One of my Twitter followers who is stressing about her kids going back to school this Fall was wondering if hotels could start offering elearning assistance as part of the re-purposing of their facilities.

Is this part of a digital hotel of the future? This digital hotel is a facility that is welcoming, hospitable, warm and can be used as a multi-functional space. Traditional revenue generation is measured in revenue from room nights, but given that instability in current demand, the facility can be re-purposed to highlight its network-enabled footprint. This is where global design strategies that leverage technology come into play, with a focus on integrative design for use. Digital classrooms, art exhibitions, alternatives to working from home – many things are possible.

With travel restrictions and hygiene and health concerns, hotels and tourism locations globally are having to pivot to a different way of doing business this year. Agility is critical, and how we measure agility and employ agility differentiate us.

I will explore the alternative view on recovery looking at the impact of COVID-19 on organisations in the hospitality industry and how they are pivoting digital priorities to adapt to the New Normal.

This post will focus on two aspects of the use of digital technology – more innovative ways to view industry recovery, and re-imaging the use of the physical asset from its traditional uses to more creative, digitally enabled functions.

Moving Towards A Different View of Recovery

Since Online Travel Agents (OTA) entered the scene, the hotel industry became obsessed with simple adjustments of rates. Revenue managers focus on analysing, forecasting, and optimising hotel inventory through availability restrictions and dynamic rates. This has become key in measuring a hotel’s demand.

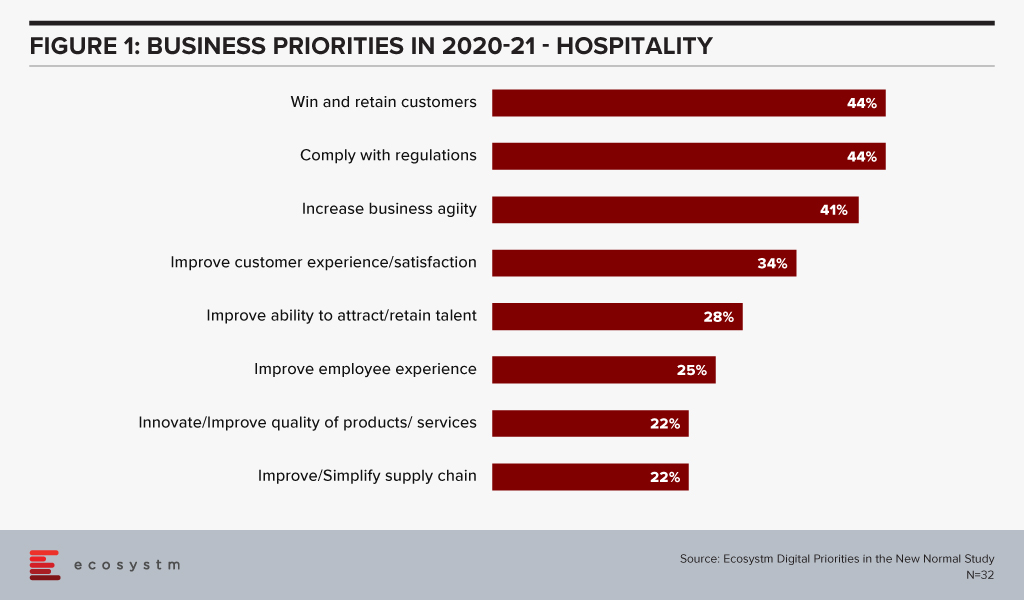

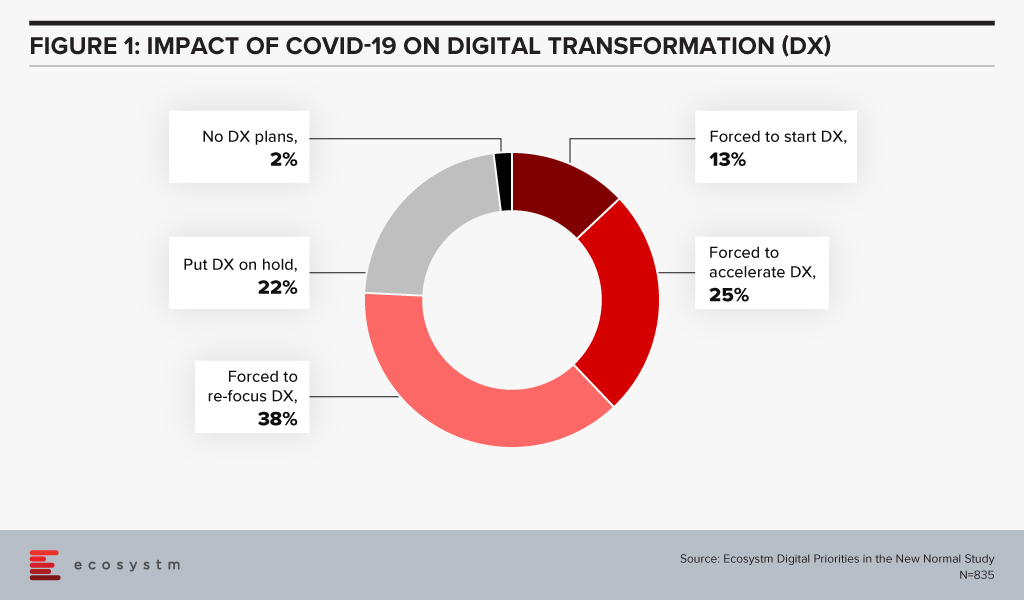

RevPAR, or revenue per available room, is one of the traditional and still the most instilled metrics in the industry. But given demand issues with the pandemic, is revenue forecasting per room the best way to examine hotel recovery? A traditional view on revenue fails when hotel closures and uncertainty on opening impact the ability to forecast and to determine capacity. As seen in Figure 1, both winning customers and increasing agility are paramount to recovery.

When a destination becomes inaccessible to the traditional clientele, your actual location becomes relevant to a different set of customers. This is for different reasons – so hotels must find different ways to leverage the resources and assets of the business.

One way of looking at this is by re-imaging the use of the physical assets and a suggested approach is looking towards profit planning and management with ProfPASF or Profit per Available Square Feet. We look at hotel construction costs this way, so it stands to reason that utilisation of the asset might also be examined from a cost benefit perspective.

Impact on Digital Transformation

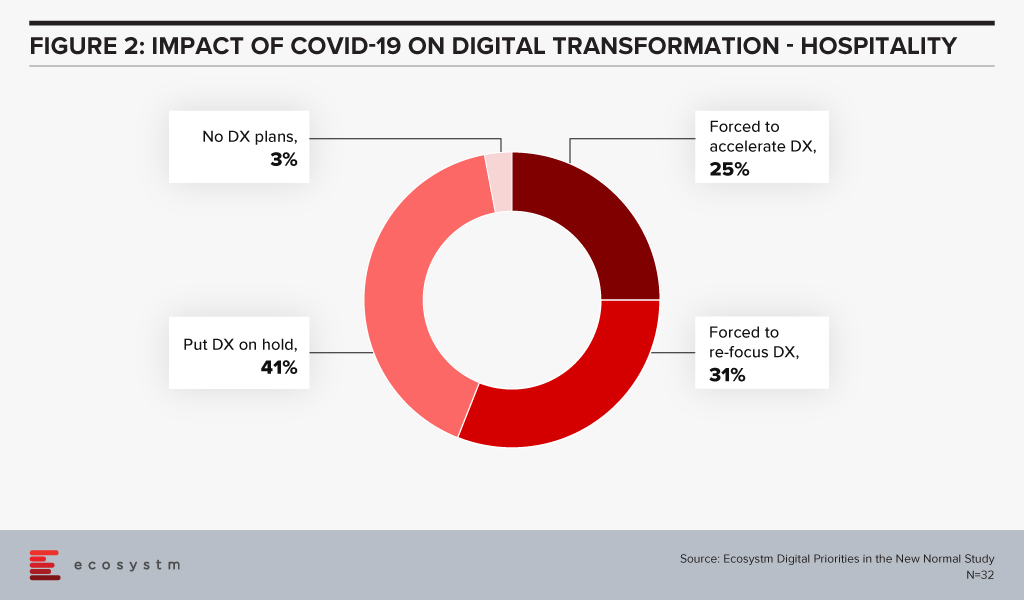

Where does technology play a role in re-imaging Hospitality? As an enabler, a facilitator, a business model supporter? How does the process of Hospitality need to change, and how can technology help? As seen in Figure 2, hotels have had to accelerate and modify their plans.

The structural assets of the business must either be repurposed or repackaged to take travel restrictions and hygiene and safety concerns into account.

There are several good examples of hotels who have had the ability financially to rethink and restructure the footprint to address issues that have come from the pandemic. The ones that already planned renovations prior to the crisis have added hygiene aspects such as improved ventilation and less porous floors and fabrics in the selection of materials used. And adding better spatial design to public spaces has allowed them to reinforce the concept of luxury. Documented renovation can be seen in innovative design work by Onyx Hospitality Group, Blink Design Group, independent brand View Hotels and Banyan Tree Holdings.

But this does not mean the hotel or destination must make the investment alone, or even all on-site. Using systems integrators and cloud resources to create digital enabled platforms for guest management, hygiene process management and physical mapping of the capacity of the facility using sensors and mobile are all methods for enabling the digital acceleration of tech investment in the property.

And personalisation of the experience is key, which leads to a discussion of personal data usage and management.

Social Distancing and the Hotel of the New Normal

Retailers, hoteliers and convention centres have the same thing in common, they are all physical locations trying to become safe yet contactless, socially distant yet memorable at the same time. As we have mentioned in previous reports, the comfort, safety and hygiene of the customer is paramount for their return to Hospitality. Using customer location data on a reliable online platform to track their movement, enable their facilities and services and limit the density of customers per square metre for health, safety and comfort are all aspects of tech-enabled social distancing.

Imagine that you are considering a day stay, for home working alternative or for having a local event. This needs to be within the sanctioned numbers of your locale. Guests want to know the population density of the location to determine their comfort level. Having a mobile app where potential visitors can see the state of the visitor density of the hotel would provide reassurance as to a safe visit.

Rich Contactless Content

With the encouragement of expanding the scope of technology and social distancing given priority, automated or contactless transaction technologies have seen an increase in implementation in the last six months. Having sensors and IoT technology implemented to see the footprint of the facility in use provides real-time insight for both the customer and the hotel, as to usage.

In order to be able to highlight the functions of both the room and the facility, augmented reality (AR) can demonstrate the use of interactive elements within hotel rooms without human contact.

AR applications within the hotel sector include offering in-house interactive elements (such as location maps and relevant points of interest). These provide digital history of the property and supply guests with relevant information when they are located within certain areas of the hotel (such as a menu if they happen to enter a restaurant).

Use of Space: Location & Hygiene for a Better Experience and as a Precaution

Hotel environments have evolved to add a healthcare layer, including well-being programs, and individual room controls. This includes materiality/ sanitised covering that protects against the spread of infection with clearly defined and explained roll-out cleaning protocols.

Accor has launched the Cleanliness & Prevention ALLSAFE label, and other brands like Hilton, Hyatt and IHG have tried to brand hygiene into the experience. But the challenge for many is how to restructure and re-image space utilisation to make it both pleasurable and secure.

Data for Purpose

With contact tracing in the news, many of us are already aware of the digital footprints we leave everywhere we go. And people have a wide variety of personal responses to this.

So how does a hotel use the information a guest either willingly offers or the hotel learns via services provided? If the hotel knows preferences prior to arrival, should they customise the room accordingly? Lighting, scent, preferred pillow choice, allergies – all are useful information. But what if preferences change or implementations are seen to be presumptuous?

Hilton is continually updating its guest technology offerings, from increasing in-app functionality to making further improvements to the entertainment system. One of their ideas is allowing guests to load personal or family pictures. These display on the TV, giving their hotel room more of a familiar sense of home.

And to be both keyless and cashless means the hotel needs to be mobile data enabled. All of this data, including mobile data, should flow like fine wine. But to do that requires knowledge, and learning – gained from experience and AI. How can I check your preferences are still the same? How should I use information I collected on you from a previous stay? Is that data kept on your mobile device, or on my hotel server? Is this in the cloud or on-premise in some manner?

Using Data and Intelligence for Personalised Experiences

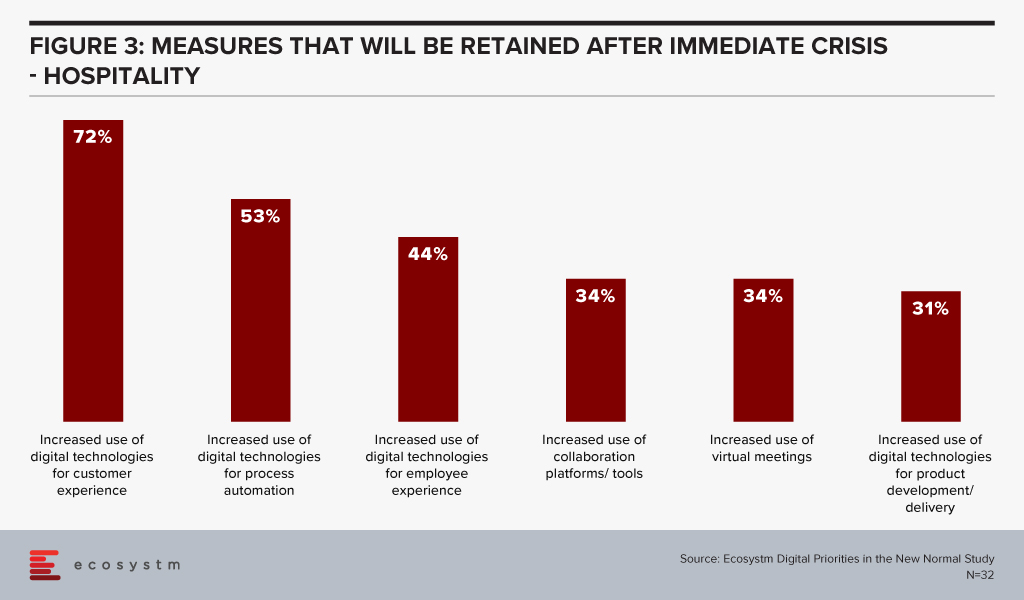

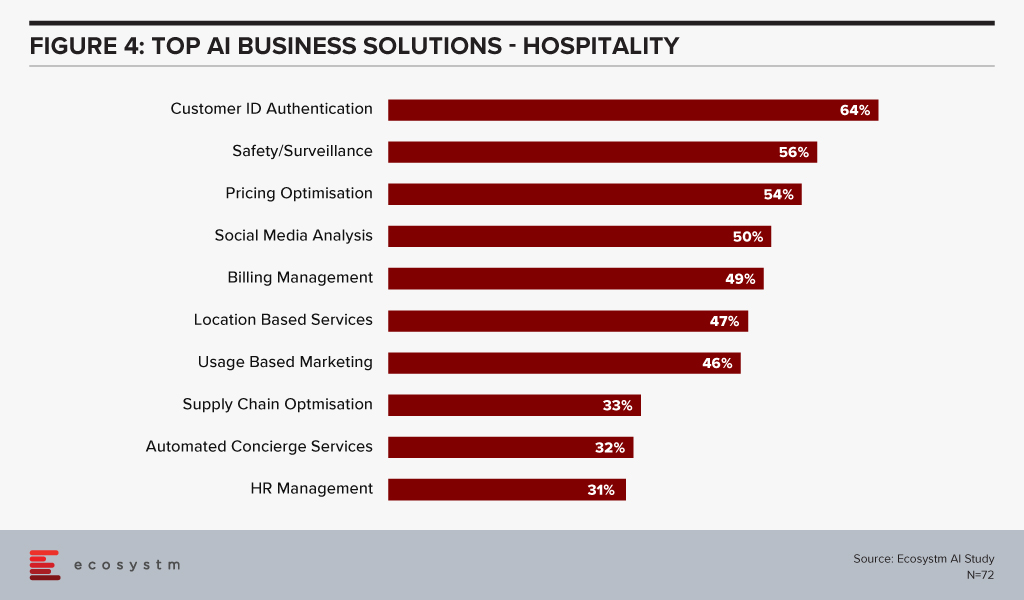

The final point shown in Figure 3 from the Ecosystm Digital Priorities in the New Normal study on technology direction from the pandemic, combined with Figure 4 from the Ecosystm AI Study showing the use of AI, highlights the need for technologies that support customer experiences and automate processes. Whether it is customer authentication at check-in, virtual customer assistance or rate pricing for appropriate engagement, technology can enable guest appreciation.

Summary – Three Post-Pandemic Takeaways

1. Demand for rooms will have to be viewed differently during this period, and cancellation policies already reflect this. To view recovery, use metrics that look at how the whole asset is being used on a physical basis.

2. Re-imagination of the physical asset will involve some agility and re-purposing within the business. Technology can help enable this, with some wise additions to add value. Voice, IoT and contactless mobile apps all are good candidates for enablement.

3. Data helps with understanding of guest preferences and can be used for staff learning and knowledge. But it must be held and used correctly. Listen carefully to what the guest is telling you and respond accordingly.

A decade ago, the axiom of a successful business model was to identify a need, find the market and then develop an idea or product that fits into that chain. It was a process of inserting a product in the customer’s already existing experience journey with the hope that the product/idea would deliver efficiency to the client. This efficiency could be financial, operational, marketing or cost savings – the uni-product, uni-feature approach.

There has been enough said about the many companies that failed to innovate beyond their existing product/feature and failed to stay ahead of the game. Nokia and Blackberry remain at the centre of any discussion about “lack of innovation”. There are others like Kodak, Canon, Napster, Palm, Blockbuster – that were devoured by innovative competitors.

The predators were ones with the vision to see the entire value chain and not just their own product. Netflix created content and distributed it, Apple touched the lives of their customers in multiple ways and AirBnb provided accommodation inventory, choice and booking all in one. The new secret sauce is to provide the customer with an ecosystem and not a product!

The Need to Transform

Cut to the COVID era – there are many businesses facing the downturn and experiencing the “moments of truth” giving rise to a desperate attempt to innovate, transform, survive, and come out as the rising stars. Ecosystm research finds that 98% of organisations have re-evaluated their Transformation roadmap (Figure 1), while 75% have started, accelerated or refocused their DX initiatives.

New business models are evolving, and accelerating digitalisation is the result. The digital movement, be it in food delivery or payments, is here to stay. This digital acceptance and absorption exaggerate the need for business models that capture holistic ecosystems and entire customer journeys, due to reasons that separate the hunter and the hunted.

- Margins will never be the same again as in the uni-product model. Using the F&B analogy; with the increasing number of customers wanting to dine in the comfort of their homes, restaurants cannot use ambiance as the price differentiator. Since most restaurants are available on food delivery services, customers are getting brand agnostic. This is the start of commoditisation of dining. Restaurants (or food caterers now!) will need to play the price card to remain competitive resulting in compressed margins. The food delivery market is expected to grow 4-fold to USD 8 billion by 2025 but with lower margins. This example of the food delivery model will be the same as experienced by retail, apparel and other industries.

- Customer experience will still be the differentiator and lever for loyalty and repeat purchase. Factors like proximity, parking, in-store experience, and store layout are fast getting replaced by the ease of navigation, user experience, seamless check out and finally efficient and timely delivery. The ease of transaction including multiple steps of search, assessment, evaluation, payment and delivery is of paramount importance. Customers do not want fractured journeys with multiple drop-offs. A unified seamless journey will win.

- Virtual, Digital and Automation are the three mantras that management consultants are betting on. However, this trilogy will not guarantee survival since the road to recovery is not a straight one. Different work schedules, observing various curves and on what point of the curve the business, its customer and the market are at, will add to the complexity of decision making and transformation.

Given the above, an obvious strategy to beat the existential crisis is to transform and seek out sustainable operating models. However, it may not be so simple since most businesses may not be able to change models as quickly as needed. There is an inherent cost to change since the existing processes and procedures have been well oiled and smoothed over time. The much-needed change requires the infusion of the 3Ts (time, technology, training) and associated costs. Most often, there is an inverse correlation noticed between the sturdiness of the business and its ability to be flexible to change. Businesses that are “rock-solid” and profitably sturdy and stable, have high inertia of transformation versus FinTech businesses, as an example, that pride themselves with nimble operations but are financially fragile and may not be able to absorb the cost of speedy transformation.

This Sturdy-Flexible continuum is the tight rope walk that businesses will need to walk in this need for transformation. Businesses that embark on this walk alone will find it extremely painful and lonely. Especially in the case of small business owners who are scared and low on all 3Ts.

The Rise of Ecosystems

The new world has manifested that businesses that use physical space or assets as their competitive advantage are more prone to be impacted. Retail, Education, Hospitality and Entertainment are some obvious examples that have been impacted by the physicality in their propositions. Digital businesses are more agile but have suffered in their inability to scale up in time to capture the increased demand.

Fashion retailer FJ Benjamin has decided to shut 300 physical stores and rely on online sales. This strategy also helps to utilise precious time to scale diversification. Other retailers too have been going down the FJ Benjamin path and ramping up eCommerce as this trend is expected to stick beyond COVID-19.

Zouk, the renowned nightclub with 30,000 square feet of space in Singapore uses this venue as a live streaming venue during the day to host bazaars for eCommerce vendors. From June 2020, it launched an online shop selling merchandise, bottled cocktails and food from its RedTail kitchen.

Transformation of businesses will require capabilities that were not created within their models. The instinct to survive in the short term will require businesses to create symbiotic partnerships. This will require some fresh thinking by business leaders.

- Change the “Build” obsession and not try to own every leg of the customer journey. That will not only take time but also distract capital and management.

- Rethink the customer needs – and this time think of the entire journey rather than an inward view of product-market fits. Customer needs are changing at breakneck speeds, so chasing and “building” these “fits” will always remain a common string amongst laggards.

- Connect with like-minded ecosystem players and complement strengths with a single-minded focus on solving customer problems.

- View technology stacks through the lens of your partners. There may be opportunities available from near open source technology solutions.

For example, FJ Benjamin will need the last-mile-delivery capability that will be provided by partners who have optimised in that field, Zouk has tied up with Lazada to host the bazaars and GrabFood is using underutilised taxi capacity to meet the increased demand for food delivery. There are many other examples in the O2O (Offline to Online) space.

This ecosystem approach is also relevant to other sectors like Financial Services. These firms also need to understand the changing consumer needs faster, with a mantra to deliver. Aspire, originally an alternate lending platform has gone through a metamorphosis and transformed into a Neobank. From a uni-product loan provider, it is now solving for a business account, card solution, integration with expense management solutions and continue to provide loans. Capabilities not necessarily built in-house.

The changing world will give rise to business models that will integrate and complement each other. Businesses with an ecosystem mindset will be winners while others might just be relegated to oblivion.

Never before has the world experienced a shutdown in both supply and demand which has effectively slammed the brakes on economic activities and forced a complete rethink on how to continue doing business and maintain social interactions. The COVID-19 pandemic has accelerated digitalisation of consumers and enterprises and the telecommunications industry has been the pillar which has kept the world ticking over.

It is unthinkable just how the human race would have coped with such massive disruption, two decades ago in the absence of broadband internet. The technology and telecom sector has seen a rise in their visible importance in recent months. Various findings show that peak level traffic was about 20-30% higher than the levels before the pandemic. The rise in traffic coupled with the fervent growth of the digital economy augurs well for the technology and telecom sector in Southeast Asia.

Revenues Hit Despite Rise in Traffic

Unfortunately, the rise in network traffic has not translated to an increase in revenue for many operators in the region. The winners, that enjoyed YoY growth in Q1 2020 despite challenging circumstances were: Maxis (4.9%) and DiGi (3.4%) in Malaysia; dtac (3.3%) and True (5.7%) in Thailand; PDLT (7.5%) and Globe (1.4%) in the Philippines; and Indosat Ooredoo (7.9%) and XL Axiata (8.8%) in Indonesia. The telecom operators that struggled include: Celcom (-6.1%) and TM (-8.0%) in Malaysia; Singapore’s trio of Singtel (-6.5%), StarHub (-15.2%) and M1 (-10.3%); and AIS (-1.0%) in Thailand.

Key market trends include a dip in prepaid subscribers due to fall in tourist numbers, roaming income losses due to travel restrictions, and a general decline in average revenue per user (ARPU) due to weaker customer spend. The postpaid customer segment was resilient while the fixed broadband revenue stream was stable due to the increase in work from home (WFH) practices. With fixed tariffs, there are no incremental gains with an increase in usage. Voice revenue has been hit with the increase in collaboration-based communication applications such as Zoom and Microsoft Teams.

Equipment sales fell as global supply chains were severely disrupted and impacted new sign-ups of the more premium customers. Most markets in Southeast Asia depend on retail outlets as a key channel to the market, which has been hampered.

With the job losses across the world, bad debts and weakened customer spend is inevitable and it is imperative that the operators provide for reflective pricing strategies, listen to new customer requirements to ensure customer retention and strengthening of their market position. In May, Verizon’s CEO Hans Vestberg said nearly 800,000 of their subscribers were unable to pay their monthly bills. Discussions with operators in Southeast Asia also highlighted this as a current concern.

Enterprise Segment Target for New Growth

Ecosystm research shows that enterprises in Southeast Asia are increasingly considering telecom operators as go-to-market partners (Figure 1). Enterprises are demanding more than just devices and connectivity and with the fervent digital transformation (DX) efforts underway, services such as managed services, business application services, cybersecurity and network services are in demand. Technology vendors have an opportunity to partner with the right telecom operator in each market to enhance their IT market offerings, ahead of the 5G rollouts.

The broad 5G ecosystem inculcates cross-sector innovation and greater collaboration leading to new business models and exciting new opportunities. Singtel is the leading operator in the region and has the enterprise segment contributing approximately 65% to its revenue in its domestic market. In the World Communications Award 2019, Singtel won both “Best Enterprise Service” and “The Broadband Pioneer” awards. This places Singtel in a fine position to capitalise on the 5G enterprise services.

5G Needed Now More Than Ever

The pandemic has seen a rise in network traffic, onboarding of the digital customer and rapid DX of businesses which has whetted the appetite for faster broadband speeds and new services. Southeast Asia countries stand to profit from the trade war between the US and China and 5G features of low latency and higher security can boost adoption of IoT, Smart Manufacturing and broader Industry 4.0 goals to drive the economy.

Fixed Wireless in Southeast Asia is expected to be very popular considering the low penetration of fibre to the home (with the exception of Singapore) and will provide enterprises with a viable secondary connection to the internet. Popular applications – including video streaming and gaming – which are speed, latency and volume hungry will also be a target market for operators. Mobile operators that do not have a fixed broadband offering can enter this space and provide a serious “wireless fibre” alternative to homes and businesses.

Governments and telecom regulators ought to make spectrum available to the major telecom operators as soon as possible in order to ensure that the cutting edge 5G communications services are made available to consumers and businesses. Many experts believe 5G can raise the competitiveness of a nation.

Recent research from World Economic Forum (WEF) has found that significant economic and social value can be gained from the widespread deployment of 5G networks, with 5G facilitating industrial advances, productivity and improving the bottom line while enabling sustainable cities and communities. GSMA notes that mobile technologies and services in the wider Asia Pacific region generated USD 1.6 trillion of economic value while the mobile ecosystem supported 18 million jobs as well as contributing USD 180 billion of funding to the public sector through taxation.

US-China Trade War Threatens to Change Equipment Supplier Landscape

Despite severe pressures caused by the US-China trade war, Huawei posted an impressive 13.1% YoY growth in 1H 2020 registering revenue of USD 64.88 billion. Both Huawei and ZTE generate approximately 60% of their business from their domestic markets which is critical with the current unfavourable global sentiments. Huawei has diversified its business and built its consumer devices business which should withstand the disruptions caused by the political challenges.

Ericsson and Nokia stand to benefit from Huawei’s current global position and this was evident with the wins for the 5G contracts by Singtel and JVCo (Singtel and M1). The JVCo announced it selected Nokia to build the Radio Access Network (RAN) for the 5G standalone (SA) mmWave network infrastructure in the 3.5GHz radio frequency band. Singtel selected Ericsson to provide for the RAN on the same mmWave network.

However, while there is an opportunity for NEC and Samsung to join the party, Huawei is expected to do well in most other countries in Southeast Asia.

The Rise of the Digital Economy in Southeast Asia

A recent Google report valued the internet economy in Southeast Asia at USD 100 billion in 2019, more than tripling since 2015, and the sector is expected to hit USD 300 billion in 2025. With a population of approximately 570 million people, the region has some of the fastest-growing internet economies in the world.

The Indonesia market is the largest in the region and is expected to hit USD 133 billion from USD 40 billion in 2025. Indonesia’s lack of a world-class telecom infrastructure coupled with their slowness in 5G adoption has not impeded the country’s attractiveness for global technology investors who see the 270 million population as an immense opportunity. US tech giants, Facebook, Google, and PayPal have invested in Indonesia to reap the benefits from the growing digital economy powered by unicorns such as Gojek, Bukalapak, Tokopedia. In June 2020, Google Cloud launched in Jakarta, only the second in the region after Singapore with the four big unicorns being anchor customers.

In 2025, Google predicts Thailand to be the second-largest internet economy worth USD 50 billion. The internet economy for Singapore, Malaysia and the Philippines are estimated to be over USD 27 billion each. Shopee and Lazada are the top eCommerce apps in the region and have seen an increase in sales due to the disruption in the Retail industry. In-store shopping contributes to more than 50% of Retail in Singapore and Malaysia – this provides a tremendous opportunity for eCommerce players.

While movement restrictions are gradually being lifted, some things may never return where they were before COVID-19. Public debts have risen with numerous aids and handouts impacting economic growth forecast and rising unemployment is impacting customer spending power. On the plus side, DX of businesses and sharp onboarding of customers have redefined interactions, and sectors such as Education, are going online which will boost the digital economy. While the challenges are evident, exciting times are ahead for the technology and telecom sector in Southeast Asia.

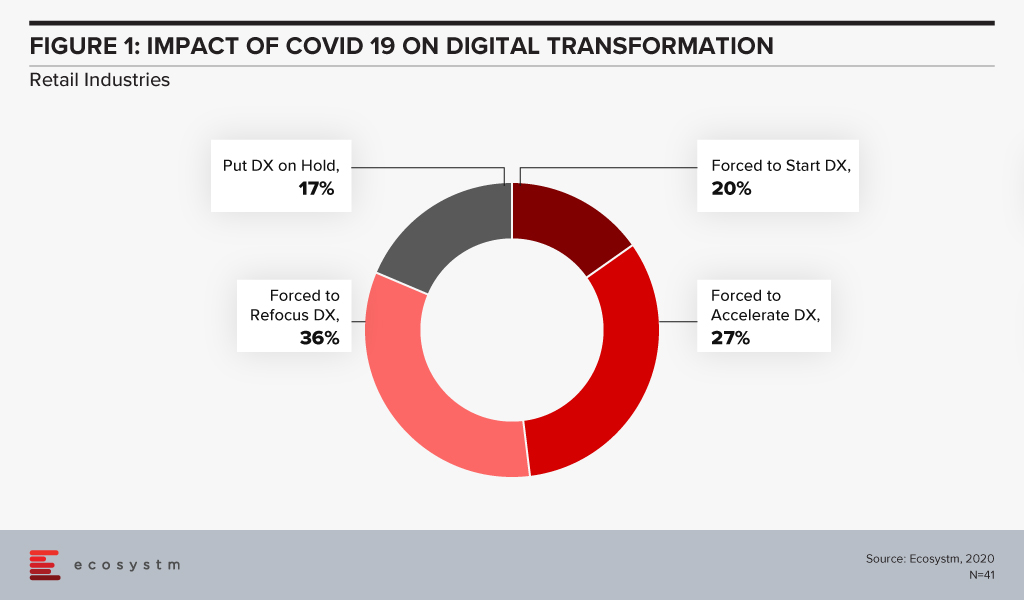

The Retail industry has been one of the hardest-hit industries during the COVID-19 crisis. The industry had to pivot faster than many to cater to an evolving market need and customer expectation, amidst social distancing measures and supply chain disruption. Ecosystm’s Digital Priorities in the New Normal study finds that nearly 83% of organisations in Asia Pacific’s Retail industries were forced to work on digital transformation (DX) in the aftermath of the crisis (Figure 1).

Retail organisations that had not walked the DX path found themselves struggling to cope in recent times. Ecosystm Principal Advisor, Alan Hesketh says, “Digital transformation in retail, as represented by deep customer understanding and omnichannel operations, is far from new. Industry leaders launched these activities almost 20 years ago and continue to aggressively develop these capabilities. Retailers not actively leveraging these capabilities to understand their customer preferences are at a massive competitive disadvantage.”

Anta Group Accelerates DX

The Anta Group, a sports products manufacturer based in China with over 12,500 stores, has launched a group-wide digital platform designed and deployed by IBM Services based on SAP S/4HANA. The initial phase of Anta Group’s DX included creating intelligent workflows and was completed in January 2020. This enabled the company to adjust its retail operations and switch to quickly to online channels during the COVID-19 pandemic.

Like any retail organisation, the Anta Group realised that their product offerings had to be diverse to cater to an evolving customer base. This growth required an upgrade to a group-level management platform to help the business run more efficiently across the entire value chain of procurement, supply, production and sales. The SAP S/4HANA platform gives the senior management a single view of data across business units to help with better decision making regarding production and sales optimisation. The company claims to have improved its supply chain efficiency by 80%, that has led to faster delivery and business growth even in these difficult times.

IBM Services has a role to play in providing the business intelligence required for agile decision-making. By integrating data from multiple sources – retail stores, multi-brand products, channels, customers, suppliers and finance teams – on the one platform can help Anta Group to settle accounts quickly and issue business analysis reports for different entities as well as a real-time view of the operation across the organisation.

Hesketh says, “Retailers must have an accurate, timely understanding of their customers’ behaviour and resulting sales performance. COVID-19 has dramatically increased the volatility of sales, making rapid recognition of changes essential. For those lagging in their digital transformation to acquire this understanding, an attractive option is partnering with organisations with demonstrated relevant capabilities; in this case with SAP, for the capabilities and performance of their in-memory product, and IBM for their configuration and implementation expertise.”

IBM and SAP evolving their partnership

In 2016, IBM and SAP had expressed intentions of increasing investments to help their customers on their DX journeys. As some economies move into the recovery phase, all businesses will be forced to transform – or keep transforming if they are already along that path. Last month saw IBM and SAP announce the evolution of their partnership with new offerings to help businesses transform faster. The next evolution of the IBM and SAP partnership aims to focus on faster DX time to value, innovation through industry-specific offerings, customer and employee experiences and providing flexibility and choice to organisations to run their workloads in hybrid cloud environments.

Hesketh adds, “But the product and implementation partners are, while important, not the real determinant of the success of DX activity and time to value. Retailers must recognise and commit to the strategic reshaping of their business, taking their large workforces with them on the journey. This is a high-risk change. A strong relationship between product vendor and implementation partner, as SAP and IBM demonstrate here, assists in reducing, not removing, this risk.”

2020 has seen extreme disruption – and fast. The socio-economic impact will probably outlast the pandemic, but several industries have had to transform themselves to survive during these past months and to walk the path to recovery.

Against this backdrop, the Retail industry has been impacted early due to supply chain disruptions, measures such as lockdowns and social distancing, demand spikes in certain products (and diminished demands in others) and falling margins. Moreover, it is facing changed consumer buying behaviour. In the short-term consumers are focusing on essential retail and conservation of cash. The impact does not end there – in the medium and long term, the industry will face consumers who have acquired digital habits including buying directly from home through eCommerce platforms. They will expect a degree of digitalisation from retailers that the industry is not ready to provide at the moment. This raises the question on how they should transform to adapt to the New Normal and what could be a potential game-changer for them.

Translating Business Needs into Technology Capabilities

In his report, The Path to Retail’s New Normal, Ecosystm Principal Advisor, Kaushik Ghatak says, “Satisfying their old consumers, now set in their new ways, should be the ‘mantra’ for the retailers in order to survive in the New Normal.” To be able to do so they have to evaluate what their new business requirements are and translate them into technological requirements. Though it may sound simple, it may prove to be harder than usual to identify their evolving business requirements. This is especially difficult because even before the pandemic, the Retail industry was challenged with consumers who are becoming increasingly demanding, providing enhanced customer experience (CX), offering more choices and lowering prices. The market was already extremely competitive with large retailers fighting for market consolidation and smaller and more nimble retailers trying to carve out their niche.

In the New Normal, retailers will struggle to retain and grow their customer base. They will also have to focus aggressively on cost containment. A robust risk management process will become the new reality. But above all else, they will have to innovate – in their product range as well as in their processes. These are all areas where technology can help them. This can come in the form of technology partnerships, adopting hybrid models, increased usage of technology across all channels and investing in reskilling or upskilling the technology capabilities of employees.

Re-evaluating the Supply Chain

One of the first business operation to get disrupted by the current crisis was the supply chain. Ecosystm Principal Advisor, Alea Fairchild says, “Retailers are finding themselves at the front-end of the broken supply chain in the current situation and there is an enormous gap between suppliers and buyers. Retailers will have to aim to combine inventory with local sourcing and become agile and adopt change quickly. This will highlight to them the importance of transparency of information, traceability, and information flow of goods.”

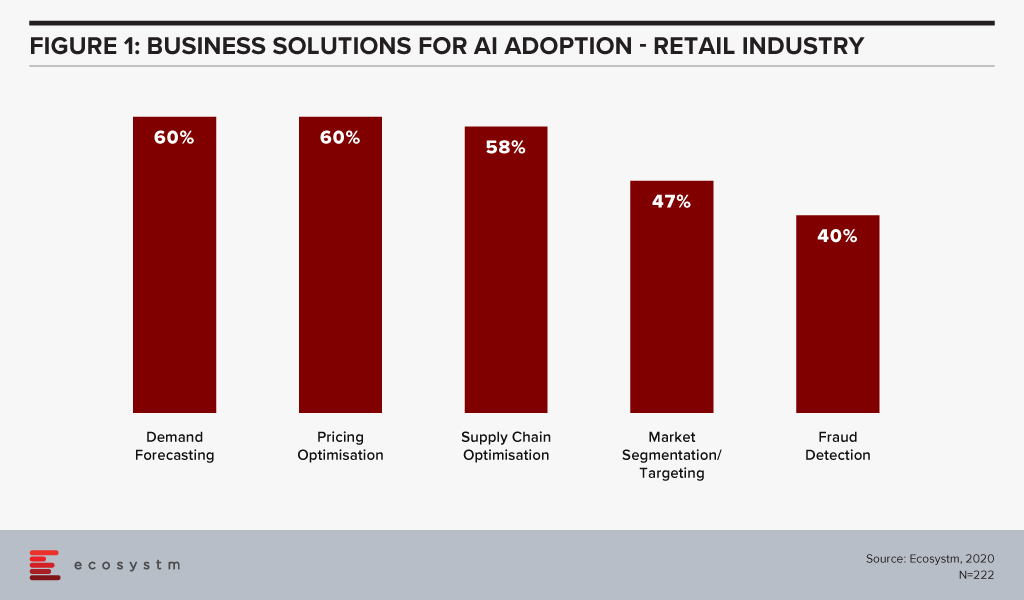

Ecosystm research shows that supply chain optimisation and demand forecasting among the top 5 business solutions that firms in Retail consider using AI for (Figure 1).

“In the New Normal, consumers are going to demand the same level of perfection that they have received and at the same cost. In order to make that possible, at the right time and at a lower cost, automation has to be implemented to improve the supply chain process, fulfill expectations and enhance visibility,” says Ghatak. “Providing differentiated CX is intimately dependent upon an aligned, flexible and efficient supply chain. Retailers will not only need to innovate at the store (physical or online) level and offer more innovative products – they will also need to have a high level of innovation in their supply chain processes.”

Digital Transformation in the Retail Industry

Ecosystm research reveals that only about 34% of global retailers had considered themselves to be digital-ready to face the challenges of the New Normal, before the pandemic. The vast majority of them admit that they still have a long way to go.

With COVID-19, the timeframes for digitalisation have imploded for most retailers. The study to evaluate the Digital Priorities in the New Normal reveals that in Asia Pacific nearly 83% of retailers have been forced to start, accelerate or refocus their Digital Transformation (DX) initiatives (Figure 2).

![]()

So, what technology areas will Retail see increased adoption oF?

Fairchild sees retailers adopt IoT, mobility, AI and solutions that deliver personalised experiences such as push notifications. What they are likely to do is blend different aspects of their physical and virtual environment to create a solution for customers. “To address in-store processing, hygiene, safety standards and compliance requirements, retailers will change their processes through a combination of resources, KPIs, automation, task management software and switching the information flow.”

Ghatak thinks automation has a significant role to play in improving both CX and the supply chain. “This is also an opportunity for retailers – both online and in-store – to create a solution experience where technologies such as Augment/Virtual Reality (AR/VR) can help. While retailers are adopting these technologies, with 5G rollouts, there is potential that the adoption will implode in a short time-frame.”

Those retailers that are not re-evaluating their business models and technology investments now will find themselves unprepared to handle the customer expectations when the global economy opens up.

The telecommunications industry has long been an enabler of Digital Transformation (DX) in other industries. Now it is time for the industry to transform in order to survive a challenging market, newer devices and networking capabilities, and evolving customer requirements. While the telecom industry market dynamics can be very local, we will see a widespread technology disruption in the industry as the world becomes globally connected.

Drivers of Transformation in the Telecom Industry

Remaining Competitive

Nokia Bell Labs expects global telecom operators to fall from 10 to 5 and local operators to fall from 800 to 100, between 2020 and 2025. Simultaneously, there are new players entering the market, many leveraging newer technologies and unconventional business models to gain a share of the pie. While previous DX initiatives happened mostly at the periphery (acquiring new companies, establishing disruptive business units), operators are now focusing on transforming the core – cost reduction, improving CX, capturing new opportunities, and creating new partner ecosystems – in order to remain competitive. There is a steady disaggregation in the retail space, driving consolidation in traditional network business models.

“The telecom industry is looking at gradual decline from traditional services and there has been a concerted effort in reducing costs and introducing new digital services,” says Ecosystm Principal Advisor, Shamir Amanullah. “Much of the telecom industry is unfortunately still associated with the “dumb pipe” tag as the over-the-top (OTT) players continue to rake in revenues and generate higher margins, using the telecom infrastructure to provide innovative services.”

Bringing Newer Products to Market

Industries and governments have shifted focus to areas such as smart energy, Industry 4.0, autonomous driving, smart buildings, and remote healthcare, to name a few. In the coming days, most initial commercial deployments will centre around network speed and latency. Technologies like GPON, 5G, Wifi 6, WiGig, Edge computing, and software-defined networking are bringing new capabilities and altering costs.

Ecosystm’s telecommunications and mobility predictions for 2020, discusses how 5G will transform the industry in multiple ways. For example, it will give enterprises the opportunity to incorporate fixed network capabilities natively to their mobility solutions, meaning less customisation of enterprise networking. Talking about the opportunity 5G gives to telecom service providers, Amanullah says, “With theoretical speeds of 20 times of 4G, low latency of 1 millisecond and a million connections per square kilometre, the era of mobile Internet of Everything (IoE) is expected to transform industries including Manufacturing, Healthcare and Transportation. Telecom operators can accelerate and realise their DX, as focus shifts to solutions for not just consumers but for enterprises and governments.”

Changing Customer Profile

Amanullah adds, “Telecom operators can no longer offer “basic” services – they must become customer-obsessed and customer experience (CX) must be at the forefront of their DX goals.” But the real challenge is that their traditional customer base has steadily diverged. On the one hand, their existent retail customers expect better CX – at par with other service providers, such as the banking sector. Building a customer-centric capability is not simple and involves a substantial operational and technological shift.

On the other hand, as they bring newer products to market and change their business models, they are being forced to shift focus away from horizontal technologies and connecting people – to industry solutions and connecting machines. As their business becomes more solution-based, they are being forced to address their offerings at new buying centres, beyond IT infrastructure and Facilities. Their new customer base within organisations wants to talk about a variety of managed services such as VoIP, IoT, Edge computing, AI and automation.

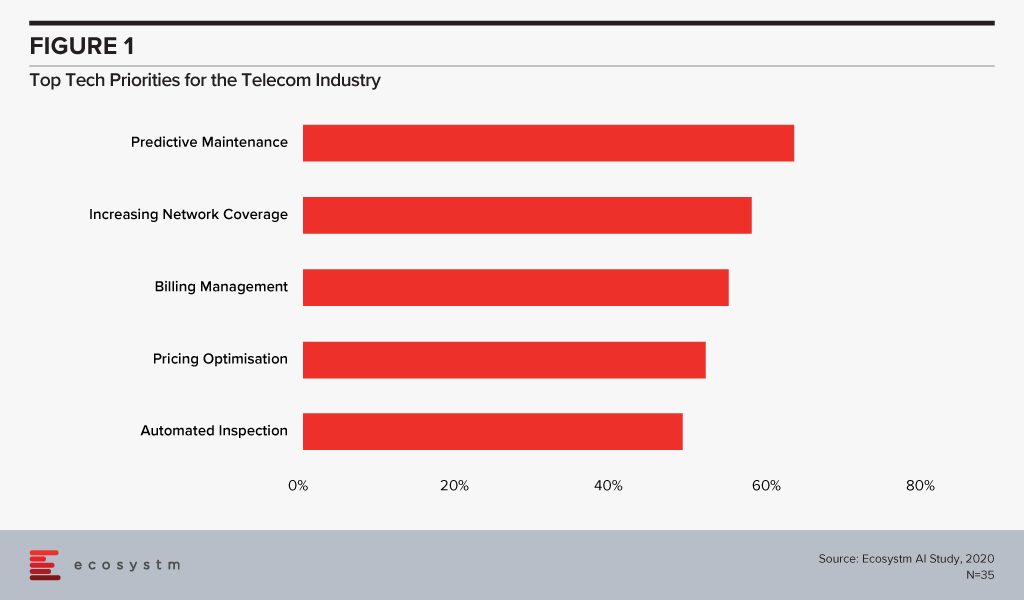

The global Ecosystm AI study reveals the top priorities for telecom service providers, focused on adopting emerging technologies (Figure 1). It is very clear that the top priorities are driving customer loyalty (through better coverage, smart billing and competitive pricing) and process optimisation (including asset maintenance).

Technology as an Enabler of Telecom Transformation

Several emerging technologies are being used internally by telecom service providers as they look towards DX to remain competitive. They are transforming both asset and customer management in the telecom industry.

IoT & AI

Telecom infrastructure includes expensive equipment, towers and data centres, and providers are embedding IoT devices to monitor and maintain the equipment while ensuring minimal downtime. The generators, meters, towers are being fitted with IoT sensors for remote asset management and predictive maintenance, which has cost as well as customer service benefits. AI is also unlocking advanced network traffic optimisation capabilities to extend network coverage intelligently, and dynamically distribute frequencies across users to improve network experience.

Chatbots and virtual assistants are used by operators to improve customer service and assist customers with equipment set-up, troubleshooting and maintenance. These AI investments see tremendous improvement in customer satisfaction. This also has an impact on employee experience (EX) as these automation tools free workforce from repetitive tasks and they be deployed to more advanced tasks.

Telecom providers have access to large volumes of customer data that can help them predict customer usage patterns. This helps them in price optimisation and last-minute deals, giving them a competitive edge. More data is being collected and used as several operators provide location-based services and offerings.

In the end, the IoT data and the AI/Analytics solutions are enabling telecom service providers to improve products and solutions and offer their customers the innovation that they want. For instance, Vodafone partnered with BMW to incorporate an in-built SIM that enables vehicle tracking and provides theft protection. In case of emergencies, alerts can also be sent to emergency services and contacts. AT&T designed a fraud detection application to look for patterns and detect suspected fraud, spam and robocalls. The system looks for multiple short-duration calls from a single source to numbers on the ‘Do Not Call’ registry. This enables them to block calls and prevent scammers, telemarketers and identity theft issues.

Cybersecurity

Talking about the significance of increasing investments in cybersecurity solutions by telecom service providers, Amanullah says, “Telecom operators have large customer databases and provide a range of services which gives criminals a great incentive to steal identity and payment information, damage websites and cause loss of reputation. They have to ramp up their investment in cybersecurity technology, processes and people. A telecom operator’s compromised security can have country-wide, and even global consequences. As networks become more complex with numerous partnerships, there is a need for strategic planning and implementation of security, with clear accountability defined for each party.”

One major threat to the users is the attack on infrastructure or network equipment, such as routers or DDoS attacks through communication lines. Once the equipment has been compromised, hackers can use it to steal data, launch other anonymous attacks, store exfiltrated data or access expensive services such as international phone calls. To avoid security breaches, telecom companies are enhancing cybersecurity in such devices. However, what has become even more important for the telecom providers is to actually let their consumers know the security features they have in place and incorporate it into their go-to-market messaging. Comcast introduced an advanced router to monitor connected devices, inform security threats and block online threats to provide automatic seamless protection to connected devices.

Blockchain

Blockchain can bring tremendous benefits to the telecom industry, according to Amanullah. “It will undeniably increase security, transparency and reduce fraud in areas including billing and roaming services, and in simply knowing your customer better. With possibilities of 5G, IoT and Edge computing, more and more devices are on the network – and identity and security are critical. Newer business models are expected, including those provided for by 5G network slicing, which involves articulation in the OSS and BSS.”

Blockchain will be increasingly used for supply chain and SLA management. Tencent and China Unicom launched an eSIM card which implements new identity authentication standards. The blockchain-based authentication system will be used in consumer electronics, vehicles, connected devices and smart city applications.

Adoption of emerging technologies for DX may well be the key to survival for many telecom operators, over the next few years.

As the ‘Experience Economy’ becomes a reality, organisations will look beyond improving customer experience (CX) to enhancing employee experience (EX). It is estimated that people spend a third of their life at their workplaces. This realisation will drive organisations to focus on EX over priorities such as growing revenue or reducing costs. Retaining employees is important in today’s war for talent – and organisations have started appointing Chief Experience Officers. Ultimately, workplace technology should drive employee productivity – and there is a proven link between happy and productive employees.

The Top 5 Workplace Of The Future Trends For 2020

The Top 5 Workplace of the Future trends are drawn from the findings of the global Ecosystm CX Study and are also based on qualitative research by Ecosystm Principal Advisors, Tim Sheedy and Audrey William.

-

Employee Experience as a Business Focus Will Drive Faster Adoption of Consumer Collaboration Tools

Organisations in mature economies already have employee experience (EX) and CX as their top business priorities. This comes with an understanding that offering a great customer and employee experience will lead to revenue growth, profit growth and lower costs.

For communication and collaboration solutions, if the experience is not right, employees will move on to the next best app for the right experience. The competition between the vendors across voice, video and collaboration is heightening. It may sound simple but that is where the innovation needs to happen in the industry. If employees do not like what IT has provided for them, they will download the application of their choice for work. This will be a huge challenge especially in industries that are heavily regulated such as Financial Services and Healthcare.

-

HR KPIs Will Drive IT Teams to Invest in Workplace Analytics

HR teams are ultimately responsible for driving improved EX. And a happy employee is a productive employee – so an employee’s environment (managed by the Operations or Facilities team) and their technology (managed by the IT team) will have the biggest impact on driving employee satisfaction. To drive these outcomes, we will see these three teams work closer than they ever have – and not just on a project basis, but as a permanent arrangement.

Investments in Workplace Analytics will increase, and there will be more collaboration between IT, HR and Facilities Management to drive best practices for employees. Right now, there is very little collaboration between the three departments in driving better workplace practices. Workplace Analytics will help solve problems related to poor office practices around email overload, long work hours, absenteeism, usage of rooms and other facilities, employee discontent, as well as understand the overall trends on communications and collaboration solutions usage.

-

5G Services will Push Organisations to Rethink their Network

Today 5G is not available in many countries – and where it is available coverage is generally spotty. But this will change in 2020 as more operators launch or expand their 5G coverage. The unique capabilities of 5G to offer software-defined networks (SDNs) – designed specifically for organisations’ needs – will help businesses rethink the way they operate. They can stop thinking of their network as a physical place and start thinking of it as a set of capabilities and this takes work beyond designated physical addresses. Retailers will be able to offer complete retail environments from wherever they choose. Banks will be able to offer complete in-branch services from anywhere. Employees will be able to get access to all sorts of data and systems regardless of location. 5G is about much more than a faster network – the potential to transform enterprise networks will see a huge rethink of the network and the way IT teams provide technology services to their employees.

-

Organisations Will Wake Up to the Need for the Right Knowledge Management Solution

IT has been guilty of dictating the knowledge management (KM) requirements and platforms to the business. Many customer teams are using tools that are inherently wrong for the job. Management is using tools that do not support their needs, and information workers are given generic platforms when they have specific needs. 2020 will see a fragmentation of the KM market as businesses start to buy based on customer and employee needs – not based on what the IT team dictates.

-

2020 Will See a Rise in CPaaS Adoption

Cloud-based platforms that enable developers to add real-time communications features within the workflow of their own business applications will be the next big area of innovation in the unified communications space. Through the use of APIs, developers can embed communication capabilities into their existing business applications, without extra hardware or software costs. Developers can embed it directly into the cloud platform so the time to market is fast. Communications Platform as a Service (CPaaS) will see greater adoption as more organisations look to build code and apply agile and DevOps methodologies.

Download Report: The top 5 Workplace of the future trends for 2020

The full findings and implications of the report ‘Ecosystm Predicts: The Top 5 Workplace of the future Trends for 2020’ are available for download from the Ecosystm platform. Signup for Free to download the report and gain insight into ‘the top 5 Workplace of the future trends for 2020’, implications for tech buyers, implications for tech vendors, insights, and more resources. Download Link Below ?

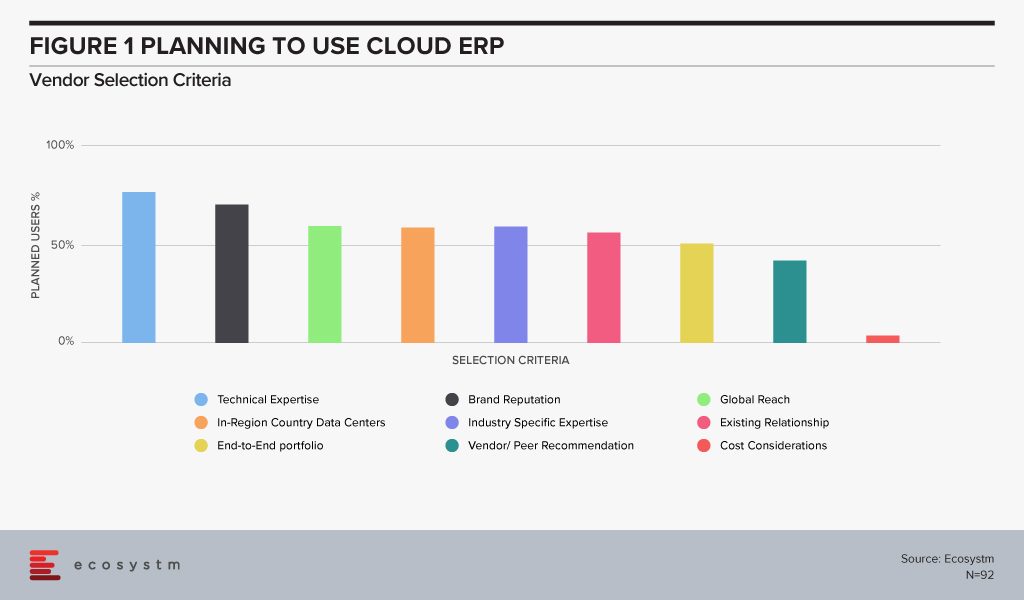

ERP serves as an important component that connects various business operations and verticals in an organisation. As a part of digital strategy, many organisations have started adopting digital tools and technologies where an Enterprise Resource Planning (ERP) solution is one of the primary components. ERP was originally applied to manufacturing systems, but today it describes the software at the core of an organisation’s business, without which it could not function.

ERP software has evolved significantly since it first came into widespread existence in the 1980s. Major vendors like SAP and Oracle offer sophisticated suites of software that integrate several functions. Other vendors offer ‘best-of-breed’ applications optimised for a particular purpose or market segment. The implementation, maintenance and efficient management of ERP software is a large industry in its own right. ERP services companies are a major part of the global ICT industry.

Enterprise applications are core to the business

All enterprises run core application software essential to their business. These include financial software and applications like human resources/human capital management (HR/HCM) and customer relationship management (CRM). They also typically run mission-critical applications like manufacturing, distribution and logistics and others, depending on their vertical market sector. ERP better integrates various business units and data flowing in departments such as backend office operations, accounting, inventory management and finance management throughout an organisation.

Some of the industries benefitting from ERP include banks and insurance companies that run vast client databases, manufacturers running sophisticated production and asset management systems, retailers, government agencies, educational institutions, transport companies – organisations in every market sector – run specialised applications that enable them to efficiently run and manage their operations.

Cloud transforming ERP

Like all applications, ERP systems are increasingly becoming cloud-based, or use cloud infrastructure for much of their functionality. Today, almost all the major vendors are migrating their product offerings to the cloud, using the SaaS (Software-as-a-Service) model.

As ERP migrates to the cloud it is changing the business models of both vendors and user organisations. It is also affecting the ERP services market. The global Ecosystm study on Cloud ERP Solutions – Best Practices and Vendor Selection finds that organisations which are planning to use Cloud ERP solutions prioritise industry expertise and local presence of data centres as a significant selection criterion for vendors.

Cloud computing encourages a pay-per-use subscription model for ERP and other applications which are changing the structure of the industry. Users are moving their budgets from the CapEx (capital expenditure) to the OpEx (operational expenditure) model, where outgoings are better able to be varied according to use.

A giant, mission-critical matrix

ERP is referred to as ‘mission-critical’ applications for a very good reason. An organisation’s core business functions are non-negotiable and without them, the organisation will cease to function. In addition, they need to be robust and flexible and capable of meeting the demands of changing technologies, economics and business conditions.

In this increasingly connected world, ERP extends beyond the enterprise. Modern ERP systems are interconnected in a giant business matrix that enables a world of global commerce. ERP systems support multiple interfaces and act as a modular system to any organisations demands. Their importance to the global business should not be underestimated.

While talking about the paradigm shift that we are seeing in the industry today, I like to use the analogy of space exploration. The aim is to make space an extension of the earth through its use in communication, tourism and for mineral exploration. This is an entirely new paradigm on how all the investments in space technology and transportation are being made – by private industries as well as by governments of major economies.

Similarly, technology is no longer a business enabler – it is now a catalyst to create and capture new value streams and to create sustainable differentiation. The relationship between customers and enterprises is now a two-way street. Customers are not just using products and services but feeding information and critical insights back to the enterprises on a real-time basis. Now, even B2B enterprise businesses must be seen more as a B2B2C.

This new paradigm has brought technology to the core of every business and is forcing enterprises to transform the way they run their businesses.

The Multiplier Effect

Enterprises have to look at technology with a fresh new lens now. So far, they have had to cope with any emerging technology in isolation. Now they are being hit by a number of technologies – agile network, cloud, data analytics, intelligent technologies – each of which has its impact. But what makes it transformational is the interplay of these technologies. Big Data analytics, AI and IoT has taken in isolation can definitely impact an organisation. But when the three work together, they have an exponential impact on an organisation and on it’s Digital Transformation (DX) journey. This has two clear impacts on businesses.

Impact on Enterprises

Expanding Role of Business Functions. As organisations embark on their DX journeys, they are likely to increase technology spend. Even though some budget would go into upgradation of IT infrastructure, a larger portion of the budget is likely to go towards digitisation, business applications, cybersecurity, and intelligent technologies. These projects would require the involvement of multiple stakeholders. And consequently, a higher proportion of technology spend will be controlled by the business functions – and this proportion will only get. Let us take AI as an instance. The global Ecosystm AI Study shows that only about a fifth of AI projects now are being funded by IT. Multiple other stakeholders are involved in emerging technology projects – the key department being where the solutions are being deployed.

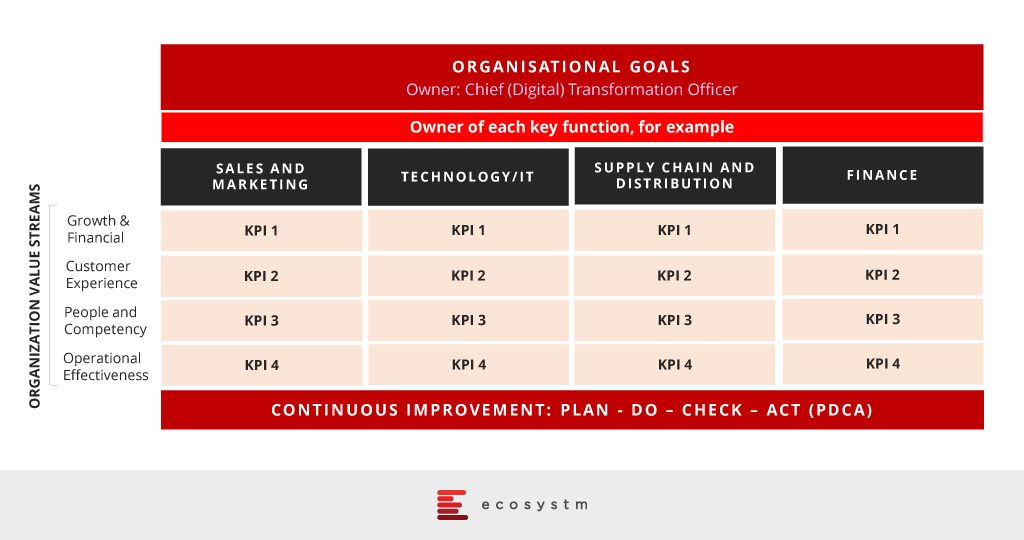

Building a Transformation Roadmap. Ad-hoc implementation of technology will no longer be a viable option. What enterprises will need is an interdisciplinary model of work to attain the most value out of their transformation through technology. This should lead to a clear roadmap – that melds technological capabilities with business requirements. And mind you, each organisation’s roadmap will be distinct and unique.

Wider organisational functions will have to be engaged and aligned. Managing budgets and new business models simultaneously comes with a set of its own complexities. In my opinion, a Balanced Scorecard and Lean Approach is the way ahead for organisations as they approach Transformation.

Irrespective of the size of your organisation, you have to focus on the three main building blocks necessary to implement transformation:

- Defining measurable business objectives that are aligned with the organisational goals and aspirations

- Assigning transformation owners for each of the key functions identified for Transformation

- Using structured program management using Lean principle and the Balanced Score Card approach

Understandably, an interdisciplinary model of work and a structured program may not be easy to implement. I discuss the complexities of introducing the new wave of technology in my report.

If your organisation is embarking on a DX journey or if you wish to discuss your ongoing DX roadmap, leave a comment below or connect with me on the Ecosystm platform.