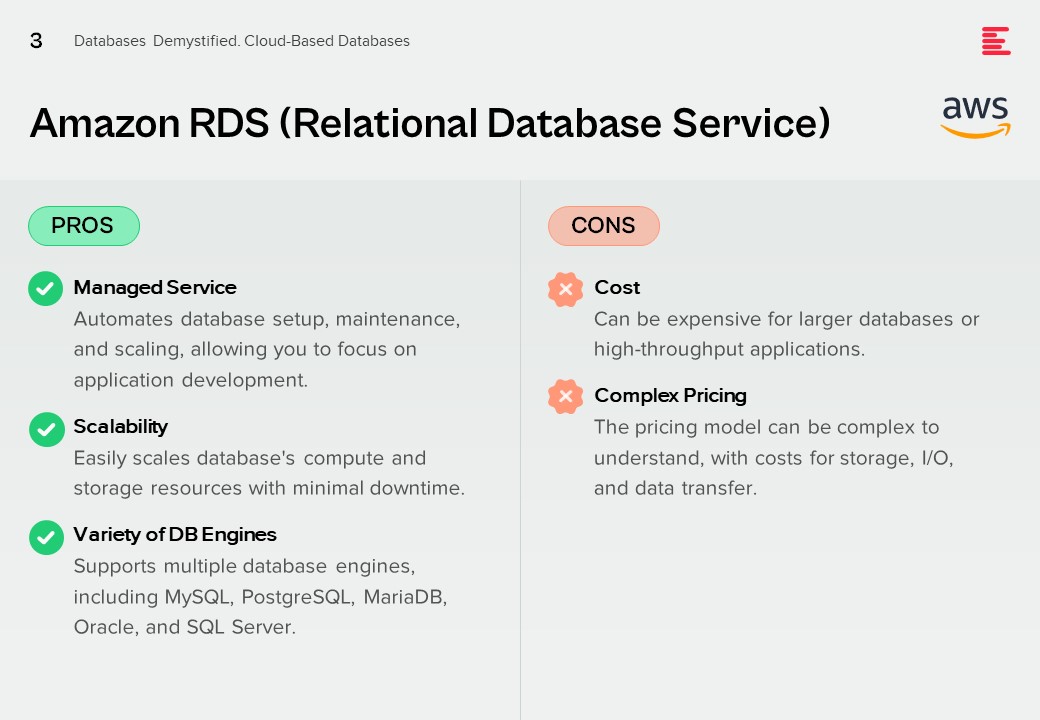

Amazon RDS (Relational Database Service)

Pros.

Managed Service. Automates database setup, maintenance, and scaling, allowing you to focus on application development.

Scalability. Easily scales database’s compute and storage resources with minimal downtime.

Variety of DB Engines. Supports multiple database engines, including MySQL, PostgreSQL, MariaDB, Oracle, and SQL Server.

Cons.

Cost. Can be expensive for larger databases or high-throughput applications.

Complex Pricing. The pricing model can be complex to understand, with costs for storage, I/O, and data transfer.

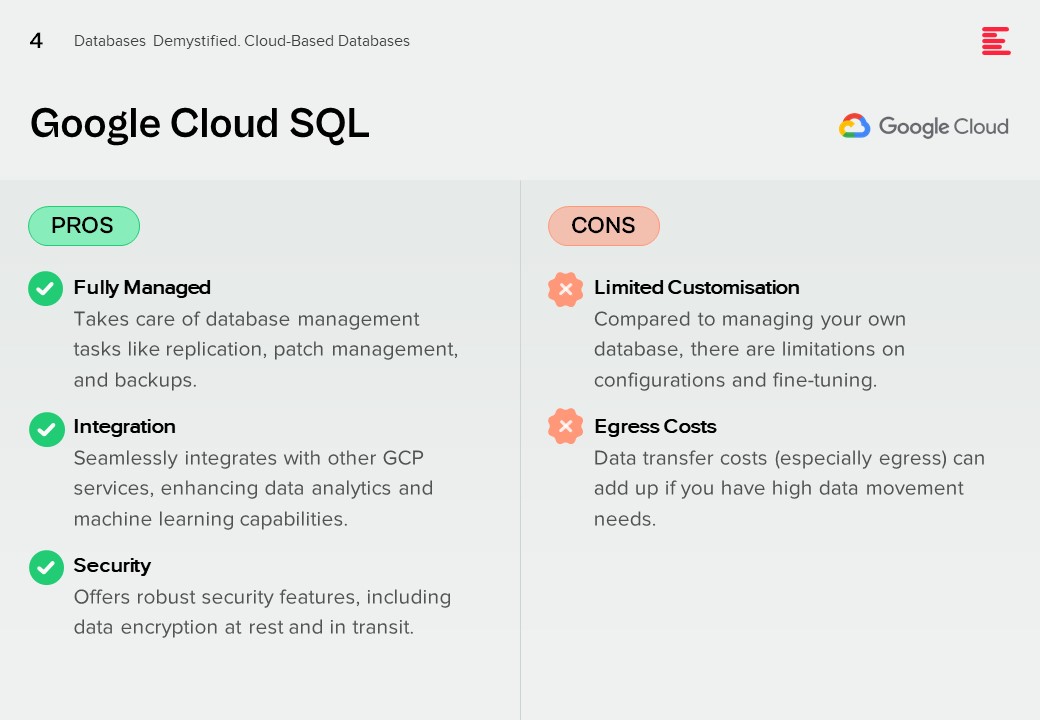

Google Cloud SQL

Pros.

Fully Managed. Takes care of database management tasks like replication, patch management, and backups.

Integration. Seamlessly integrates with other GCP services, enhancing data analytics and machine learning capabilities.

Security. Offers robust security features, including data encryption at rest and in transit.

Cons.

Limited Customisation. Compared to managing your own database, there are limitations on configurations and fine-tuning.

Egress Costs. Data transfer costs (especially egress) can add up if you have high data movement needs.

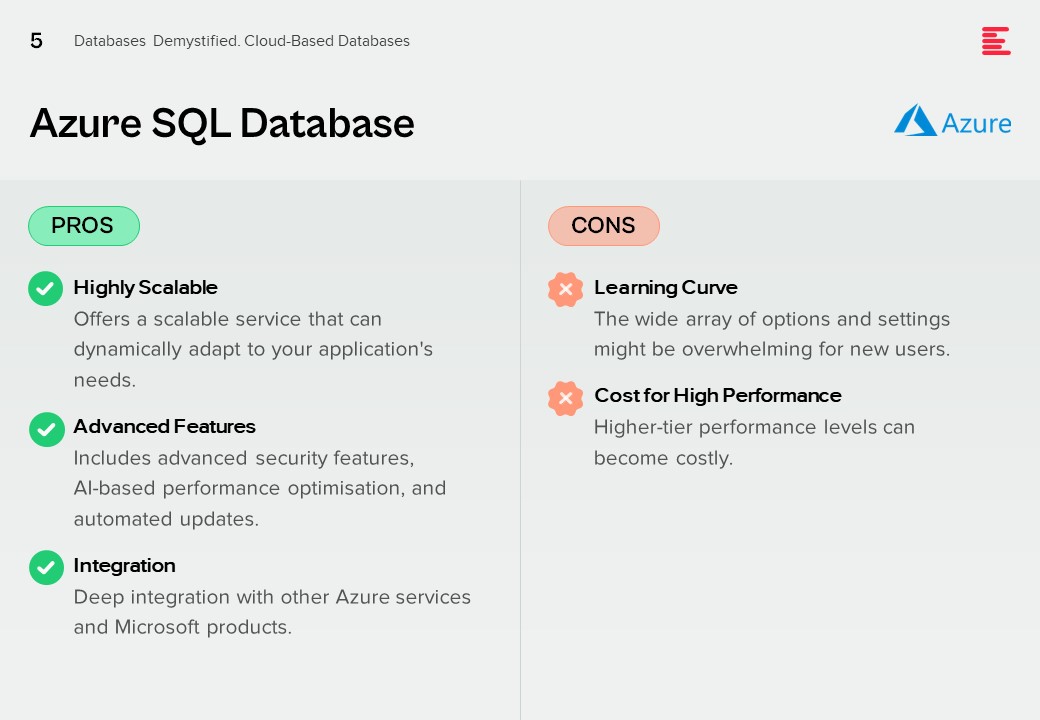

Azure SQL Database

Pros.

Highly Scalable. Offers a scalable service that can dynamically adapt to your application’s needs.

Advanced Features. Includes advanced security features, AI-based performance optimisation, and automated updates.

Integration. Deep integration with other Azure services and Microsoft products.

Cons.

Learning Curve. The wide array of options and settings might be overwhelming for new users.

Cost for High Performance. Higher-tier performance levels can become costly.

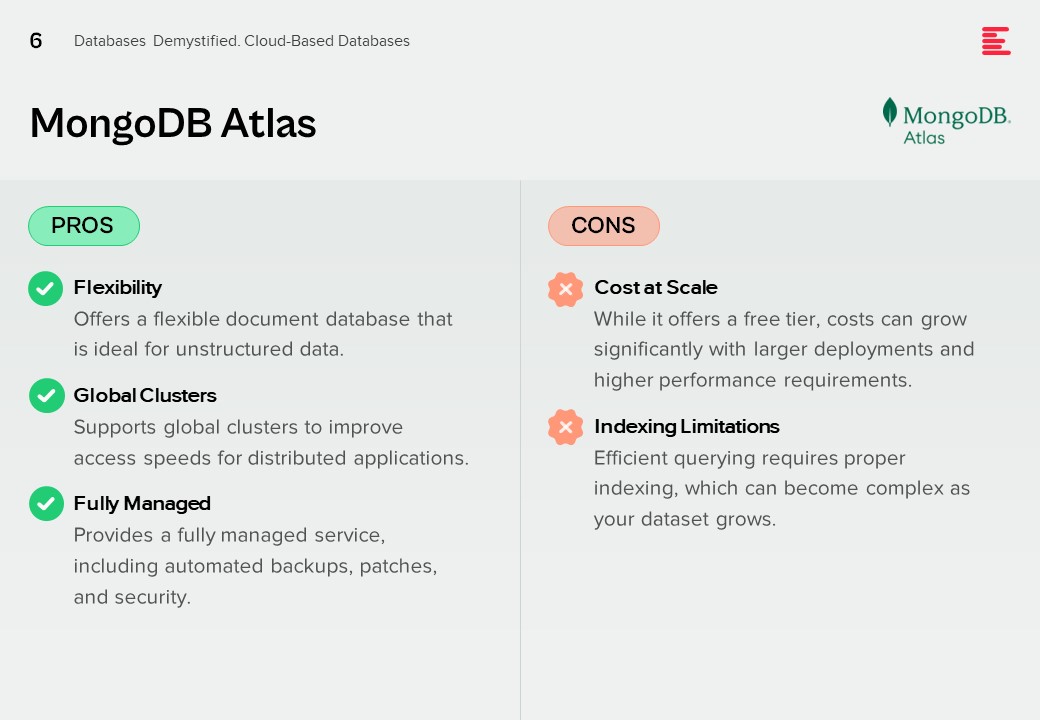

MongoDB Atlas

Pros.

Flexibility. Offers a flexible document database that is ideal for unstructured data.

Global Clusters. Supports global clusters to improve access speeds for distributed applications.

Fully Managed. Provides a fully managed service, including automated backups, patches, and security.

Cons.

Cost at Scale. While it offers a free tier, costs can grow significantly with larger deployments and higher performance requirements.

Indexing Limitations. Efficient querying requires proper indexing, which can become complex as your dataset grows.

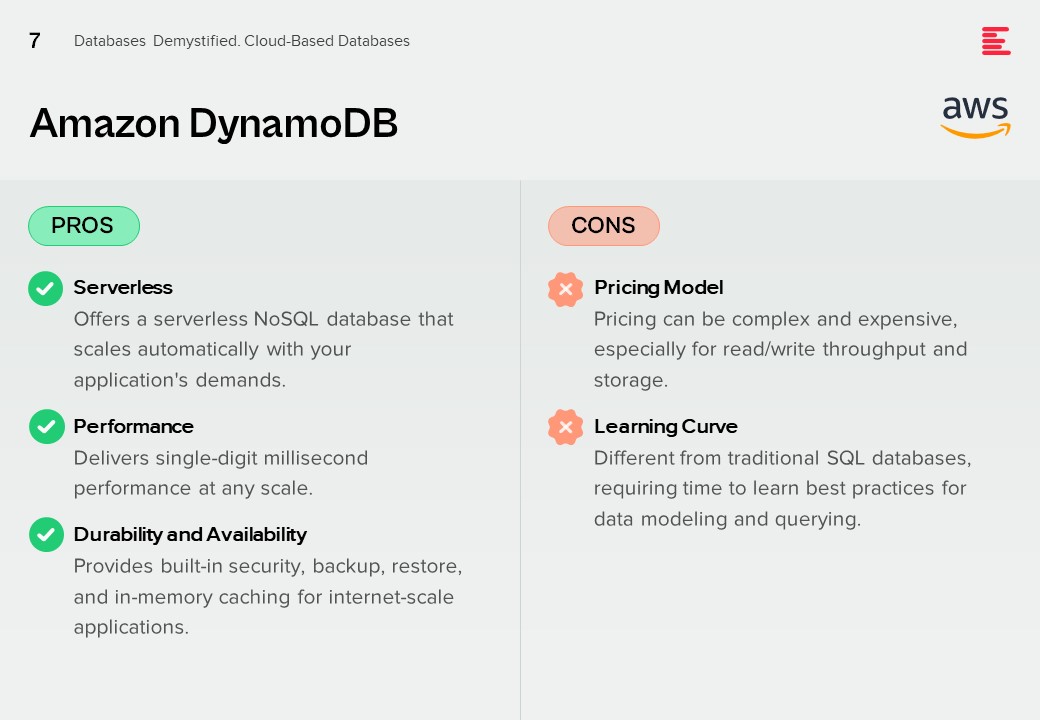

Amazon DynamoDB

Pros.

Serverless. Offers a serverless NoSQL database that scales automatically with your application’s demands.

Performance. Delivers single-digit millisecond performance at any scale.

Durability and Availability. Provides built-in security, backup, restore, and in-memory caching for internet-scale applications.

Cons.

Pricing Model. Pricing can be complex and expensive, especially for read/write throughput and storage.

Learning Curve. Different from traditional SQL databases, requiring time to learn best practices for data modeling and querying.

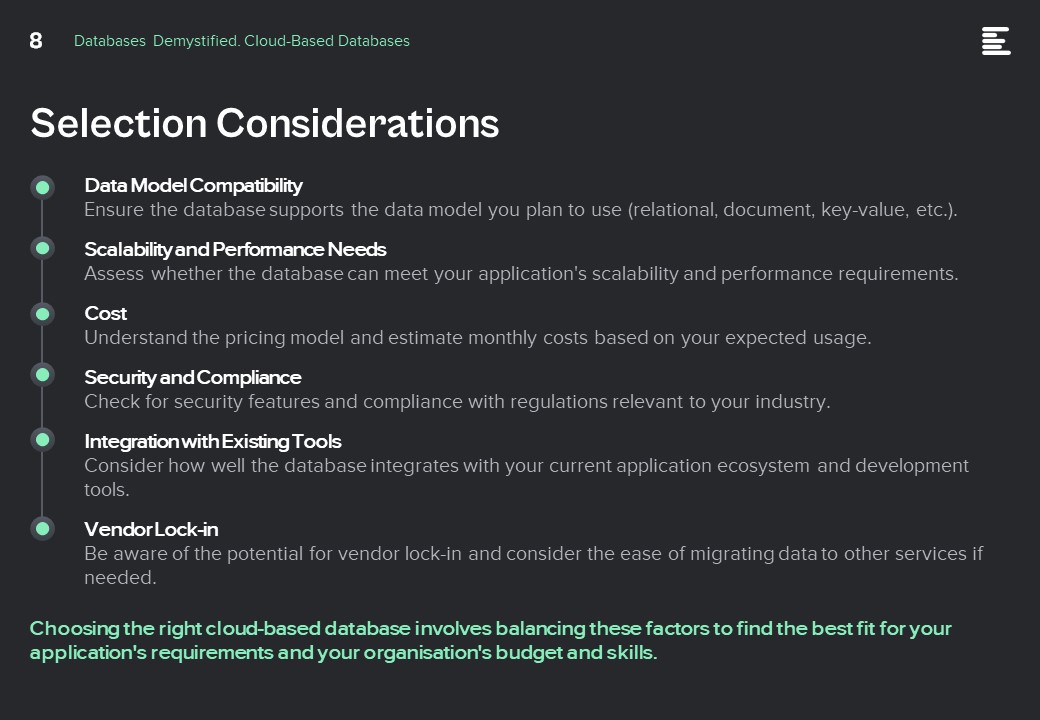

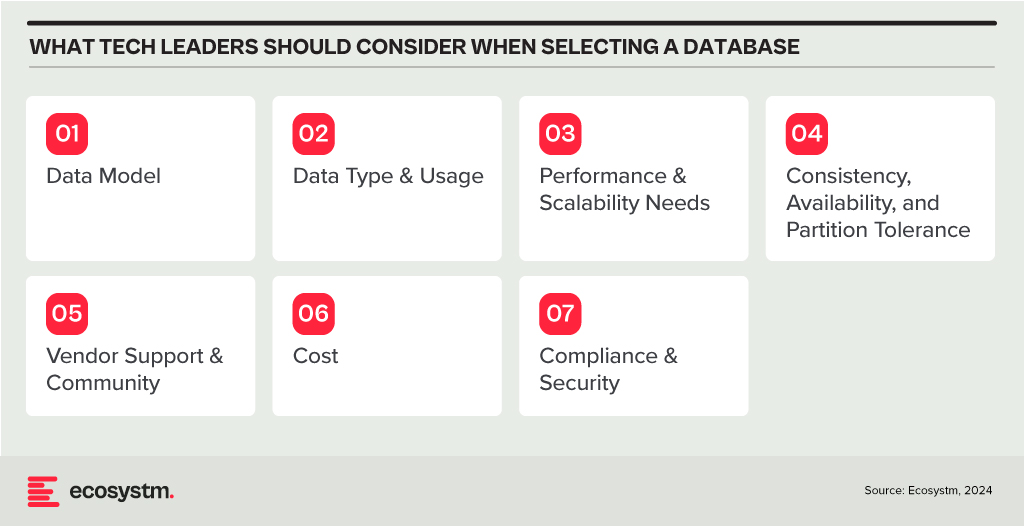

Selection Considerations

Data Model Compatibility. Ensure the database supports the data model you plan to use (relational, document, key-value, etc.).

Scalability and Performance Needs. Assess whether the database can meet your application’s scalability and performance requirements.

Cost. Understand the pricing model and estimate monthly costs based on your expected usage.

Security and Compliance. Check for security features and compliance with regulations relevant to your industry.

Integration with Existing Tools. Consider how well the database integrates with your current application ecosystem and development tools.

Vendor Lock-in. Be aware of the potential for vendor lock-in and consider the ease of migrating data to other services if needed.

Choosing the right cloud-based database involves balancing these factors to find the best fit for your application’s requirements and your organisation’s budget and skills.

In my last Ecosystm Insights, I outlined various database options available to you. The challenge lies in selecting the right one. Selecting the right database is crucial for the success of any application or project. It involves understanding your data, the operations you’ll perform, scalability requirements, and more. Here is a guide that will walk you through key considerations and steps to choose the most suitable database from the list I shared last week.

Understand Your Data Model

Relational (RDBMS) vs. NoSQL. Choose RDBMS if your data is structured and relational, requiring complex queries and transactions with ACID (Atomicity, Consistency, Isolation, Durability) properties. Opt for NoSQL if you have unstructured or semi-structured data, need to scale horizontally, or require flexibility in your schema design.

Consider the Data Type and Usage

Document Databases are ideal for storing, retrieving, and managing document-oriented information. They’re great for content management systems, ecommerce applications, and handling semi-structured data like JSON, XML.

Key-Value Stores shine in scenarios where quick access to data is needed through a key. They’re perfect for caching and storing user sessions, configurations, or any scenario where the lookup is based on a unique key.

Wide-Column Stores offer flexibility and scalability for storing and querying large volumes of data across many servers, suitable for big data applications, real-time analytics, and high-speed transactions.

Graph Databases are designed for data intensely connected through relationships, ideal for social networks, recommendation engines, and fraud detection systems where relationships between data points are key.

Time-Series Databases are optimised for storing and querying sequential data points indexed in time order. Use them for monitoring systems, IoT applications, and financial trading systems where time-stamped data is critical.

Spatial Databases support spatial data types and queries, making them suitable for geographic information systems (GIS), location-based services, and applications requiring spatial indexing and querying capabilities.

Assess Performance and Scalability Needs

In-Memory Databases like Redis offer high throughput and low latency for scenarios requiring rapid access to data, such as caching, session storage, and real-time analytics.

Distributed Databases like Cassandra or CouchDB are designed to run across multiple machines, offering high availability, fault tolerance, and scalability for applications with global reach and massive scale.

Evaluate Consistency, Availability, and Partition Tolerance (CAP Theorem)

Understand the trade-offs between consistency, availability, and partition tolerance. For example, if your application requires strong consistency, consider databases that prioritise consistency and partition tolerance (CP) like MongoDB or relational databases. If availability is paramount, look towards databases that offer availability and partition tolerance (AP) like Cassandra or CouchDB.

Other Considerations

Check for Vendor Support and Community. Evaluate the support and stability offered by vendors or open-source communities. Established products like Oracle Database, Microsoft SQL Server, and open-source options like PostgreSQL and MongoDB have robust support and active communities.

Cost. Consider both initial and long-term costs, including licenses, hardware, maintenance, and scalability. Open-source databases can reduce upfront costs, but ensure you account for support and operational expenses.

Compliance and Security. Ensure the database complies with relevant regulations (GDPR, HIPAA, etc.) and offers robust security features to protect sensitive data.

Try Before You Decide. Prototype your application with shortlisted databases to evaluate their performance, ease of use, and compatibility with your application’s requirements.

Conclusion

Selecting the right database is a strategic decision that impacts your application’s functionality, performance, and scalability. By carefully considering your data model, type of data, performance needs, and other factors like cost, support, and security, you can identify the database that best fits your project’s needs. Always stay informed about the latest developments in database technologies to make educated decisions as your requirements evolve.

Banks, insurers, and other financial services organisations in Asia Pacific have plenty of tech challenges and opportunities including cybersecurity and data privacy management; adapting to tech and customer demands, AI and ML integration; use of big data for personalisation; and regulatory compliance across business functions and transformation journeys.

Modernisation Projects are Back on the Table

An emerging tech challenge lies in modernising, replacing, or retiring legacy platforms and systems. Many banks still rely on outdated core systems, hindering agility, innovation, and personalised customer experiences. Migrating to modern, cloud-based systems presents challenges due to complexity, cost, and potential disruptions. Insurers are evaluating key platforms amid evolving customer needs and business models; ERP and HCM systems are up for renewal; data warehouses are transforming for the AI era; even CRM and other CX platforms are being modernised as older customer data stores and models become obsolete.

For the past five years, many financial services organisations in the region have sidelined large legacy modernisation projects, opting instead to make incremental transformations around their core systems. However, it is becoming critical for them to take action to secure their long-term survival and success.

Benefits of legacy modernisation include:

- Improved operational efficiency and agility

- Enhanced customer experience and satisfaction

- Increased innovation and competitive advantage

- Reduced security risks and compliance costs

- Preparation for future technologies

However, legacy modernisation and migration initiatives carry significant risks. For instance, TSB faced a USD 62M fine due to a failed mainframe migration, resulting in severe disruptions to branch operations and core banking functions like telephone, online, and mobile banking. The migration failure led to 225,492 complaints between 2018 and 2019, affecting all 550 branches and required TSB to pay more than USD 25M to customers through a redress program.

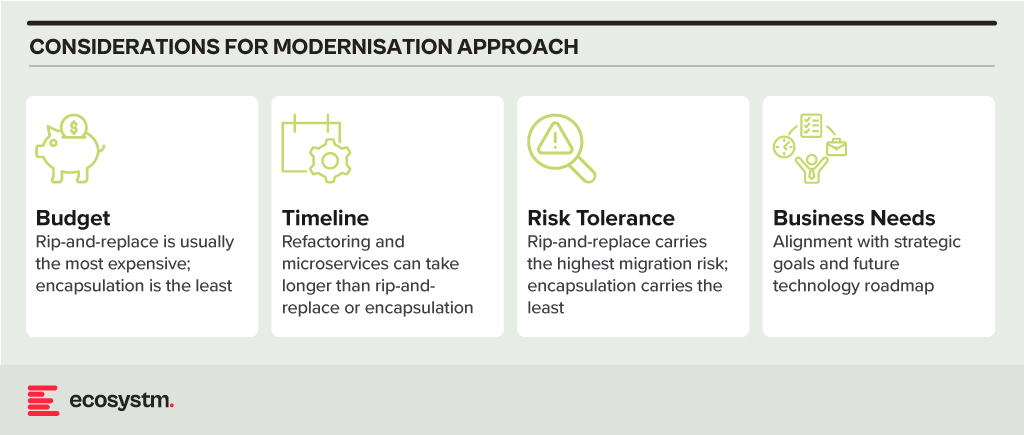

Modernisation Options

- Rip and Replace. Replacing the entire legacy system with a modern, cloud-based solution. While offering a clean slate and faster time to value, it’s expensive, disruptive, and carries migration risks.

- Refactoring. Rewriting key components of the legacy system with modern languages and architectures. It’s less disruptive than rip-and-replace but requires skilled developers and can still be time-consuming.

- Encapsulation. Wrapping the legacy system with a modern API layer, allowing integration with newer applications and tools. It’s quicker and cheaper than other options but doesn’t fully address underlying limitations.

- Microservices-based Modernisation. Breaking down the legacy system into smaller, independent services that can be individually modernised over time. It offers flexibility and agility but requires careful planning and execution.

Financial Systems on the Block for Legacy Modernisation

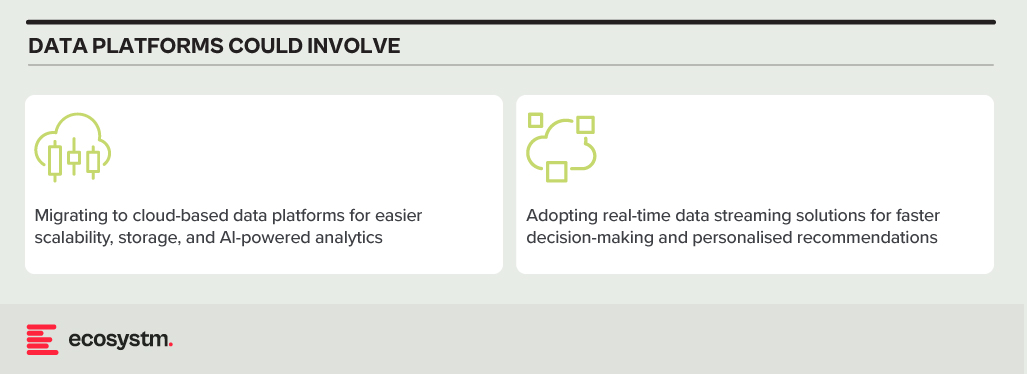

Data Analytics Platforms. Harnessing customer data for insights and targeted offerings is vital. Legacy data warehouses often struggle with real-time data processing and advanced analytics.

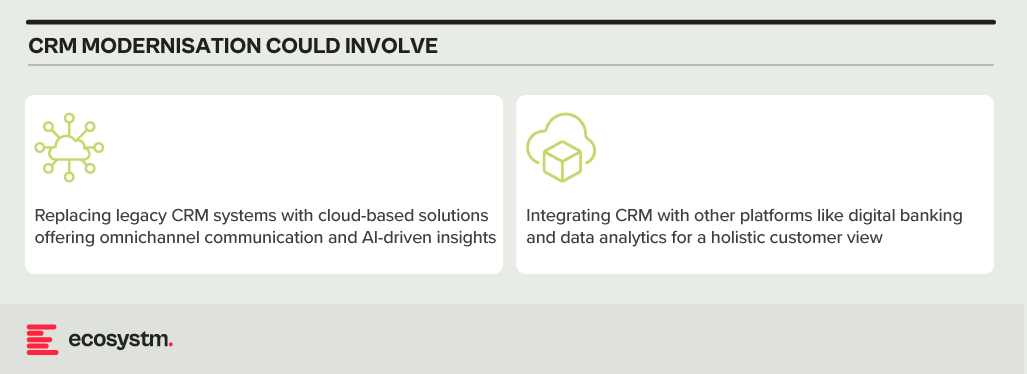

CRM Systems. Effective customer interactions require integrated CRM platforms. Outdated systems might hinder communication, personalisation, and cross-selling opportunities.

Payment Processing Systems. Legacy systems might lack support for real-time secure transactions, mobile payments, and cross-border transactions.

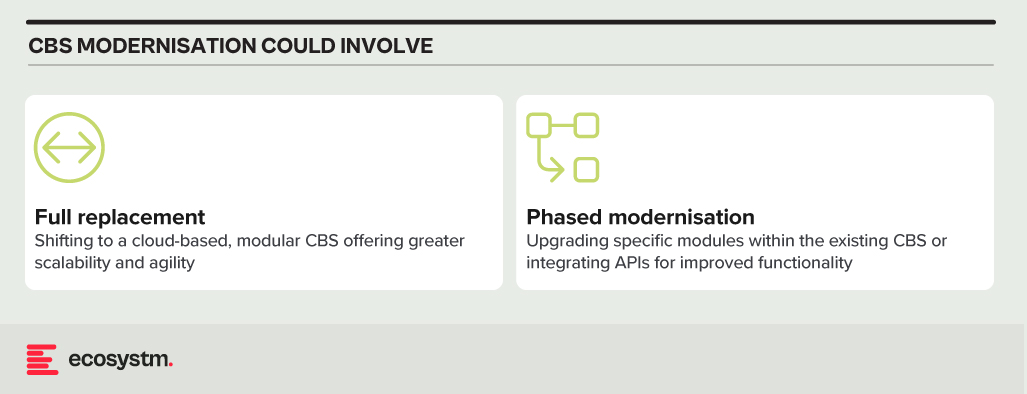

Core Banking Systems (CBS). The central nervous system of any bank, handling account management, transactions, and loan processing. Many Asia Pacific banks rely on aging, monolithic CBS with limited digital capabilities.

Digital Banking Platforms. While several Asia Pacific banks provide basic online banking, genuine digital transformation requires mobile-first apps with features such as instant payments, personalised financial management tools, and seamless third-party service integration.

Modernising Technical Approaches and Architectures

Numerous technical factors need to be addressed during modernisation, with decisions needing to be made upfront. Questions around data migration, testing and QA, change management, data security and development methodology (agile, waterfall or hybrid) need consideration.

Best practices in legacy migration have taught some lessons.

Adopt a data fabric platform. Many organisations find that centralising all data into a single warehouse or platform rarely justifies the time and effort invested. Businesses continually generate new data, adding sources, and updating systems. Managing data where it resides might seem complex initially. However, in the mid to longer term, this approach offers clearer benefits as it reduces the likelihood of data discrepancies, obsolescence, and governance challenges.

Focus modernisation on the customer metrics and journeys that matter. Legacy modernisation need not be an all-or-nothing initiative. While systems like mainframes may require complete replacement, even some mainframe-based software can be partially modernised to enable services for external applications and processes. Assess the potential of modernising components of existing systems rather than opting for a complete overhaul of legacy applications.

Embrace the cloud and SaaS. With the growing network of hyperscaler cloud locations and data centres, there’s likely to be a solution that enables organisations to operate in the cloud while meeting data residency requirements. Even if not available now, it could align with the timeline of a multi-year legacy modernisation project. Whenever feasible, prioritise SaaS over cloud-hosted applications to streamline management, reduce overhead, and mitigate risk.

Build for customisation for local and regional needs. Many legacy applications are highly customised, leading to inflexibility, high management costs, and complexity in integration. Today, software providers advocate minimising configuration and customisation, opting for “out-of-the-box” solutions with room for localisation. The operations in different countries may require reconfiguration due to varying regulations and competitive pressures. Architecting applications to isolate these configurations simplifies system management, facilitating continuous improvement as new services are introduced by platform providers or ISV partners.

Explore the opportunity for emerging technologies. Emerging technologies, notably AI, can significantly enhance the speed and value of new systems. In the near future, AI will automate much of the work in data migration and systems integration, reducing the need for human involvement. When humans are required, low-code or no-code tools can expedite development. Private 5G services may eliminate the need for new network builds in branches or offices. AIOps and Observability can improve system uptime at lower costs. Considering these capabilities in platform decisions and understanding the ecosystem of partners and providers can accelerate modernisation journeys and deliver value faster.

Don’t Let Analysis Paralysis Slow Down Your Journey!

Yes, there are a lot of decisions that need to be made; and yes, there is much at stake if things go wrong! However, there’s a greater risk in not taking action. Maintaining a laser-focus on the customer and business outcomes that need to be achieved will help align many decisions. Keeping the customer experience as the guiding light ensures organisations are always moving in the right direction.

AI has become a business necessity today, catalysing innovation, efficiency, and growth by transforming extensive data into actionable insights, automating tasks, improving decision-making, boosting productivity, and enabling the creation of new products and services.

Generative AI stole the limelight in 2023 given its remarkable advancements and potential to automate various cognitive processes. However, now the real opportunity lies in leveraging this increased focus and attention to shine the AI lens on all business processes and capabilities. As organisations grasp the potential for productivity enhancements, accelerated operations, improved customer outcomes, and enhanced business performance, investment in AI capabilities is expected to surge.

In this eBook, Ecosystm VP Research Tim Sheedy and Vinod Bijlani and Aman Deep from HPE APAC share their insights on why it is crucial to establish tailored AI capabilities within the organisation.

“AI Guardrails” are often used as a method to not only get AI programs on track, but also as a way to accelerate AI investments. Projects and programs that fall within the guardrails should be easy to approve, govern, and manage – whereas those outside of the guardrails require further review by a governance team or approval body. The concept of guardrails is familiar to many tech businesses and are often applied in areas such as cybersecurity, digital initiatives, data analytics, governance, and management.

While guidance on implementing guardrails is common, organisations often leave the task of defining their specifics, including their components and functionalities, to their AI and data teams. To assist with this, Ecosystm has surveyed some leading AI users among our customers to get their insights on the guardrails that can provide added value.

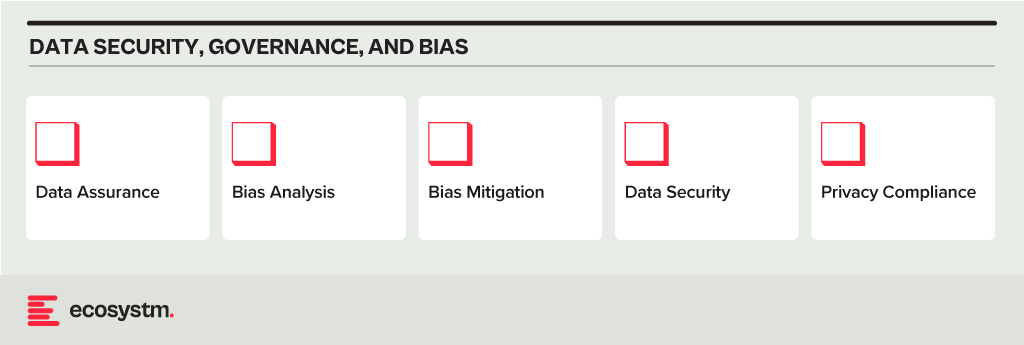

Data Security, Governance, and Bias

- Data Assurance. Has the organisation implemented robust data collection and processing procedures to ensure data accuracy, completeness, and relevance for the purpose of the AI model? This includes addressing issues like missing values, inconsistencies, and outliers.

- Bias Analysis. Does the organisation analyse training data for potential biases – demographic, cultural and so on – that could lead to unfair or discriminatory outputs?

- Bias Mitigation. Is the organisation implementing techniques like debiasing algorithms and diverse data augmentation to mitigate bias in model training?

- Data Security. Does the organisation use strong data security measures to protect sensitive information used in training and running AI models?

- Privacy Compliance. Is the AI opportunity compliant with relevant data privacy regulations (country and industry-specific as well as international standards) when collecting, storing, and utilising data?

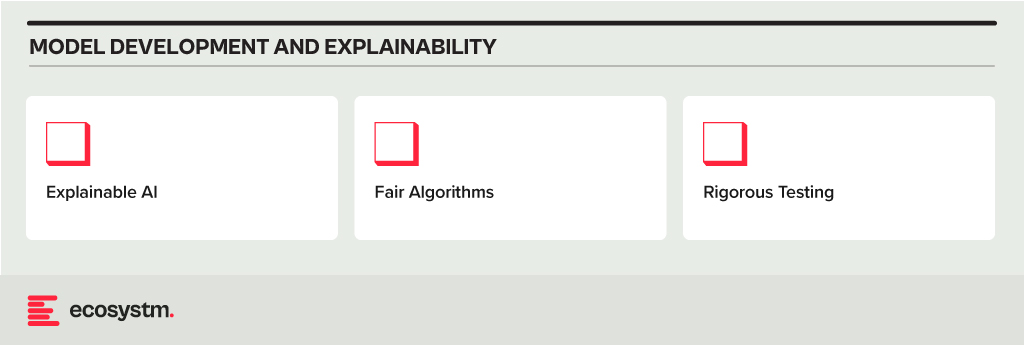

Model Development and Explainability

- Explainable AI. Does the model use explainable AI (XAI) techniques to understand and explain how AI models reach their decisions, fostering trust and transparency?

- Fair Algorithms. Are algorithms and models designed with fairness in mind, considering factors like equal opportunity and non-discrimination?

- Rigorous Testing. Does the organisation conduct thorough testing and validation of AI models before deployment, ensuring they perform as intended, are robust to unexpected inputs, and avoid generating harmful outputs?

AI Deployment and Monitoring

- Oversight Accountability. Has the organisation established clear roles and responsibilities for human oversight throughout the AI lifecycle, ensuring human control over critical decisions and mitigation of potential harm?

- Continuous Monitoring. Are there mechanisms to continuously monitor AI systems for performance, bias drift, and unintended consequences, addressing any issues promptly?

- Robust Safety. Can the organisation ensure AI systems are robust and safe, able to handle errors or unexpected situations without causing harm? This includes thorough testing and validation of AI models under diverse conditions before deployment.

- Transparency Disclosure. Is the organisation transparent with stakeholders about AI use, including its limitations, potential risks, and how decisions made by the system are reached?

Other AI Considerations

- Ethical Guidelines. Has the organisation developed and adhered to ethical principles for AI development and use, considering areas like privacy, fairness, accountability, and transparency?

- Legal Compliance. Has the organisation created mechanisms to stay updated on and compliant with relevant legal and regulatory frameworks governing AI development and deployment?

- Public Engagement. What mechanisms are there in place to encourage open discussion and engage with the public regarding the use of AI, addressing concerns and building trust?

- Social Responsibility. Has the organisation considered the environmental and social impact of AI systems, including energy consumption, ecological footprint, and potential societal consequences?

Implementing these guardrails requires a comprehensive approach that includes policy formulation, technical measures, and ongoing oversight. It might take a little longer to set up this capability, but in the mid to longer term, it will allow organisations to accelerate AI implementations and drive a culture of responsible AI use and deployment.

The tech industry tends to move in waves, driven by the significant, disruptive changes in technology, such as cloud and smartphones. Sometimes, it is driven by external events that bring tech buyers into sync – such as Y2K and the more recent pandemic. Some tech providers, such as SAP and Microsoft, are big enough to create their own industry waves. The two primary factors shaping the current tech landscape are AI and the consequential layoffs triggered by AI advancements.

While many of the AI startups have been around for over five years, this will be the year they emerge as legitimate solutions providers to organisations. Amidst the acceleration of AI-driven layoffs, individuals from these startups will go on to start new companies, creating the next round of startups that will add value to businesses in the future.

Tech Sourcing Strategies Need to Change

The increase in startups implies a change in the way businesses manage and source their tech solutions. Many organisations are trying to reduce tech debt, by typically consolidating the number of providers and tech platforms. However, leveraging the numerous AI capabilities may mean looking beyond current providers towards some of the many AI startups that are emerging in the region and globally.

The ripple effect of these decisions is significant. If organisations opt to enhance the complexity of their technology architecture and increase the number of vendors under management, the business case must be watertight. There will be less of the trial-and-error approach towards AI from 2023, with a heightened emphasis on clear and measurable value.

AI Startups Worth Monitoring

Here is a selection of AI startups that are already starting to make waves across Asia Pacific and the globe.

- ADVANCE.AI provides digital transformation, fraud prevention, and process automation solutions for enterprise clients. The company offers services in security and compliance, digital identity verification, and biometric solutions. They partner with over 1,000 enterprise clients across Southeast Asia and India across sectors, such as Banking, Fintech, Retail, and eCommerce.

- Megvii is a technology company based in China that specialises in AI, particularly deep learning. The company offers full-stack solutions integrating algorithms, software, hardware, and AI-empowered IoT devices. Products include facial recognition software, image recognition, and deep learning technology for applications such as consumer IoT, city IoT, and supply chain IoT.

- I’mCloud is based in South Korea and specialises in AI, big data, and cloud storage solutions. The company has become a significant player in the AI and big data industry in South Korea. They offer high-quality AI-powered chatbots, including for call centres and interactive educational services.

- H2O.ai provides an AI platform, the H2O AI Cloud, to help businesses, government entities, non-profits, and academic institutions create, deploy, monitor, and share data models or AI applications for various use cases. The platform offers automated machine learning capabilities powered by H2O-3, H2O Hydrogen Torch, and Driverless AI, and is designed to help organisations work more efficiently on their AI projects.

- Frame AI provides an AI-powered customer intelligence platform. The software analyses human interactions and uses AI to understand the driving factors of business outcomes within customer service. It aims to assist executives in making real-time decisions about the customer experience by combining data about customer interactions across various platforms, such as helpdesks, contact centres, and CRM transcripts.

- Uizard offers a rapid, AI-powered UI design tool for designing wireframes, mockups, and prototypes in minutes. The company’s mission is to democratise design and empower non-designers to build digital, interactive products. Uizard’s AI features allow users to generate UI designs from text prompts, convert hand-drawn sketches into wireframes, and transform screenshots into editable designs.

- Moveworks provides an AI platform that is designed to automate employee support. The platform helps employees to automate tasks, find information, query data, receive notifications, and create content across multiple business applications.

- Tome develops a storytelling tool designed to reduce the time required for creating slides. The company’s online platform creates or emphasises points with narration or adds interactive embeds with live data or content from anywhere on the web, 3D renderings, and prototypes.

- Jasper is an AI writing tool designed to assist in generating marketing copy, such as blog posts, product descriptions, company bios, ad copy, and social media captions. It offers features such as text and image AI generation, integration with Grammarly and other Chrome extensions, revision history, auto-save, document sharing, multi-user login, and a plagiarism checker.

- Eightfold AI provides an AI-powered Talent Intelligence Platform to help organisations recruit, retain, and grow a diverse global workforce. The platform uses AI to match the right people to the right projects, based on their skills, potential, and learning ability, enabling organisations to make informed talent decisions. They also offer solutions for diversity, equity, and inclusion (DEI), skills intelligence, and governance, among others.

- Arthur provides a centralised platform for model monitoring. The company’s platform is model and platform agnostic, and monitors machine learning models to ensure they deliver accurate, transparent, and fair results. They also offer services for explainability and bias mitigation.

- DNSFilter is a cloud-based, AI-driven content filtering and threat protection service, that can be deployed and configured within minutes, requiring no software installation.

- Spot AI specialises in building a modern AI Camera System to create safer workplaces and smarter operations for every organisation. The company’s AI Camera System combines cloud and edge computing to make video footage actionable, allowing customers to instantly surface and resolve problems. They offer intelligent video recorders, IP cameras, cloud dashboards, and advanced AI alerts to proactively deliver insights without the need to manually review video footage.

- People.ai is an AI-powered revenue intelligence platform that helps customers win more revenue by providing sales, RevOps, marketing, enablement, and customer success teams with valuable insights. The company’s platform is designed to speed up complex enterprise sales cycles by engaging the right people in the right accounts, ultimately helping teams to sell more and faster with the same headcount.

These examples highlight a few startups worth considering, but the landscape is rich with innovative options for organisations to explore. Similar to other emerging tech sectors, the AI startup market will undergo consolidation over time, and incumbent providers will continue to improve and innovate their own AI capabilities. Till then, these startups will continue to influence enterprise technology adoption and challenge established providers in the market.

The UN’s global stocktake synthesis report underscores the need for significant efforts to meet the ambitious goals of the Paris Agreement to keep the global warming limit to 1.5ºC, compared to pre-industrial levels. Achieving this requires collective action from governments, organisations, and individuals.

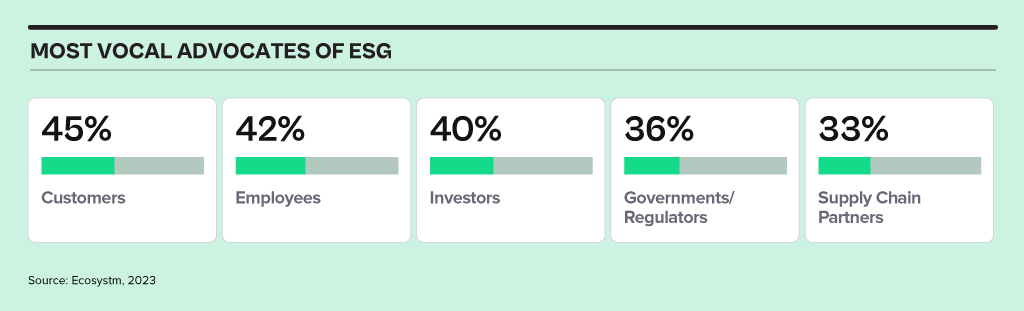

While regulators focus on mandates, organisations today are being influenced more by individual responsibility for positive impact. Customers and employees are leading ESG actions – another fast-emerging voice driving ESG initiatives are value chain partners looking to build sustainable supply chains.

Ecosystm research reveals that only 27% of organisations worldwide currently view ESG as a strategic imperative, yet we anticipate rapid change in the landscape.

Click below to find out what Ecosystm analysts Gerald Mackenzie, Kaushik Ghatak, Peter Carr and Sash Mukherjee consider the top 5 ESG trends that will shape organisations’ sustainability roadmaps in 2024.

Click here to download ‘Ecosystm Predicts: Top 5 ESG Trends in 2024’ as a PDF.

#1 Organisations Will Evolve ESG Strategies from Compliance to Customer & Brand Value

Many of the organisations that we talk to have framed their ESG strategy and roadmaps primarily in relation to compliance and regulatory standards that they need to meet, e.g. in relation to emissions reporting and reduction, or in verifying that their supply chains are free from Modern Slavery.

However, organisations that are more mature in their journeys have realised that ESG is quickly becoming a strategic differentiator and compliance is only the start of their sustainability journey.

Customers, employees, and investors are increasingly selective about the brands they want to associate with and expect them to have a purpose and values that are aligned with their own.

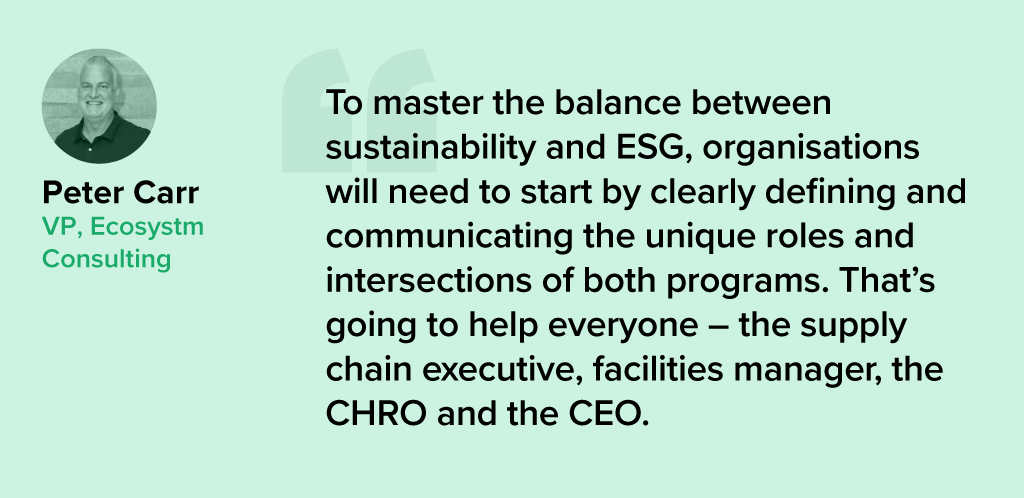

#2 Sustainability Will Remain a Stepping-Stone to Full ESG

Heading into 2024, the corporate continues to navigate the nuances between Sustainability and Environmental, Social, and Governance (ESG) initiatives. Sustainability, focused on environmental stewardship, is a common starting point for corporate responsibility, offering measurable goals for a solid foundation.

Yet, the transition to comprehensive ESG, which includes broader social and governance issues alongside environmental concerns, demands broader scope and deeper capabilities, shifting from quantitative to qualitative measures. The trend of merging sustainability with ESG risks is blurring distinct objectives, potentially complicating reporting and compliance, and causing confusion in the market. Nevertheless, this conflation ultimately paves the way for more integrated, holistic corporate strategies.

By aligning sustainability efforts with wider ESG goals, companies will develop more comprehensive solutions that address the entire spectrum of corporate responsibility.

#3 ESG Consulting Will Grow – Till Industry Templates Take Over

At the end of 2022, LinkedIn buzzed with announcements of Chief Sustainability Officer appointments. However, the Global Sustainability Barometer Study reveals that only around one-third of global organisations have a dedicated sustainability lead. What changed?

Organisations have recognised that ESG is intricate, requiring a comprehensive focus and a capable team, not just a sustainability leader.

Each organisation’s path to sustainability is unique, shaped by factors like size, industry, location, stakeholders, culture, and values. Successfully integrating ESG requires a nuanced understanding of an organisation’s barriers, opportunities, and risks, making it challenging to navigate the sustainability journey alone. This is complicated by the absence of clear government/industry mandates and guidelines that frame best practices.

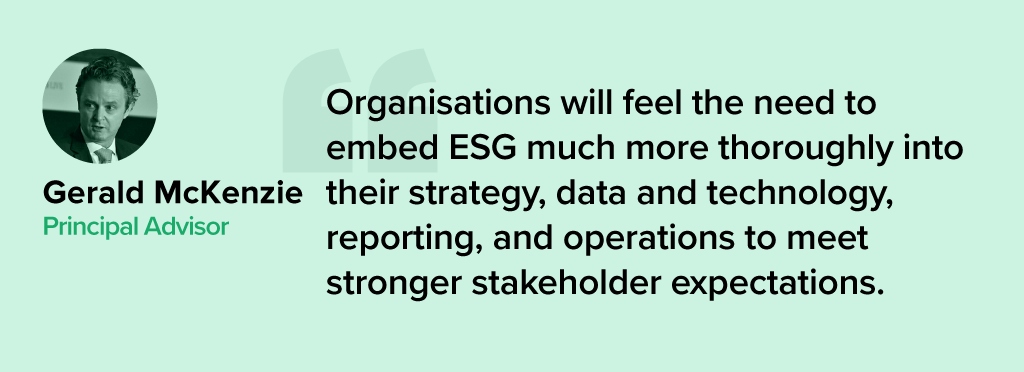

#4 Sustainability Tech Will Finally Gain Traction

Many organisations initiate sustainability journeys with promises and general strategies. While the role of technology in accelerating goals is recognised, alignment has been lacking. In 2024 sustainability tech will gain traction.

Environmental Tech. Improved sensors and analytics will enhance monitoring of air and water quality, carbon footprint, biodiversity, and climate patterns.

Carbon-Neutral Transportation. Advancements in electric and hydrogen vehicles, batteries, and clean mobility infrastructure will persist.

Circular Economy. Innovations like reverse logistics and product lifecycle tracking will help reduce waste and extend product/material life.

Smart Grids and Renewable Energy. Smart grid tech and new solutions for renewable energy integration will improve energy distribution.

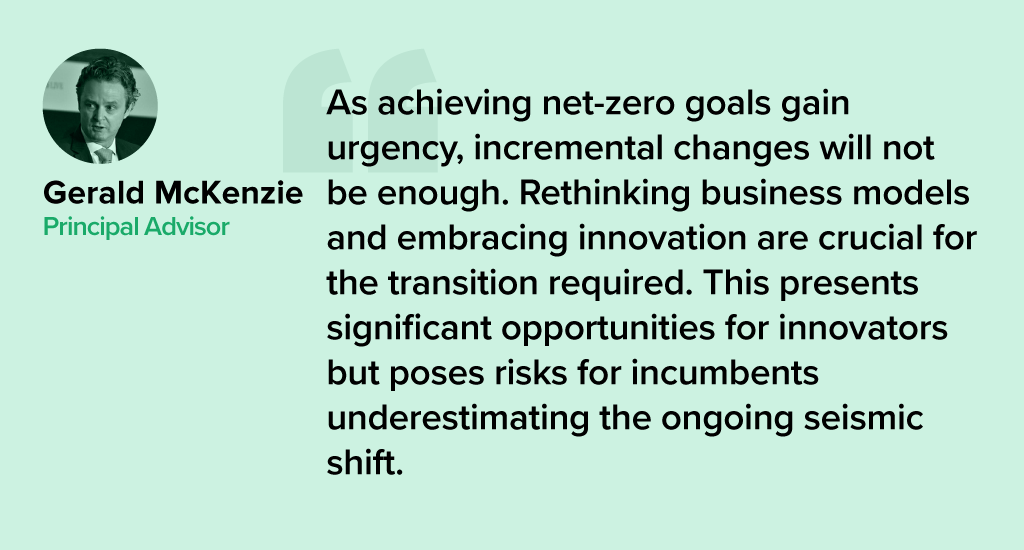

#5 Cleantech Innovation Will See Increased Funding

Cleantech is the innovation that is driving our adaptation to climate change. We expect that investments into, and the pace of innovation and adoption of Cleantech will accelerate into 2024.

As companies commit to their net-zero targets, the need to operationalise the technologies required to fuel this transition becomes all the more urgent. BloombergNEF reported that for Europe alone, nearly USD 220 billion was invested in Cleantech in 2022.

But to meet net-zero ambitions, annual investments in Cleantech will need to triple over the rest of this decade and quadruple in the next.

A lot gets written about cybersecurity – and organisations spend a lot on it! Ecosystm research finds that 63% of organisations across Asia Pacific are planning to increase their cyber budget for the next year. As budgets continue to rise, the threat landscape continues to get more complex and difficult to navigate. Despite increasing spend, 69% of organisations believe a breach is inevitable. And breaches can be EXPENSIVE! Medibank, in Australia, was breached in (or around) October, 2022. The cost of the breach is expected to reach around USD 52 million when everything is done and dusted – and this does not include the impacts of any potential findings or outcomes from regulatory investigations or litigation.

Recovering Strong

While cybersecurity is still crucially important, the ability to recover from breaches quickly and cost-effectively is also imperative. How you recover from a breach will ultimately determine your organisation’s long-term viability and success. The capabilities needed to recover quickly include:

- A well-documented and practices incident response plan. The plan should outline the roles and responsibilities of all team members, communication protocols, and steps to be taken in the event of a breach.

- Backup and Disaster Recovery (DR) solutions. Regular backups of critical data and systems are essential to quickly recover from a breach. Backup solutions should include offsite or cloud-based options that are isolated from the main network. DR solutions ensure that critical systems can be quickly restored and made operational after a breach.

- Cybersecurity awareness training. Investing in regular training for all employees is crucial to ensure they are aware of the latest threats and know how to respond in the event of a breach.

- Automated response tools. Automation can help speed up the response time during a breach by automatically blocking malicious IPs, quarantining infected devices, or taking other predefined actions based on the nature of the attack.

- Threat intelligence. This can help organisations stay ahead of the latest threats and vulnerabilities and frame quicker responses if a breach occurs.

Backup and Disaster Recovery is Evolving

Most organisations already have backup and disaster recovery capabilities in place – but too often they are older systems, designed more as a “just in case” versus a “will keep us in business” capability. Backup and DR systems are evolving and improving – and with the increased likelihood of a breach, it is a good time to consider what a modern Backup and DR system can provide to your organisation. Here are some of the key trends and considerations that technology leaders should be aware of:

- Cloud-based solutions. More organisations are moving towards cloud-based backup and DR solutions. Cloud solutions offer several advantages, including scalability, cost-effectiveness, and the ability to access data and systems from anywhere. However, technology leaders need to consider data security, compliance requirements, and the reliability of the cloud service provider.

- Hybrid options. As hybrid cloud becomes the norm for most organisations, hybrid solutions backup and DR that combine on-premises and cloud-based backups are becoming more popular. This approach provides the best of both worlds – the security and control of on-premises backups with the scalability and flexibility of the cloud.

- Increased use of automation. Automation is becoming more prevalent in backup and DR solutions. Automation helps reduce the time it takes to backup data, restore systems, and test DR plans. It also minimises the risk of human error. Technology leaders should look for solutions that offer automation capabilities while also allowing for manual intervention when necessary.

- Cybersecurity integration. With the rise of cyberattacks, especially ransomware, it is crucial that backup and DR solutions are integrated with an organisation’s cybersecurity strategy. Backup data should be encrypted and isolated from the main network to prevent attackers from accessing or corrupting it. Regular testing of backup and DR plans should also include scenarios where a cyberattack, such as ransomware, is involved.

- More frequent backups. Data is becoming more critical to business operations, so there is a trend towards more frequent backups, even continuous backups, to minimise data loss in the event of a disaster. Technology leaders need to balance the need for frequent backups with the cost and complexity involved.

- Super-fast data recovery. Some data recovery platforms can recover data FAST – in as little as 6 seconds. The ability to recover data faster than the bad actors can delete it makes organisations less vulnerable and buys more time to plug the gaps that the attackers are exploiting to gain access to data and systems.

- Monitoring and analytics. Modern backup and DR solutions offer advanced monitoring and analytics capabilities. This allows organisations to track the performance of their backups, identify potential issues before they become critical, and optimise their backup and DR processes. Technology leaders should look for solutions that offer comprehensive monitoring and analytics capabilities.

- Compliance considerations. With the increasing focus on data privacy and protection, organisations need to ensure that backup and DR solutions are compliant with relevant regulations, often dictated at the industry level in each geography. Technology leaders should work with their legal and compliance teams to ensure that their backup and DR solutions meet all necessary requirements.

The sooner you evolve and modernise your backup and disaster recovery capabilities, the more breathing room your cybersecurity team has, to improve the ability to repel threats. New security architectures and postures – such as Zero Trust and SASE are emerging as better ways to build your cybersecurity capabilities – but they won’t happen overnight and require significant investment, training, and business change to implement.

In our previous Ecosystm Insights, Ecosystm Principal Advisor, Gerald Mackenzie, highlighted the key drivers for boosting ESG maturity and the need to transition from standalone ESG projects to integrating ESG goals into organisational strategy and operations.

This shift can be difficult, requiring an alignment of ESG objectives with broader strategic aims and using organisational capabilities effectively. The solution involves prioritising essential goals, knitting them into overall business strategy, quantifying success metrics, and establishing incentives and governance for effective execution.

The benefits are proven and significant. Stronger Customer and Employee Value Propositions, better bottom line, improved risk profile, and more attractive enterprise valuations for investors and lenders.

According to Gerald, here are 5 things to keep in mind when starting on an ESG journey.

Download ‘Embedding Sustainability in Corporate Strategy and Operations’ as a PDF