Banks, insurers, and other financial services organisations in Asia Pacific have plenty of tech challenges and opportunities including cybersecurity and data privacy management; adapting to tech and customer demands, AI and ML integration; use of big data for personalisation; and regulatory compliance across business functions and transformation journeys.

Modernisation Projects are Back on the Table

An emerging tech challenge lies in modernising, replacing, or retiring legacy platforms and systems. Many banks still rely on outdated core systems, hindering agility, innovation, and personalised customer experiences. Migrating to modern, cloud-based systems presents challenges due to complexity, cost, and potential disruptions. Insurers are evaluating key platforms amid evolving customer needs and business models; ERP and HCM systems are up for renewal; data warehouses are transforming for the AI era; even CRM and other CX platforms are being modernised as older customer data stores and models become obsolete.

For the past five years, many financial services organisations in the region have sidelined large legacy modernisation projects, opting instead to make incremental transformations around their core systems. However, it is becoming critical for them to take action to secure their long-term survival and success.

Benefits of legacy modernisation include:

- Improved operational efficiency and agility

- Enhanced customer experience and satisfaction

- Increased innovation and competitive advantage

- Reduced security risks and compliance costs

- Preparation for future technologies

However, legacy modernisation and migration initiatives carry significant risks. For instance, TSB faced a USD 62M fine due to a failed mainframe migration, resulting in severe disruptions to branch operations and core banking functions like telephone, online, and mobile banking. The migration failure led to 225,492 complaints between 2018 and 2019, affecting all 550 branches and required TSB to pay more than USD 25M to customers through a redress program.

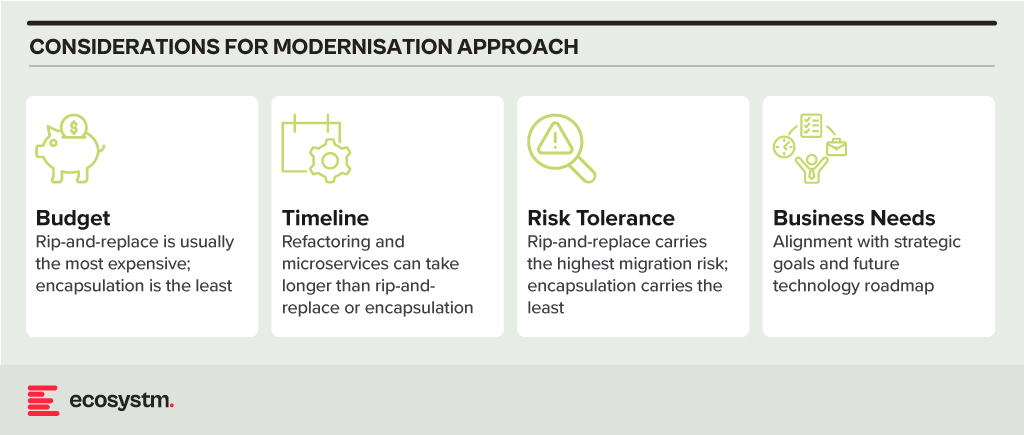

Modernisation Options

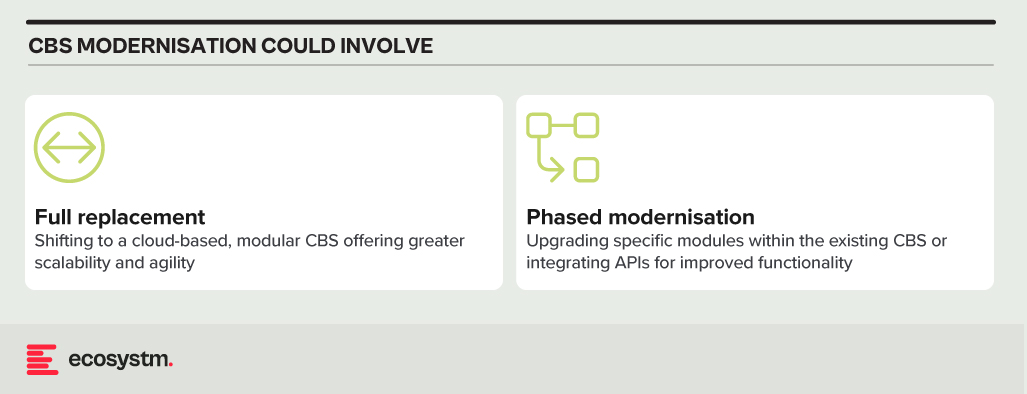

- Rip and Replace. Replacing the entire legacy system with a modern, cloud-based solution. While offering a clean slate and faster time to value, it’s expensive, disruptive, and carries migration risks.

- Refactoring. Rewriting key components of the legacy system with modern languages and architectures. It’s less disruptive than rip-and-replace but requires skilled developers and can still be time-consuming.

- Encapsulation. Wrapping the legacy system with a modern API layer, allowing integration with newer applications and tools. It’s quicker and cheaper than other options but doesn’t fully address underlying limitations.

- Microservices-based Modernisation. Breaking down the legacy system into smaller, independent services that can be individually modernised over time. It offers flexibility and agility but requires careful planning and execution.

Financial Systems on the Block for Legacy Modernisation

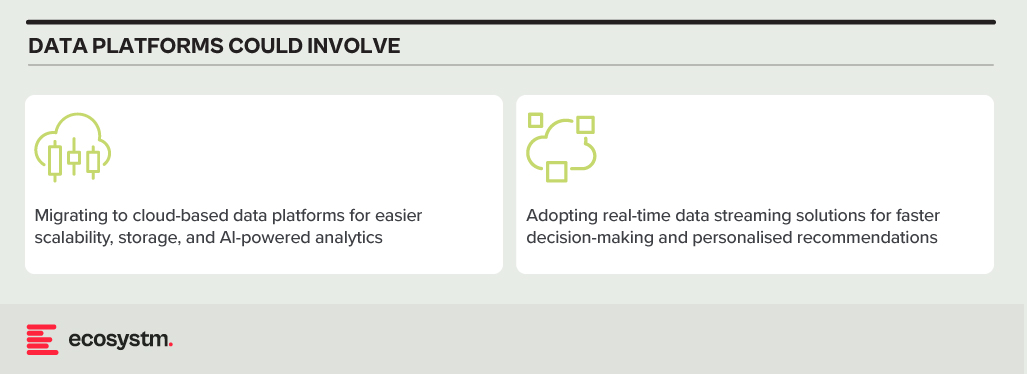

Data Analytics Platforms. Harnessing customer data for insights and targeted offerings is vital. Legacy data warehouses often struggle with real-time data processing and advanced analytics.

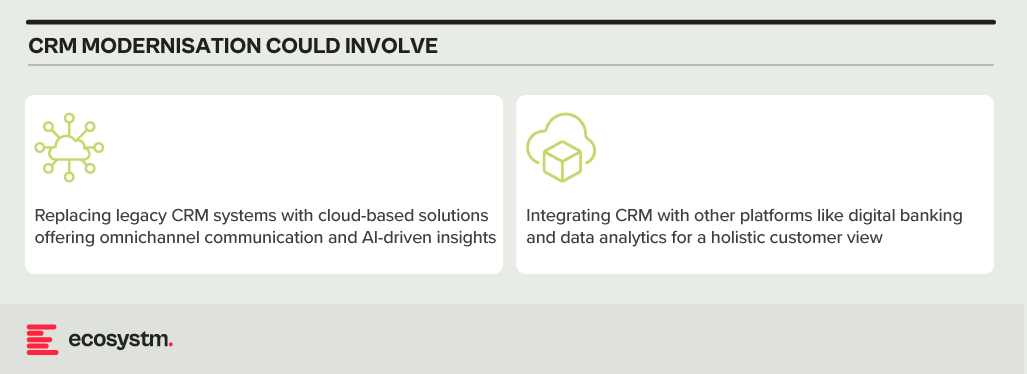

CRM Systems. Effective customer interactions require integrated CRM platforms. Outdated systems might hinder communication, personalisation, and cross-selling opportunities.

Payment Processing Systems. Legacy systems might lack support for real-time secure transactions, mobile payments, and cross-border transactions.

Core Banking Systems (CBS). The central nervous system of any bank, handling account management, transactions, and loan processing. Many Asia Pacific banks rely on aging, monolithic CBS with limited digital capabilities.

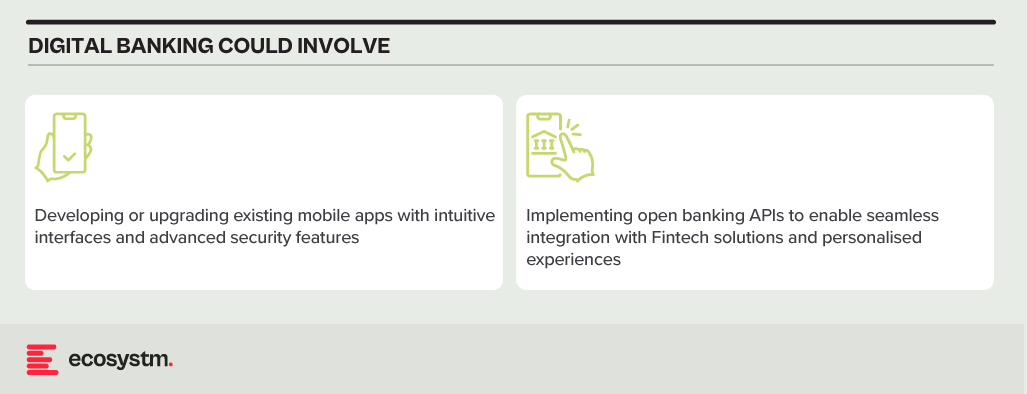

Digital Banking Platforms. While several Asia Pacific banks provide basic online banking, genuine digital transformation requires mobile-first apps with features such as instant payments, personalised financial management tools, and seamless third-party service integration.

Modernising Technical Approaches and Architectures

Numerous technical factors need to be addressed during modernisation, with decisions needing to be made upfront. Questions around data migration, testing and QA, change management, data security and development methodology (agile, waterfall or hybrid) need consideration.

Best practices in legacy migration have taught some lessons.

Adopt a data fabric platform. Many organisations find that centralising all data into a single warehouse or platform rarely justifies the time and effort invested. Businesses continually generate new data, adding sources, and updating systems. Managing data where it resides might seem complex initially. However, in the mid to longer term, this approach offers clearer benefits as it reduces the likelihood of data discrepancies, obsolescence, and governance challenges.

Focus modernisation on the customer metrics and journeys that matter. Legacy modernisation need not be an all-or-nothing initiative. While systems like mainframes may require complete replacement, even some mainframe-based software can be partially modernised to enable services for external applications and processes. Assess the potential of modernising components of existing systems rather than opting for a complete overhaul of legacy applications.

Embrace the cloud and SaaS. With the growing network of hyperscaler cloud locations and data centres, there’s likely to be a solution that enables organisations to operate in the cloud while meeting data residency requirements. Even if not available now, it could align with the timeline of a multi-year legacy modernisation project. Whenever feasible, prioritise SaaS over cloud-hosted applications to streamline management, reduce overhead, and mitigate risk.

Build for customisation for local and regional needs. Many legacy applications are highly customised, leading to inflexibility, high management costs, and complexity in integration. Today, software providers advocate minimising configuration and customisation, opting for “out-of-the-box” solutions with room for localisation. The operations in different countries may require reconfiguration due to varying regulations and competitive pressures. Architecting applications to isolate these configurations simplifies system management, facilitating continuous improvement as new services are introduced by platform providers or ISV partners.

Explore the opportunity for emerging technologies. Emerging technologies, notably AI, can significantly enhance the speed and value of new systems. In the near future, AI will automate much of the work in data migration and systems integration, reducing the need for human involvement. When humans are required, low-code or no-code tools can expedite development. Private 5G services may eliminate the need for new network builds in branches or offices. AIOps and Observability can improve system uptime at lower costs. Considering these capabilities in platform decisions and understanding the ecosystem of partners and providers can accelerate modernisation journeys and deliver value faster.

Don’t Let Analysis Paralysis Slow Down Your Journey!

Yes, there are a lot of decisions that need to be made; and yes, there is much at stake if things go wrong! However, there’s a greater risk in not taking action. Maintaining a laser-focus on the customer and business outcomes that need to be achieved will help align many decisions. Keeping the customer experience as the guiding light ensures organisations are always moving in the right direction.

Ecosystm, supported by their partner Zurich Insurance, conducted an invitation-only Executive ThinkTank at the Point Zero Forum in Zurich, earlier this year. A select group of regulators, investors, and senior executives from financial institutions from across the globe came together to share their insights and experiences on the critical role data is playing in a digital economy, and the concrete actions that governments and businesses can take to allow a free flow of data that will help create a global data economy.

Here are the key takeaways from the ThinkTank.

- Bilateral Agreements for Transparency. Trade agreements play an important role in developing standards that ensure transparency across objective criteria. This builds the foundation for cross-border privacy and data protection measures, in alignment with local legislations.

- Building Trust is Crucial. Privacy and private data are defined differently across countries. One of the first steps is to establish common standards for opening up the APIs. This starts with building trust in common data platforms and establishing some standards and interoperability arrangements.

- Consumers Can Influence Cross-Border Data Exchange. Organisations should continue to actively lobby to change regulator perspectives on data exchange. But, the real impact will be created when consumers come into the conversation – as they are the ones who will miss out on access to global and uniform services due to restrictions in cross-country data sharing.

Read below to find out more.

Click here to download “Opportunities Created by Cross Border Data Flows” as a PDF

We are in the midst of an economic and social crisis. COVID-19 will have far-reaching effects on organisations and how they do business. It is expected to drive more investments in Fintech, especially in digital payments, as more organisations and consumers adopt eCommerce. Countries will also have to re-think the ways they trade with other countries, as travel restrictions continue. This is expected to boost the Fintech industry and July was witness to how Fintech organisations, financial institutions and governments are gearing up to leverage Fintech in their path to economic and social recovery.

Financial Industry Seeing More Open Banking Initiatives

The banking industry is fast moving towards collaboration and openness. July saw several initiatives that take the industry closer to open banking.

Late last year, South Korea piloted an open banking system with participation from local banks and lenders. The Financial Services Commission (FSC), South Korea’s top financial regulator reported in July that the initiative had participation from 72 companies including commercial banks and Fintech firms with 20 million subscribers using the open banking services.

Australia introduced an open banking initiative, monitored by the Australian Competition and Consumer Commission (ACCC). From July, Australia’s banking customers can share their financial and banking data with accredited businesses under Consumer Data Right Act to access a better suite of financial applications.

There is global expansion as well. Railsbank, a global open banking platform with a presence in Southeast Asia introduced their services in the US market. The company will offer Banking-as-a Service, Cards-as-a Service and Credit Card-as-a-Service in the US market. Khaleeji Commercial Bank (KHCB), an Islamic bank in Bahrain, launched their open banking service enabling a customer to link their bank accounts with other banks and manage through the ‘Khaleeji 360’ platform. The portal allows clients to view all their bank accounts, automate operations and conduct banking through a unified platform.

Financial Institutions Increasing Partnerships with Fintech

Financial institutions no longer look at Fintech as competition. They appreciate that customers are at the centre of their entire operation – and Fintech services can and will provide them with the solutions they need. As financial institutions re-think their transformation journeys and face increasingly stringent regulations, they no longer have the option of ignoring Fintechs.

American Express, Visa, Mastercard and Discover came together to roll out a global standard. The big four’s advanced digital checkout solution Click to Pay is an online checkout system based on EMV Secure Remote Commerce (SRC) to make online payments across websites, mobile applications and connected devices, frictionless.

With an aim to unify payment solutions, a group of 16 major European banks launched the European Payment Initiative (EPI) to create a unified pan-European payment solution leveraging Instant Payments/SEPA Instant Credit Transfer (SCT Inst), including a card, e-wallet and P2P payments.

We also saw financial institutions strengthen their cross-border payment services in July. Deutsche Bank partnered with Airwallex to offer virtual account collections and API-enabled foreign exchange services in Japan and Hong Kong. The service will enable merchants and traders to transact through virtual accounts and APIs without opening bank accounts in foreign markets. Mastercard and Bank of China partnered to enhance cross-border business payments into China. This will enable global businesses to send payments to China while accessing real-time exchange rates, reduce the need for unnecessary documentation between merchants, and reduce transaction hassles and costs.

Fintechs Facilitating Cross-border Trade

Seamless cross-border financial transactions will be key to economic recovery, whether easy remittance or the ability to reach a larger market and be able to trade beyond borders.

July saw the formalisation of the Digital Economy Partnership Agreement (DEPA) between New Zealand, Chile and Singapore, to facilitate end-to-end digital trade, which includes establishing digital identities, paperless trade and the development of Fintech solutions to support it. The initiative also intends to allow cross-border data flow and give access to necessary government data to small and medium enterprises (SMEs) enabling them to be digital-ready to explore newer markets.

Dubai International Financial Centre (DIFC) signed an MoU with Jiaozi Fintech Dreamworks based in China opening new opportunities for innovation and trade. The agreement will enable Fintech companies based in both cities to access each other’s markets. Primarily established to facilitate the ‘Belt and Road’ initiative, it is a critical component of the DIFC’s 2024 strategy to strengthen relationships with the international financial community and increase access to the South-South corridor. Over the last few years, DIFC has been associated with over 200 Fintech organisations, and last month invested in four Fintech startups through their accelerator program. The agreement with Jiaozi will look at collaboration opportunities in Blockchain, AI and Cloud and will facilitate cross-border workshops and training programs.

Continuing Interests in Emerging Economies

Fintechs have been a means to bring about financial inclusion and are increasingly being used to target the unbanked and underbanked. Emerging economies continue to be attractive for Fintech organisations and global financial institutions.

With much of Malaysia’s economy dependent on foreign workers, Instapay, regulated by the Bank Negara Malaysia (BNM), announced a collaboration with Mastercard, to provide e-wallet accounts to the migrant workers. The widespread use of e-wallets by the migrant worker community will bring benefits to both workers, as well as their employers. Interestingly, Fintech providers in emerging economies are also looking to expand into other emerging markets. Malaysia’s GHL Group received approval from Philippines Securities and Exchange Commission to operate a lending business through their new unit, GHL Philippines Financing Services. GHL has been diversifying its business and has been operating its lending business in Malaysia and Thailand since 2019.

Crown Agent Bank, a wholesale foreign exchange and cross-border payment services based in the UK, partnered with South Africa’s biometric-based payment company, Paycode. Together the companies are aiming to reach 100 million unbanked customers where Crown Agents Bank will use their FX and payment services to bolster Paycode’s product offering and support financial inclusion across Sub-Saharan Africa.

India and Indonesia in the Asia Pacific continue to be popular markets because of the huge proportion of the unbanked population. Rapyd, a UK based global B2B Fintech-as-as-service provider partnered with major Indian e-payment providers – including Paytm, PhonePe, PayU, Citibank, DBS Bank, HDFC Bank, BharatPay, and Unimoni to launch an all-in-one payments solution that spans credit and debit cards, UPI, wallets, and cash. New registrations for digital banking in Indonesia are on the rise and Fintech startup Akulaku is capitalising on the potential digital banking overhaul to offer affordable and comprehensive financial services to consumers.

Fintechs benefiting other industries

The Fintech revolution has shown the path to several other industries – Healthcare and Agriculture are some of the industries that are hoping to benefit from Fintech organisations and their innovations. The MoU between Alibaba Cloud, Pfizer and Singapore’s Fintech Academy announced earlier in July, promises to give early and necessary guidance to Healthtech start-ups, and shows the deep connection between Healthtech and Fintech. In the Philippines, in an effort to improve financial services for farmers, AgriNurture acquired Fintech firm Pay8. By leveraging Pay8 e-wallet services, farmers will be able to access online payment services. This will enable the largely unbanked farmer community to become an active part of the economy.

The technology that these industries are looking to benefit from is Blockchain. South Korea brought Blockchain to their healthcare industry for better data management and storage. The 3 major telecommunications providers in the country – KT, SK Telecom and mobile carrier LG U+ – have also collaborated with KB Insurance to launch the blockchain-based mobile notification service (MNS) by matching customer data to their mobile subscription information. Oxfam Ireland – a charity organisation based in Ireland, received a sum of USD 1.18 million from the European Commission for a Blockchain-based pilot. The company is working on a project -The UnBlocked Cash – to help disaster-affected communities receive cash-based entitlements with more efficiency and traceability.

Fintech will continue to be a cornerstone of economic and social recovery in the future, and the financial industry will see more collaborations between Fintech organisations, financial institutions and governments. Other industries will continue to take learnings from Fintech.

Singapore is committed to empower its small and medium enterprises (SMEs) to make better financial decisions and avail of seamless trade and financial transactions across the larger global economy. In June, the Digital Economic Partnership Agreement (DEPA) was signed between New Zealand, Singapore and Chile. The initiative includes facilitating end-to-end digital trade – by creating digital identities, allowing paperless trade and developing Fintech solutions – and ensuring a trusted cross-border data flow. To learn more about the DEPA agreement, register for the “Re-image the Digital Economy” webinar on the 29th July at 10am SGT.

This follows the announcement that was made last year by the Monetary Authority of Singapore (MAS) and Infocomm Media Development Authority (IMDA); of the successful completion of phase 1 of the proof-of-concept (POC) for its Business sans Borders (BSB). BSB is meant to be a “meta-hub” connecting several SME-centric platforms (starting within the Philippines, India and Singapore) giving SMEs seamless access to a larger ecosystem of buyers, sellers, logistics service providers, financing, and digital solution providers; and allowing them to be part of the larger global marketplace. The PoC involved a collaboration with private sector partners such as GlobalLinker, Mastercard, PwC, SAP and Yellow Pages.

AMTD Aligns with the BSB Objective

Hongkong-based investment banking firm AMTD Group leads a consortium that includes Xiaomi Finance, Singapore’s SP Group, and Funding Societies, that is a contender for one of Singapore’s digital wholesale banking licenses. While announcing their bid, they had clearly stated that they aimed to focus on SMEs in the region and globally. They continue to focus on SMEs by strengthening their partner ecosystem.

Last week AMTD announced a partnership with GlobalLinker making them the preferred financial services partner on the GlobalLinker’s SME-focused platform. AMTD intends to make available their entire ecosystem to SMEs including their virtual bank in Hong Kong, Airstar and their potential digital wholesale bank consortium in Singapore (which is to be called Singa Bank). In line with Singapore’s BSB objective, the partnership will see GlobalLinker join AMTD’s network which includes Fintech companies, regional banks and enterprises – SpiderNet. SpiderNet is a cross-sector ecosystem which is continuously expanding to connect and collaborate with shareholders, government bodies, industry associations, and clients. GlobalLinker’s AI-powered SME networking platform fosters SME digitalisation and helps members and customers connect with each other and use digital solutions. AMTD will be part of this network and bring the breadth of their partner ecosystem onto GlobalLinker’s platform.

Ecosystm Principal Advisor, Dheeraj Chowdhry says, “This marks the deepening of the trend of convergence between the established industry players and the Fintechs. The inefficiency of the obsession to ‘build’ and the associated resource and cost effort has perhaps been recognised on both sides and hence the path of coexistence and synergy seems more pragmatic. Fintechs are not competing but, in fact, complementing industry players by accelerating customer adoption of new digital formats for the entire landscape.”

AMTD Continues to Strengthen Partner Ecosystem

Last week also saw AMTD announce a collaboration with Singapore’s CIMB Bank and Funding Societies, to explore opportunities to create a wide range of banking and capital market services to aid SMEs with a one-stop solution for cross-regional and financial products.

Such partnerships by AMTD provides a glimpse of the group’s strong focus on Singapore. In April this year, AFIN and AMTD partnered to establish the USD 36 million AMTD ASEAN-Solidarity Fund. In May, AMTD, MAS, and Singapore FinTech Association (SFA) announced the launch of a USD 4.3 million MAS-SFA-AMTD FinTech Solidarity Grant to support Singapore-based FinTech firms.

AMTD remains committed to evolving their capabilities and ecosystem to empower the SME market in Singapore and the region. AMTD Digital announced their intention of acquiring a controlling stake in PolicyPal, Singapore’s InsureTech pioneer, and CapBridge Financial, a leading private capital platform for investing in growth companies globally. They have also expressed their intentions to acquire a controlling stake in FOMO Pay, a Singapore-based QR code and digital payment solution provider.

“AMTD’s early cognizance of the need for a strong ecosystem has led the organisation to their foray into partnerships and stakes in PolicyPal, FOMO Pay and now GlobalLinker. This strengthens AMTD’s commitment to the Fintech space including stakes in AirStar Digital Bank in Hong Kong and the Digital Bank application in Singapore,” says Chowdhry. “The Fintechs in AMTD’s stable will be part of the ‘AMTD web’ associated companies cutting across geographies and accelerate the ‘Business sans Borders’ objective of MAS and IMDA.”