Microsoft announced their intentions to acquire Activision Blizzard for USD 68.7 billion, creating quite a buzz in the Gaming and tech industry. The acquisition is set to be completed in 2023 and according to Microsoft is well set to fuel “growth in Microsoft’s gaming business across mobile, PC, console and cloud and will provide building blocks for the metaverse.”

There have been a few animated discussions at Ecosystm on Microsoft’s potential monopoly in the Gaming industry, whether it is aligned to their ‘Metaverse plans’ and the challenges that Microsoft is likely to face with the acquisition. Here is what our experts have to say.

Impact on the Gaming Industry

Activision Blizzard is the publisher of some of the most popular games around – loved by both hardcore and casual gamers. The acquisition of franchises such as Call of Duty, Overwatch, Warcraft and Diablo – as well as mobile games like Candy Crush and Hearthstone – demonstrates Microsoft’s commitment to what is now the largest medium of entertainment.

Microsoft is clearly focusing on growing their software revenue. But most importantly, they will be able to integrate these popular titles within Game Pass. This allows them to compete more actively with Steam and Epic Games Store but as a subscription-based model. The Game Pass model has proven extremely popular with gamers (with approximately 25 million gamers spending USD 10 per month to subscribe to the service), so this will continue to bolster their market position and increase users and revenue.

The latest Xbox Series X/S are the fastest-selling Xboxes ever – even with chip shortages and logistics challenges. The majority of Microsoft’s gaming revenue comes from hardware now. This acquisition will inevitably drive hardware growth, as well as increase gaming software revenue from both a subscription on Game Pass as well as outright purchases.

Microsoft’s Bigger Play

Microsoft made a great start by acquiring key titles like Doom in 2020. The go-to-market strategy through subscriptions and gaming as a cloud service is well managed. Last year when Microsoft relaunched Flight Simulator, the Ecosystm review spoke of how Microsoft wanted to be the “Netflix of Gaming”. They just fired another big shot in that battle by announcing their intention to acquire Activision. With a USD 69 billion price tag, it is probably more of a ballistic missile than a shot!

There has been a lot of conversation (including at Ecosystm!) on how this acquisition makes sense. Microsoft’s revenue from gaming sales is said to be USD 11.5 billion on an annualised basis – and Activision’s revenue is estimated to be USD 7.7 billion. The combination will obviously be huge, but is it worth so much? It is!

The reason for that is today’s leading buzzword – the Metaverse. As people live more of their lives in an online world and interact more with their peers online, being a leader in that “universe” is the key to the future. The Metaverse occupies the spaces of work, play and socialisation which have all gone increasingly virtual.

For Microsoft, this really translates into how relevant their cloud is to the Metaverse. This is a world where one can play using Game Pass, work on Office 365 and store everything on OneDrive. This pervasiveness is key to Microsoft’s consumer strategy. On the enterprise side, they have a dominant share, especially with Office 365. This will see them gaining strength in the consumer business.

Challenges for Microsoft

What a bargain for Microsoft! When Microsoft made the USD 95 per share offer this week Activision’s market value was about USD 51 billion. While the premium that they are offering was almost 50% of the share market close on the previous trading day, they are getting market-leading content for about 10% less than what Activision was worth in February 2021. A year in which the pandemic continued to increase demand for online gaming.

However, this leaves Microsoft with three significant challenges.

First, they have to get regulatory approval in the different markets in which the two companies operate. Microsoft has advised they expect the deal to close in late 2023, so it looks like they are expecting some interesting discussions over the next few months. This acquisition is a significant consolidation of the Gaming market, so regulators will look at the deal closely.

In addition, regulators will also look closely at the privacy implications, with Microsoft gaining access to millions of gamers’ personal details to add to the personal information they already hold from their other divisions.

Second, they have the challenge of addressing the sexual harassment issues that caused the drop in Activision’s market value. There are court settlements under appeal, and reports talk about 40 people leaving Activision since July. Integrating the large teams into Microsoft will need careful attention.

Third, retaining the talent in Activision may be a challenge for Microsoft as I would expect their competition to be actively approaching Activision’s key creatives.

Unless these challenges are handled well, the company they bid on may not be the company they acquire.

A decade ago, the axiom of a successful business model was to identify a need, find the market and then develop an idea or product that fits into that chain. It was a process of inserting a product in the customer’s already existing experience journey with the hope that the product/idea would deliver efficiency to the client. This efficiency could be financial, operational, marketing or cost savings – the uni-product, uni-feature approach.

There has been enough said about the many companies that failed to innovate beyond their existing product/feature and failed to stay ahead of the game. Nokia and Blackberry remain at the centre of any discussion about “lack of innovation”. There are others like Kodak, Canon, Napster, Palm, Blockbuster – that were devoured by innovative competitors.

The predators were ones with the vision to see the entire value chain and not just their own product. Netflix created content and distributed it, Apple touched the lives of their customers in multiple ways and AirBnb provided accommodation inventory, choice and booking all in one. The new secret sauce is to provide the customer with an ecosystem and not a product!

The Need to Transform

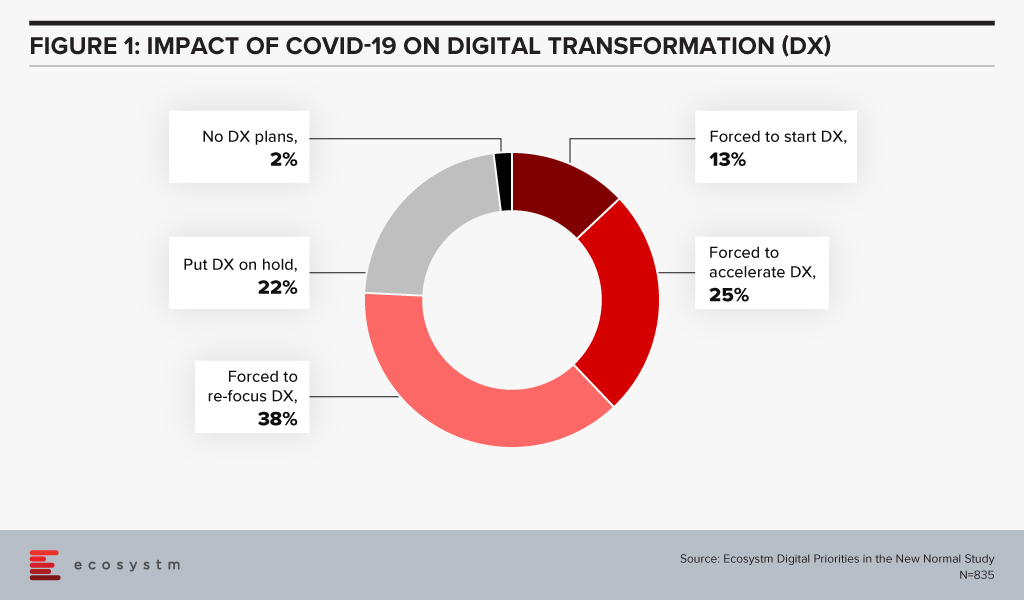

Cut to the COVID era – there are many businesses facing the downturn and experiencing the “moments of truth” giving rise to a desperate attempt to innovate, transform, survive, and come out as the rising stars. Ecosystm research finds that 98% of organisations have re-evaluated their Transformation roadmap (Figure 1), while 75% have started, accelerated or refocused their DX initiatives.

New business models are evolving, and accelerating digitalisation is the result. The digital movement, be it in food delivery or payments, is here to stay. This digital acceptance and absorption exaggerate the need for business models that capture holistic ecosystems and entire customer journeys, due to reasons that separate the hunter and the hunted.

- Margins will never be the same again as in the uni-product model. Using the F&B analogy; with the increasing number of customers wanting to dine in the comfort of their homes, restaurants cannot use ambiance as the price differentiator. Since most restaurants are available on food delivery services, customers are getting brand agnostic. This is the start of commoditisation of dining. Restaurants (or food caterers now!) will need to play the price card to remain competitive resulting in compressed margins. The food delivery market is expected to grow 4-fold to USD 8 billion by 2025 but with lower margins. This example of the food delivery model will be the same as experienced by retail, apparel and other industries.

- Customer experience will still be the differentiator and lever for loyalty and repeat purchase. Factors like proximity, parking, in-store experience, and store layout are fast getting replaced by the ease of navigation, user experience, seamless check out and finally efficient and timely delivery. The ease of transaction including multiple steps of search, assessment, evaluation, payment and delivery is of paramount importance. Customers do not want fractured journeys with multiple drop-offs. A unified seamless journey will win.

- Virtual, Digital and Automation are the three mantras that management consultants are betting on. However, this trilogy will not guarantee survival since the road to recovery is not a straight one. Different work schedules, observing various curves and on what point of the curve the business, its customer and the market are at, will add to the complexity of decision making and transformation.

Given the above, an obvious strategy to beat the existential crisis is to transform and seek out sustainable operating models. However, it may not be so simple since most businesses may not be able to change models as quickly as needed. There is an inherent cost to change since the existing processes and procedures have been well oiled and smoothed over time. The much-needed change requires the infusion of the 3Ts (time, technology, training) and associated costs. Most often, there is an inverse correlation noticed between the sturdiness of the business and its ability to be flexible to change. Businesses that are “rock-solid” and profitably sturdy and stable, have high inertia of transformation versus FinTech businesses, as an example, that pride themselves with nimble operations but are financially fragile and may not be able to absorb the cost of speedy transformation.

This Sturdy-Flexible continuum is the tight rope walk that businesses will need to walk in this need for transformation. Businesses that embark on this walk alone will find it extremely painful and lonely. Especially in the case of small business owners who are scared and low on all 3Ts.

The Rise of Ecosystems

The new world has manifested that businesses that use physical space or assets as their competitive advantage are more prone to be impacted. Retail, Education, Hospitality and Entertainment are some obvious examples that have been impacted by the physicality in their propositions. Digital businesses are more agile but have suffered in their inability to scale up in time to capture the increased demand.

Fashion retailer FJ Benjamin has decided to shut 300 physical stores and rely on online sales. This strategy also helps to utilise precious time to scale diversification. Other retailers too have been going down the FJ Benjamin path and ramping up eCommerce as this trend is expected to stick beyond COVID-19.

Zouk, the renowned nightclub with 30,000 square feet of space in Singapore uses this venue as a live streaming venue during the day to host bazaars for eCommerce vendors. From June 2020, it launched an online shop selling merchandise, bottled cocktails and food from its RedTail kitchen.

Transformation of businesses will require capabilities that were not created within their models. The instinct to survive in the short term will require businesses to create symbiotic partnerships. This will require some fresh thinking by business leaders.

- Change the “Build” obsession and not try to own every leg of the customer journey. That will not only take time but also distract capital and management.

- Rethink the customer needs – and this time think of the entire journey rather than an inward view of product-market fits. Customer needs are changing at breakneck speeds, so chasing and “building” these “fits” will always remain a common string amongst laggards.

- Connect with like-minded ecosystem players and complement strengths with a single-minded focus on solving customer problems.

- View technology stacks through the lens of your partners. There may be opportunities available from near open source technology solutions.

For example, FJ Benjamin will need the last-mile-delivery capability that will be provided by partners who have optimised in that field, Zouk has tied up with Lazada to host the bazaars and GrabFood is using underutilised taxi capacity to meet the increased demand for food delivery. There are many other examples in the O2O (Offline to Online) space.

This ecosystem approach is also relevant to other sectors like Financial Services. These firms also need to understand the changing consumer needs faster, with a mantra to deliver. Aspire, originally an alternate lending platform has gone through a metamorphosis and transformed into a Neobank. From a uni-product loan provider, it is now solving for a business account, card solution, integration with expense management solutions and continue to provide loans. Capabilities not necessarily built in-house.

The changing world will give rise to business models that will integrate and complement each other. Businesses with an ecosystem mindset will be winners while others might just be relegated to oblivion.