We are in the midst of an economic and social crisis. COVID-19 will have far-reaching effects on organisations and how they do business. It is expected to drive more investments in Fintech, especially in digital payments, as more organisations and consumers adopt eCommerce. Countries will also have to re-think the ways they trade with other countries, as travel restrictions continue. This is expected to boost the Fintech industry and July was witness to how Fintech organisations, financial institutions and governments are gearing up to leverage Fintech in their path to economic and social recovery.

Financial Industry Seeing More Open Banking Initiatives

The banking industry is fast moving towards collaboration and openness. July saw several initiatives that take the industry closer to open banking.

Late last year, South Korea piloted an open banking system with participation from local banks and lenders. The Financial Services Commission (FSC), South Korea’s top financial regulator reported in July that the initiative had participation from 72 companies including commercial banks and Fintech firms with 20 million subscribers using the open banking services.

Australia introduced an open banking initiative, monitored by the Australian Competition and Consumer Commission (ACCC). From July, Australia’s banking customers can share their financial and banking data with accredited businesses under Consumer Data Right Act to access a better suite of financial applications.

There is global expansion as well. Railsbank, a global open banking platform with a presence in Southeast Asia introduced their services in the US market. The company will offer Banking-as-a Service, Cards-as-a Service and Credit Card-as-a-Service in the US market. Khaleeji Commercial Bank (KHCB), an Islamic bank in Bahrain, launched their open banking service enabling a customer to link their bank accounts with other banks and manage through the ‘Khaleeji 360’ platform. The portal allows clients to view all their bank accounts, automate operations and conduct banking through a unified platform.

Financial Institutions Increasing Partnerships with Fintech

Financial institutions no longer look at Fintech as competition. They appreciate that customers are at the centre of their entire operation – and Fintech services can and will provide them with the solutions they need. As financial institutions re-think their transformation journeys and face increasingly stringent regulations, they no longer have the option of ignoring Fintechs.

American Express, Visa, Mastercard and Discover came together to roll out a global standard. The big four’s advanced digital checkout solution Click to Pay is an online checkout system based on EMV Secure Remote Commerce (SRC) to make online payments across websites, mobile applications and connected devices, frictionless.

With an aim to unify payment solutions, a group of 16 major European banks launched the European Payment Initiative (EPI) to create a unified pan-European payment solution leveraging Instant Payments/SEPA Instant Credit Transfer (SCT Inst), including a card, e-wallet and P2P payments.

We also saw financial institutions strengthen their cross-border payment services in July. Deutsche Bank partnered with Airwallex to offer virtual account collections and API-enabled foreign exchange services in Japan and Hong Kong. The service will enable merchants and traders to transact through virtual accounts and APIs without opening bank accounts in foreign markets. Mastercard and Bank of China partnered to enhance cross-border business payments into China. This will enable global businesses to send payments to China while accessing real-time exchange rates, reduce the need for unnecessary documentation between merchants, and reduce transaction hassles and costs.

Fintechs Facilitating Cross-border Trade

Seamless cross-border financial transactions will be key to economic recovery, whether easy remittance or the ability to reach a larger market and be able to trade beyond borders.

July saw the formalisation of the Digital Economy Partnership Agreement (DEPA) between New Zealand, Chile and Singapore, to facilitate end-to-end digital trade, which includes establishing digital identities, paperless trade and the development of Fintech solutions to support it. The initiative also intends to allow cross-border data flow and give access to necessary government data to small and medium enterprises (SMEs) enabling them to be digital-ready to explore newer markets.

Dubai International Financial Centre (DIFC) signed an MoU with Jiaozi Fintech Dreamworks based in China opening new opportunities for innovation and trade. The agreement will enable Fintech companies based in both cities to access each other’s markets. Primarily established to facilitate the ‘Belt and Road’ initiative, it is a critical component of the DIFC’s 2024 strategy to strengthen relationships with the international financial community and increase access to the South-South corridor. Over the last few years, DIFC has been associated with over 200 Fintech organisations, and last month invested in four Fintech startups through their accelerator program. The agreement with Jiaozi will look at collaboration opportunities in Blockchain, AI and Cloud and will facilitate cross-border workshops and training programs.

Continuing Interests in Emerging Economies

Fintechs have been a means to bring about financial inclusion and are increasingly being used to target the unbanked and underbanked. Emerging economies continue to be attractive for Fintech organisations and global financial institutions.

With much of Malaysia’s economy dependent on foreign workers, Instapay, regulated by the Bank Negara Malaysia (BNM), announced a collaboration with Mastercard, to provide e-wallet accounts to the migrant workers. The widespread use of e-wallets by the migrant worker community will bring benefits to both workers, as well as their employers. Interestingly, Fintech providers in emerging economies are also looking to expand into other emerging markets. Malaysia’s GHL Group received approval from Philippines Securities and Exchange Commission to operate a lending business through their new unit, GHL Philippines Financing Services. GHL has been diversifying its business and has been operating its lending business in Malaysia and Thailand since 2019.

Crown Agent Bank, a wholesale foreign exchange and cross-border payment services based in the UK, partnered with South Africa’s biometric-based payment company, Paycode. Together the companies are aiming to reach 100 million unbanked customers where Crown Agents Bank will use their FX and payment services to bolster Paycode’s product offering and support financial inclusion across Sub-Saharan Africa.

India and Indonesia in the Asia Pacific continue to be popular markets because of the huge proportion of the unbanked population. Rapyd, a UK based global B2B Fintech-as-as-service provider partnered with major Indian e-payment providers – including Paytm, PhonePe, PayU, Citibank, DBS Bank, HDFC Bank, BharatPay, and Unimoni to launch an all-in-one payments solution that spans credit and debit cards, UPI, wallets, and cash. New registrations for digital banking in Indonesia are on the rise and Fintech startup Akulaku is capitalising on the potential digital banking overhaul to offer affordable and comprehensive financial services to consumers.

Fintechs benefiting other industries

The Fintech revolution has shown the path to several other industries – Healthcare and Agriculture are some of the industries that are hoping to benefit from Fintech organisations and their innovations. The MoU between Alibaba Cloud, Pfizer and Singapore’s Fintech Academy announced earlier in July, promises to give early and necessary guidance to Healthtech start-ups, and shows the deep connection between Healthtech and Fintech. In the Philippines, in an effort to improve financial services for farmers, AgriNurture acquired Fintech firm Pay8. By leveraging Pay8 e-wallet services, farmers will be able to access online payment services. This will enable the largely unbanked farmer community to become an active part of the economy.

The technology that these industries are looking to benefit from is Blockchain. South Korea brought Blockchain to their healthcare industry for better data management and storage. The 3 major telecommunications providers in the country – KT, SK Telecom and mobile carrier LG U+ – have also collaborated with KB Insurance to launch the blockchain-based mobile notification service (MNS) by matching customer data to their mobile subscription information. Oxfam Ireland – a charity organisation based in Ireland, received a sum of USD 1.18 million from the European Commission for a Blockchain-based pilot. The company is working on a project -The UnBlocked Cash – to help disaster-affected communities receive cash-based entitlements with more efficiency and traceability.

Fintech will continue to be a cornerstone of economic and social recovery in the future, and the financial industry will see more collaborations between Fintech organisations, financial institutions and governments. Other industries will continue to take learnings from Fintech.

Singapore is committed to empower its small and medium enterprises (SMEs) to make better financial decisions and avail of seamless trade and financial transactions across the larger global economy. In June, the Digital Economic Partnership Agreement (DEPA) was signed between New Zealand, Singapore and Chile. The initiative includes facilitating end-to-end digital trade – by creating digital identities, allowing paperless trade and developing Fintech solutions – and ensuring a trusted cross-border data flow. To learn more about the DEPA agreement, register for the “Re-image the Digital Economy” webinar on the 29th July at 10am SGT.

This follows the announcement that was made last year by the Monetary Authority of Singapore (MAS) and Infocomm Media Development Authority (IMDA); of the successful completion of phase 1 of the proof-of-concept (POC) for its Business sans Borders (BSB). BSB is meant to be a “meta-hub” connecting several SME-centric platforms (starting within the Philippines, India and Singapore) giving SMEs seamless access to a larger ecosystem of buyers, sellers, logistics service providers, financing, and digital solution providers; and allowing them to be part of the larger global marketplace. The PoC involved a collaboration with private sector partners such as GlobalLinker, Mastercard, PwC, SAP and Yellow Pages.

AMTD Aligns with the BSB Objective

Hongkong-based investment banking firm AMTD Group leads a consortium that includes Xiaomi Finance, Singapore’s SP Group, and Funding Societies, that is a contender for one of Singapore’s digital wholesale banking licenses. While announcing their bid, they had clearly stated that they aimed to focus on SMEs in the region and globally. They continue to focus on SMEs by strengthening their partner ecosystem.

Last week AMTD announced a partnership with GlobalLinker making them the preferred financial services partner on the GlobalLinker’s SME-focused platform. AMTD intends to make available their entire ecosystem to SMEs including their virtual bank in Hong Kong, Airstar and their potential digital wholesale bank consortium in Singapore (which is to be called Singa Bank). In line with Singapore’s BSB objective, the partnership will see GlobalLinker join AMTD’s network which includes Fintech companies, regional banks and enterprises – SpiderNet. SpiderNet is a cross-sector ecosystem which is continuously expanding to connect and collaborate with shareholders, government bodies, industry associations, and clients. GlobalLinker’s AI-powered SME networking platform fosters SME digitalisation and helps members and customers connect with each other and use digital solutions. AMTD will be part of this network and bring the breadth of their partner ecosystem onto GlobalLinker’s platform.

Ecosystm Principal Advisor, Dheeraj Chowdhry says, “This marks the deepening of the trend of convergence between the established industry players and the Fintechs. The inefficiency of the obsession to ‘build’ and the associated resource and cost effort has perhaps been recognised on both sides and hence the path of coexistence and synergy seems more pragmatic. Fintechs are not competing but, in fact, complementing industry players by accelerating customer adoption of new digital formats for the entire landscape.”

AMTD Continues to Strengthen Partner Ecosystem

Last week also saw AMTD announce a collaboration with Singapore’s CIMB Bank and Funding Societies, to explore opportunities to create a wide range of banking and capital market services to aid SMEs with a one-stop solution for cross-regional and financial products.

Such partnerships by AMTD provides a glimpse of the group’s strong focus on Singapore. In April this year, AFIN and AMTD partnered to establish the USD 36 million AMTD ASEAN-Solidarity Fund. In May, AMTD, MAS, and Singapore FinTech Association (SFA) announced the launch of a USD 4.3 million MAS-SFA-AMTD FinTech Solidarity Grant to support Singapore-based FinTech firms.

AMTD remains committed to evolving their capabilities and ecosystem to empower the SME market in Singapore and the region. AMTD Digital announced their intention of acquiring a controlling stake in PolicyPal, Singapore’s InsureTech pioneer, and CapBridge Financial, a leading private capital platform for investing in growth companies globally. They have also expressed their intentions to acquire a controlling stake in FOMO Pay, a Singapore-based QR code and digital payment solution provider.

“AMTD’s early cognizance of the need for a strong ecosystem has led the organisation to their foray into partnerships and stakes in PolicyPal, FOMO Pay and now GlobalLinker. This strengthens AMTD’s commitment to the Fintech space including stakes in AirStar Digital Bank in Hong Kong and the Digital Bank application in Singapore,” says Chowdhry. “The Fintechs in AMTD’s stable will be part of the ‘AMTD web’ associated companies cutting across geographies and accelerate the ‘Business sans Borders’ objective of MAS and IMDA.”

In the blog, The Top 5 Fintech Trends for 2020, we had spoken about the impact of Fintech on financial inclusion. “Fintech will have a much greater impact than we realise, and we will continue to see it drive the induction of the unbanked into the mainstream economy. The growth in mobile phone penetration, however, continues to grow at a faster pace than banking accessibility across emerging economies. We will continue to see Fintech play a significant role in driving greater inclusion, especially to bring in the underserved in the emerging economies and reducing the gender gap when it comes to adoption of financial services – creating greater inclusion overall.”

Fintech Driving Financial Inclusion in Malaysia

Much of Malaysia’s economy is dependent on foreign workers with an estimate of 3-4 million migrants that roughly contribute to about 30% of the country’s labour force. Instapay, regulated by the Bank Negara Malaysia (BNM), caters to the underbanked community of foreign migrant workers, and recently announced a collaboration with Mastercard, to provide e-wallet accounts to Malaysian migrant workers. The app supports 9 languages and aims to have 100,000 users in the first year.

The widespread use of e-wallets by the migrant worker community is meant to bring benefits to both them, as well as their employers. It enables employers to use digital technologies for payroll management, reducing their dependence on cash handling, reducing costs and eliminating downtime as their employees no longer need to queue up on paydays.

The Instapay e-wallet also gives a largely underbanked segment of the society access to affordable financial products and services. The partnership with Mastercard gives Instapay’s customers access to the global network of merchants and ATMs, allowing easier access to financial services.

Ecosystm Principal Advisor, Dheeraj Chowdhry says, “Instapay’s foray into e-wallets furthers and supports the country’s objective of democratising banking and moving to a cashless economy. Collaboration with an international player like Mastercard helps a domestic Fintech to deliver a product that is country agnostic. The migrant worker can not only use the Instapay wallet within Malaysia but also in their home country.”

Malaysia’s Focus on Fintech

The Malaysia Government aims to create a cashless society, lower transaction costs and provide access to the underserved customers. There are two kinds of financial inclusion – for the lower income group as well as for the small and medium enterprises (SMEs) – and Malaysia is committed to both. Digital payments and e-wallets aimed at the lower income group receives an estimated 36% of Fintech funding. The stumbling block is that about a third of the country’s population does not have smartphones, so funds transfer using mobile phone messages is still relevant in the country. Development of the SME sector and eCommerce are twin focus areas for the Digital Economy vision. This provides a ready market for digital payments. Also, while the SME community will still have access to traditional funding, there is expected to be a greater push towards crowdfunding and peer-to-peer financing. It is expected that the share of Fintech funding for alternative funding will grow beyond the estimated 6% that it receives now.

According to a Mastercard Impact Study 2020, Malaysia has the highest e-wallet usage in Southeast Asia. As the country moves towards creating a cashless society, the Government is hoping e-wallet adoption increases. Several initiatives and schemes have been rolled out to promote e-wallets adoption. Last month, Malaysia announced the intention to spend an estimated USD 176 million in 2020 to encourage e-wallet adoption. Earlier this year, the Government announced the e-Tunai Rakyat program to boost the adoption of e-wallets, supported by Grab, Boost and Touch ‘n Go. Chowdhry says, “Instapay e-wallet is yet another manifestation of the amplified focus on e-wallets in Malaysia. BNM has set aside an estimated USD 108 million and has introduced a scheme to give USD $7.25 in credit for every adoption of any of the top 3 e-wallets. This scheme has accelerated e-wallets in the country that has set an adoption target of 15 million i.e. half of its population.”

“This push is backed by a structured approach of increasing the number of small merchants accepting card payments. With BNM’s focus, there are as many as half a million POS terminals out there for both credit cards and QR codes.”

“Malaysia’s regulators have to be applauded for having a well-coordinated, holistic and converging strategy on creating a cashless economy. The issuance, acceptance and regulatory policies have been completely synergised to deliver.”

In the report, Ecosystm Predicts: The Top Healthcare Trends for 2020, we had noted the similarities between the healthcare and the financial services industries and that Healthtech will take lessons from the Fintech industry.

In the report, Ecosystm Principal Analyst, Sash Mukherjee said, “Fintech plays a significant role in driving greater inclusion, especially to drive the induction of the unbanked into the mainstream economy, give the underbanked more options to leverage the broader financial services available, and reduce disparity in the adoption of financial services by bridging the gender gap and differences based on ethnicity and socio-economic status. It is not hard to imagine a similar fate for Healthtech. As the industry focuses on value-based outcomes, governments put in more regulations around accountability and transparency in the industry, and people expect the customer experience that they get out of their retail interactions, Healthtech start-ups will become as mainstream as Fintech start-ups.”

However, Mukherjee notes that there might be some pitfalls in this journey, especially when organisations focus more on the technology and less on the actual application and benefits of the technology. “Innovators and start-ups need to align themselves early, with corporates and technology providers to gain a better understanding of the market and regulatory landscape.”

Singapore bringing key industry stakeholders together

The MoU between Alibaba Cloud, Pfizer and Singapore’s Fintech Academy announced yesterday, is a move in the right direction that promises to give early and necessary guidance to Healthtech start-ups. Under the newly formed Healthcare Fintech Alliance (HFA), Alibaba will provide infrastructural support and technological mentorship to the Healthtech and Fintech start-ups to help them leverage cloud, AI and other technologies for their future requirements. The Fintech Academy will guide these start-ups through talent management and venture building programs. Pfizer will provide thought leadership through its network of healthcare experts and opinion leaders, including guidance on commercialisation of the products and services. The Healthcare Fintech Alliance initiative will begin with a pilot in Singapore, Indonesia, and Vietnam before expanding to other regions – Malaysia and the Philippines.

Mukherjee says, “The healthcare industry, for all the cutting-edge research, that it represents, has been remarkably slow to transform. But the COVID-19 crisis has forced the industry to transform, without the luxury or time to think about it. While the implications on the life sciences and provider organisations is clearer, there has simultaneously emerged a need for transformation in the healthcare payer industry. There will be greater demand from consumers for micro-financing to tide over sudden healthcare crises and greater transparency in how these funds are managed. Again, there is an immense potential here for the industry to learn from Fintech.”

Healthcare Fintech Alliance Focus Areas

The focus areas for Healthcare Fintech Alliance shows the deep connection between Healthtech and Fintech.

- Healthcare Affordability. Micro-financing and other financial models involving patients, family members, payers, and other healthcare stakeholders

- Value Based Healthcare. Linking payment schemes to a drug’s effectiveness, health outcomes or utilisation

- Outcome Monitoring. Tracking and reporting of outcomes derived from patients, wearables, healthcare providers, R&D databases and real-world evidence.

- Personalised Healthcare. Using digital technology to tailor healthcare to individual needs

- Innovative Healthtech Devices. Driving adoption in digital tools, such as diagnostic tools linked to medicine access and reimbursement

- Population Health Management. Leveraging patient and associated data in a compliant way to better understand population health characteristics, for effective wellness programs, treatment protocols and cost management.

“Alliances such as these have potential benefits for the industry stakeholders such as Alibaba and Pfizer. Alibaba has been focusing on the Southeast Asia market – earlier in the month the Alibaba Cloud Philippines Ecosystem Alliance was formed to support digital transformation in start-ups and small and medium enterprises. Initiatives such as this is an effective way to associate themselves with the evolving start-up community in the region,” says Mukherjee. “Life sciences companies operate in an extremely competitive global market where they have to work on new products against a backdrop of competition from generics and global concern over rising healthcare expenditure. Against that backdrop, this alliance is the right go-to-market messaging for Pfizer as well.”

“However, the deepest positive impact of alliances such as these will be on the Healthcare industry as a whole. It makes concepts such as value-based healthcare, remote care and personalised healthcare achievable in the near future.”

We are increasingly seeing digital becoming a priority as governments look at socio-economic recovery. It is not just imperative that countries push the adoption of digital technologies – the crisis has also presented an opportunity for them to do so. In March this year, when governments across the world had started announcing stimulus packages designed to keep the economy afloat, Ecosystm Principal Advisor Tim Sheedy had said in his blog, Government Should Focus Coronavirus Stimulus on Digital Initiatives, “Good stimulus packages will have a broad impact but also drive improved business and employment outcomes. Stimulus packages have an opportunity to drive change – and the COVID-19 virus has shown that some businesses are not well equipped for the digital era.”

The pandemic has fast demonstrated the power of being aligned to the digital economy. Ecosystm CEO Amit Gupta says, “Organisations that were digital-ready were able to manage their business continuity almost immediately in enabling a remote workforce. The transfer was almost seamless for such businesses as the teams had already imbibed the principles of remote collaboration and were already familiar with tools that enable collaboration and communication. For many of these organisations, it was almost a matter of employees packing up their work-issued laptop and heading home.”

“In addition, those that were fully digitalised were better prepared to continue not only interacting with their clients remotely but also in many cases were able to deliver their offerings to their customers through their website or mobile apps.”

Gupta also notes that Ecosystm research shows that before the COVID-19 outbreak only about 35% of SMEs considered themselves ready for the digital economy, compared to half of the large enterprises. “This needs to change – and change fast!”

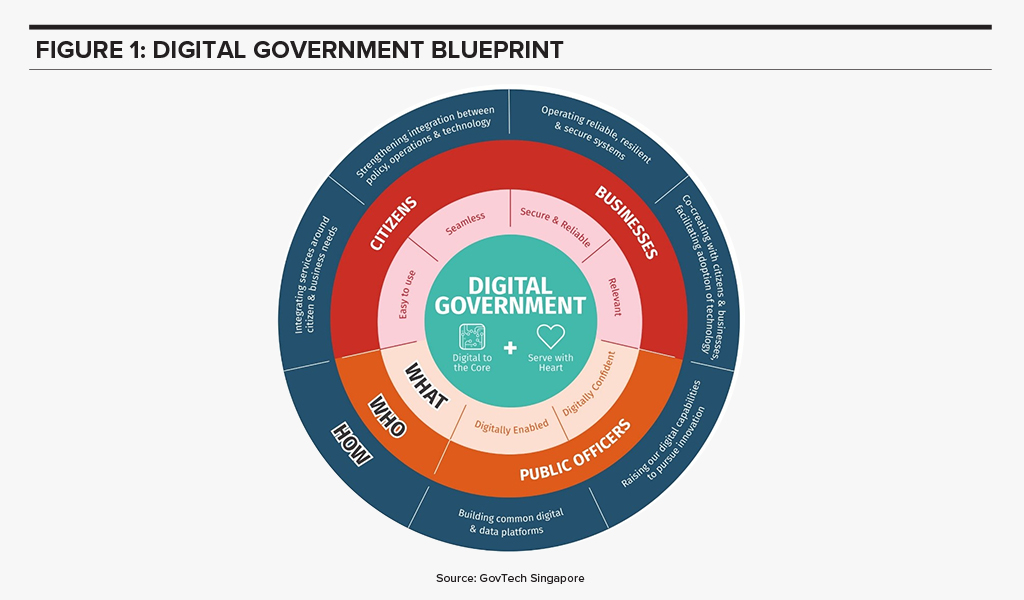

Singapore’s Digital Government Blueprint

In Singapore’s Digital Government Blueprint that supports its Smart Nation vision, digitalisation is positioned as a key pillar for public service transformation. The focus for business stakeholders in this journey includes co-creating and facilitating the adoption of technologies (Figure 1).

Small and medium enterprises (SMEs) often struggle with going digital because of lack of resources – both financial and skills – and vision. In a country such as Singapore, where SMEs are estimated to account for 99% of all enterprises and 77% of employment, it is imperative that the Digital Economy vision includes a special focus on them.

Gupta says, “Despite significant incentives, there has been resistance from SMEs to go digital as it still involves time and monetary investment from them. The need to retrain and upskill their teams is also a perceived roadblock to the uptake.”

Singapore Empowering SMEs to go Digital

As the Government looks to open the economy up in a phased manner, it sees this as the right opportunity to make SMEs digital-ready. It is “seizing the moment” and has established the SG Digital Office (SDO) in an effort to enable every individual, worker and business to go digital. Initiatives include the recruitment and deployment of 1,000 Digital Ambassadors by end June to provide personalised as well as small group support to seniors and owners of local eateries, who require additional assistance to adopt digital solutions and technology.

In 2018, the Monetary Authority of Singapore (MAS) and Infocomm Media Development Authority (IMDA) had launched SGQR to unify the fragmented e-payment landscape in the country, making it compatible with 27 payment schemes. The SDO aims to drive SMEs (especially in the F&B sector) to adopt SGQR codes for e-payments. The goal is to engage 18,000 stallholders of local eateries (hawker centres, wet markets, coffee shops and industrial canteens) to have the unified e-payment solution by June 2021. Further, multiple government agencies – IMDA, National Environment Agency (NEA), Jurong Town Corporation, Housing Development Board (HDB) and Enterprise Singapore – come together to offer a bonus of SGD 300 per month over five months to encourage more F&B SMEs to adopt e-payments.

“Financial Inclusion is one of the mainstays of a progressive economy. Given the significant investment that has gone into the e-payments infrastructure by government agencies led by MAS, we are placed well compared to other nations,” says Gupta. “However, there is work to be done in certain demographics and sectors. The drive to support F&B outlets and local eateries to get on the bandwagon will be an exceptional step and will be well received by consumers.”

“There are only a handful of governments that can compare with what the Singapore Government has put in place when it comes to initiatives to drive the uptake of technology by SMEs. This current crisis may well become the catalyst for SMEs to recognise the urgency of getting digital-ready and they should use this as an opportunity to leverage the government support around technology adoption and emerge as digital-savvy organisations.”

India has clearly been a target market for Facebook due to the size of the country’s untapped market and the proportion of its younger population. It is estimated that nearly 45% of the population is below 25 years – a prime target for social media and eCommerce platforms. Facebook’s Free Basic program, launched in 2016 to introduce the potential of the Internet to the underprivileged and digitally unskilled, failed primarily because it did not have knowledge of the telecommunications market in India. Facebook returned to the India market the following year, this time in collaboration with Airtel, to launch Express WiFi, aimed at setting up WiFi hotspots to provide internet in public places – again aimed at India’s connectivity issues.

Making its largest foray into the Indian market yet, last week Facebook announced that it is investing US$5.7 billion in Jio Platforms – India’s largest telecom operator – for a 9.9% minority stake. Facebook makes its intentions very clear and is targeting the 60 million small and medium enterprises (SMEs) who can be the backbone of India’s growing digital economy. This includes a rather unorganised retail sector, which has had to adopt digital at breakneck speed following the Government’s earlier financial reforms, which impacted the smaller retailers, dependent primarily on cash transactions. Facebook is by no means the only global giant with an interest in India’s retail business – with Amazon and Walmart leading the way.

The JioMart and WhatsApp Pilot

Just days after the announcement, JioMart – an eCommerce venture also a wholly-owned subsidiary of Reliance Industries, like Jio Platforms – has launched a pilot in Mumbai which allows users to order groceries through WhatsApp. Customers can now place grocery orders through WhatsApp Business with JioMart reaching out to small-scale retailers and brick and mortar stores – or “Kirana stores” as they are referred to in India – to fulfil the order. More than 1,200 local stores have been engaged for this pilot. It currently does not include a digital payment option and invoices and alerts are sent through WhatsApp. Mukesh Ambani, Chairman and MD of Reliance Industries, says that the JioMart and WhatsApp collaboration has the potential to make it possible for around 30 million neighbourhood stores to transact digitally.

India Emerging as the New Battlefield

India is an important eCommerce market for global giants such as Facebook and Amazon, who have struggled with establishing a presence in China. Walmart has also set it its sights on India, with its recent acquisition of Flipkart. Ecosystm Principal Advisor, Kaushik Ghatak says. “India represents the final frontier, where the battle lines are being drawn, and the three are heading towards a collision path. Facebook’s recent move has just upped the game for Amazon and Walmart, as well as for the eCommerce and Fintech start-ups who have been eyeing this market.”

Amazon has been the early mover, establishing its eCommerce presence in India way back in 2013. Ghatak says, “From its initial marketplace approach of curating suppliers to start selling on its platform, Amazon graduated to offering its own delivery and fulfilment services, by establishing dozens of warehouses across India. This was to ensure the quality and timeliness of deliveries, upholding its ‘Fulfilment by Amazon’ (FBA) brand promise. There was a considerable cost though, in terms of time to ramp up and investments – with the associated asset risks. Also, reaching out to the diffused retail sector, with their non-existent or very low level of digitalisation, has been difficult for all the major eCommerce players such as Amazon and Flipkart. Jeff Bezos’ announcement of an additional investment of $ 1 billion, earlier this year, to digitise SMEs, allowing them to sell and operate online, is a step to extend its reach into this diffused retail market.”

JioMart’s model, according to Ghatak is in stark contrast to Amazon’s. “JioMart’s currently ongoing pilot in Mumbai is a classic B2C marketplace model, with little or no asset risk. The orders placed by the customers are routed to the nearest Kirana store based on stock availability, with the customers going to pick up the ordered items themselves at times.”

Ecosystm Principal Advisor, Niloy Mukherjee says, “Jio has unparalleled market access in India with reports showing north of 370 million subscribers. Even at a $1.7 per month revenue from such a huge number, one can get to a $7.5 billion-dollar annual business. But even this is dwarfed by what that subscriber base itself is worth – through the data it provides, the products that can be sold and so on. Similarly, WhatsApp will prove to be more important than Facebook in India, with more than 400 million users. Using WhatsApp to get Kirana stores to do delivery can be a true game-changer.”

Talking about how this competes with Amazon, Mukherjee says, “This can eat into the business of an Amazon and my guess is, it will be far more efficient. The proximity to the customer will allow multiple deliveries per day at short notice, and fresh produce guarantees – maybe even door returns if not satisfied – that would be hard to match. Given the traffic situation in large Indian cities, delivery logistics from a more distant source will always struggle to compete. This is one tip of a multi-pronged spear – there are obviously other products that can be contemplated, leading to additional revenues.”

The Possibilities Ahead

Mukherjee explains why he thinks Facebook invested in Jio Platforms, rather than just forging a collaboration model. “Clearly both parties want to tie the other down and make sure that this alliance is long term. And this possibly means revenue will be shared instead of the usual commission model. Also, the go-to-market implications can run to more than just the Indian market. WeChat Pay is huge in China but not really elsewhere. If this works, there could be a potential “WhatsApp Pay” in the rest of the world. For Jio who already dominates the telecom landscape in India, this deal is a step towards taking their earnings to a new level, above the top end of the telecom category – they can access profit pools available to hardly any telecom provider worldwide.”

At a time when a market entry for foreign players in India is getting tougher with increasing regulatory pressures, a tie-up with the biggest player in India is indeed a very promising step – for both Facebook and Reliance. “For Facebook, this is a great opportunity to take its dependence away from a primarily ad-driven revenue model. The digitalisation of the diffused retail sector in India will open up new revenue opportunities from its WhatsApp Business App, WhatsApp Business API, and WhatsApp Pay-UPI gateway (pending regulatory approval). There is a potential of revenues from a variety of marketing services, membership fees, customer management services, product sales, commissions on transactions, and software service fees,” says Ghatak.

Talking about the potential for Reliance Industries, Ghatak says, “The technology horsepower of Facebook will help propel them ahead of Fintech and eCommerce companies in India – challenging already established players such as Amazon and Flipkart, and the newbie start-ups. Ability to drive transactions and digital payments in the diffused retail sector will open up huge revenue opportunities that were largely untapped until now, with low asset risks. Also, this sector has traditionally operated on a cash-based model and the recent COVID-19 crisis has exposed how vulnerable the sector is with a limited view of the supply chain, and limited funding for working capital. Developing relationships with the millions of Kirana stores spread across India also gives the opportunity of revenue generation through supply chain financing – a largely ignored sub-sector until now.”

Mukherjee thinks that this alliance will challenge players such as Amazon and Amazon Pay, Google Pay and PayTM. Ghatak also thinks that eventually, Jio Platform will have to either choose between or integrate the best features of WhatsApp Pay and the Jio Money Merchant payment gateways.

However, Ghatak offers a word of caution on the downside risks as well. “Partnering with Facebook is a hugely ambitious game plan for Reliance Industries. The success of its plans will also depend on how well it is able to curate the suppliers who are responsible for the actual delivery. In a consumer-driven business model, trust and customer experience cannot be compromised. The low asset, high leverage and high reach model can unravel itself if the customer gets the short end of the stick, in this rush for eCommerce domination.”

The ongoing global crisis is expected to drive more investments in Fintech, especially in the area of digital payments, as more organisations and consumers adopt eCommerce. Fintech will also continue to grow in areas such as Regtech and Blockchain for ease of reporting and enhanced transaction security.

Ecosystm Principal Advisor, Paul Gestro says, “In the environment, we find ourselves in now – and will be for some time – we have likely already switched to a number of new online channels, or at the very least increased the use of them. Fintech has played a big role already with online shopping & delivery, contactless payments and the general reduction in face to face transacting. Small and medium enterprises (SMEs) may gain the most as Fintech has enabled credit to be approved and distributed faster, either by banks or governments.”

“Fintech have been able to develop bespoke applications based on their open platforms to provide immediate channels to get much-needed capital flowing through the economy. Governments have often turned to the Fintechs first rather than traditional financial institutions. If Fintechs can still access investment capital to survive and keep growing, they will continue to disrupt the intermediaries across all sectors. It is yet to be seen if this will accelerate or be curtailed, but that will depend on how the financial institutions react to whatever the new normal will be.”

The Role of Blockchain in Financial Services

Talking about the role of Blockchain in Financial Services, Gestro says, “Overall Blockchain will lead to a more open and interconnected economy that is borderless, transparent and does not need counter-party trust to operate. To date, banks and other financial institutions have been the intermediary to make this happen but, in many areas, it can be slow and costly. Blockchain has the advantage of eliminating the intermediary or ‘middleman’.”

“One particular area is the use of ‘Smart Contracts’. Financial contracts involve legal work, document handling, sighting, signing and sending them to the right people. All of this involves both time and people and proves to be an expensive option eventually. Blockchain can speed this process up in a secure (with no failure points), interoperable and risk-free environment. Trade finance, lending and Islamic Banking are all potential areas that will benefit immensely.”

However, Gestro also extends a word of caution. “On paper, a cross-border Blockchain ecosystem makes perfect sense. However financial institutions have strict and long-standing governance and compliance boundaries that do not make it so easy to ‘switch’ to Blockchain overnight. The entire rationale of Blockchain is decentralising the legacy of competing rules and regulations and different agendas – this would mean that without a decision-maker, bottlenecks will form,” says Gestro. “On the other hand, financial institutions have also developed rapid transactional processing capability and Blockchain technology may be a long way from replicating that speed. So, even though Blockchain will prove immensely beneficial, scalability, risk management and compliance are the three areas that are inhibiting financial institutions from a full-blown adoption.”

Blockchain in Islamic Banking

One of the key benefits of Fintech is to drive financial inclusion. This is particularly true when it comes to widespread access to Islamic Banking facilities. With Fintech, Islamic Banking becomes more accessible to a larger population who do not bank because the banking and financial practices are not Shariah-compliant. Gestro sees a clear role of Blockchain in Islamic Banking. “The two key principles of Islamic Banking are the sharing of profit/loss and the prohibition of interest collection/payment. A key principle of Blockchain finance is smart contracts. With smart contracts, the entire contractual process can be automated quickly and transparently with the terms of each contract enforced as it should. A smart contract will be in compliance with the Shariah objective of ensuring transparency in a deal with clear asset definitions, payment terms and enforcement – all aligned with the principles of trust.”

UAE has been the hub of global Islamic financial services and there have been a few initiatives in 2019 to drive the adoption of Fintech in Banking and Financial Services. Etisalat Digital – the digital arm of Etisalat focused on transformational technologies – has developed the UAE Trade Connect (UTC), a nationwide platform that uses disruptive technologies to digitalise trade in the UAE. The initial phase will focus on addressing the risks of double financing and invoice fraud before turning to other key areas of trade finance. Created in partnership with First Abu Dhabi Bank (FAB) and Avanza Innovations, the platform has since seen the participation of 7 other major banks in the UAE. The goal of UTC is to drive transformation in trading practices by enabling banks, enterprises and governments to collaboratively evaluate technologies such as Blockchain, AI, machine learning and robotics.

Later in the year, during the Middle East Banking Forum in Abu Dhabi, the Central Bank of the UAE (CBUAE) announced the formation of a Fintech office to develop countrywide regulations for financial technology firms. The country has clearly been evaluating Fintech as a means of growth in the financial sector. Last week, the Abu Dhabi Islamic Bank (ADIB), in the UAE announced that they had successfully executed a Digital Ledger Technology (DLT) trade transaction with TradeAssets, a trade finance e-marketplace powered by Blockchain technology. It became the first Islamic Bank to transact on DLT.

As the global Islamic banking market heats up – with countries such as Malaysia openly vying to be a market leader – we will see higher adoption of Regtech and Blockchain in this sector.

Blockchain in China’s Financial Industry

Gestro says, “China is at the forefront of Blockchain technology development. Xi Jinping has announced that Blockchain is one of China’s technological priorities with the impending launch of the Blockchain Service Network (BCN). This is similar to the Belt and Road Initiative to provide infrastructure for the world to use, be a first mover and gain a strong foothold. It is no coincidence that China has filed the most Blockchain patents in the world. It has the collective power of the banking system, telecommunications behemoths and internet giants – all collaborating to realise China’s Blockchain vision.”

Last year, China unveiled plans to adopt and develop Blockchain to reduce banking fraud, offer secure loans, and streamline transactions in the financial industry. A Blockchain committee called the National Blockchain and Distributed Accounting Technology Standardisation Technical Committee was set up to explore the possibilities. The primary goal of the committee is to set standards for the adoption of Blockchain and involved big tech companies, such as Huawei, Tencent, Baidu, Ant Financial Services, and JD.com.

Ant Financial Services – Alibaba’s Fintech arm – recently created a new consortium Blockchain platform called Open Alliance Chain aimed at SMEs and developers. The available Blockchain tools would be able to help supply chain, invoices, donations, financial transactions and promote various other Blockchain uses across financial services.

There appears to be an interest in global financial services around Blockchain. It will be interesting to watch this space to see if Blockchain adoption in the Financial Services industry becomes mainstream, as the global economy adjusts to the new normal.

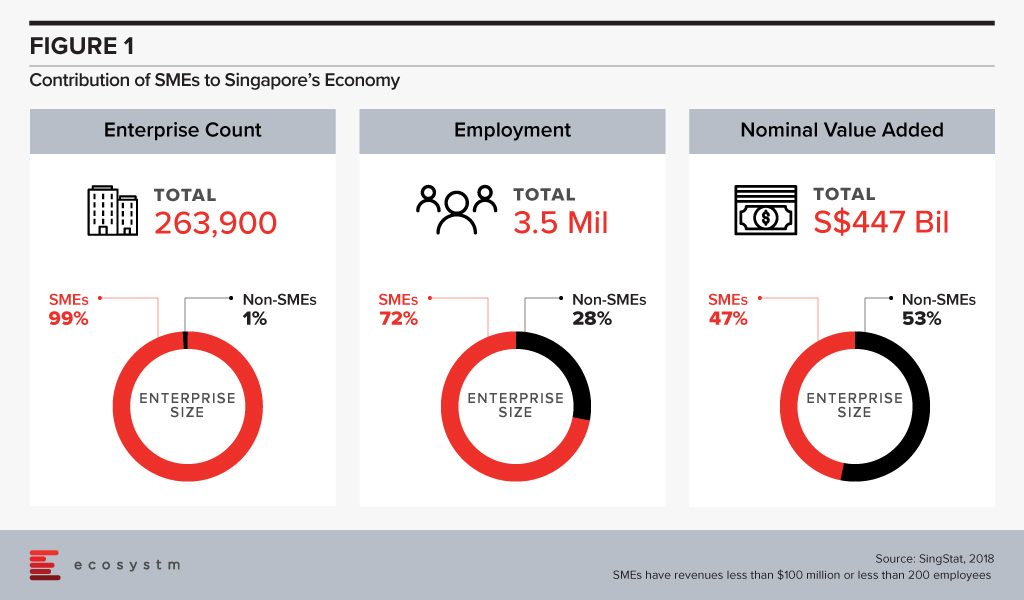

Singapore maintains its competitiveness through strong Government support and an environment that encourages trade and investments. The economy sees a huge contribution from start-ups and small and medium enterprises (SMEs), which receives financial incentives and technology guidance from the Government.

The success of SMEs in Singapore is at the core of national economic growth with approximately 261,000 SMEs contributing to nearly 50% of the country’s GDP.

A survey conducted by United Overseas Bank (UOB) in November 2019 illustrates that SMEs in Singapore are focusing on boosting productivity as they grapple with macro-economic and socio-political uncertainties this year. The UOB survey included 615 local SMEs with a revenue of less than S$100 million. Nearly half of the SMEs surveyed have a positive outlook for their business in 2020, while nearly a third are not so optimistic about it.

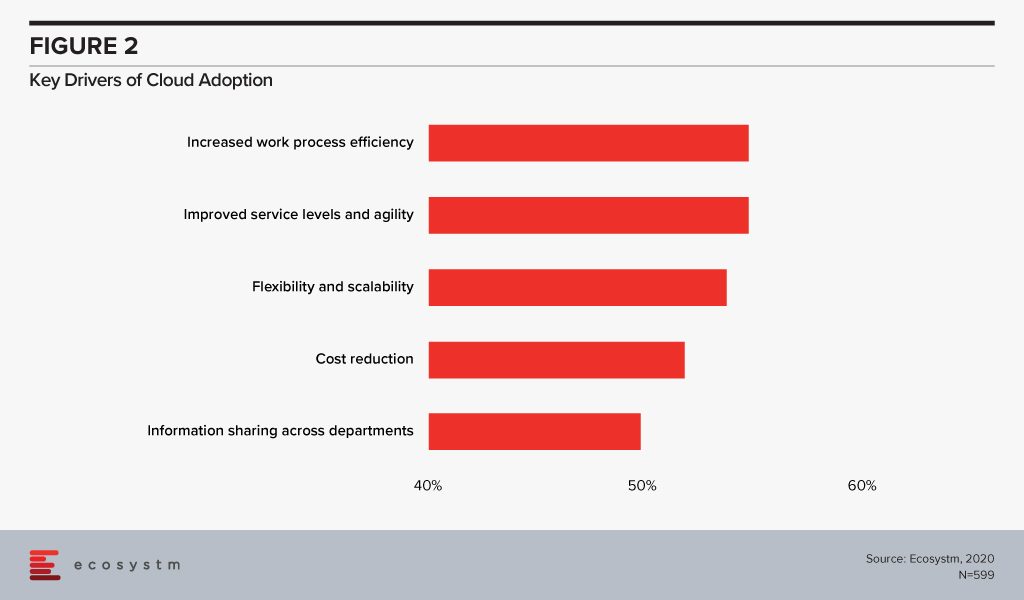

While cost reduction and new streams of revenue generation are top business priorities, more than half of the SMEs polled, mentioned increasing productivity as their top priority. Technology adoption has often been linked to an increase in productivity. SMEs in Singapore appear to be on the right track as currently 65% use digital solutions, mostly geared towards accounting, HR and customer relationship management. Digitalisation involves a widespread adoption of cloud and automation solutions. If we look at the key drivers of cloud adoption across all global organisations (Figure 2), we find that optimisation and productivity are key incentives.

Interestingly, the UOB survey also finds that more than half of SMEs in Singapore have sustainability goals. Resource optimisation and energy efficiency will also see higher adoption of technology in the future.

Government Initiatives Empowering SMEs

Government agencies and industry bodies have always been proactive in empowering SMEs with technological knowledge. There are various programs and initiatives to promote digitalisation, which have made Singapore SMEs competitive at a global level.

The Infocomm Media Development Authority (IMDA) is helping Singapore SMEs to scale and improve their digital capabilities, expand their network and go global through collaboration with multinational companies (MNCs). The SMEs Go Digital program launched in 2017, has seen an estimated 4,000 SMEs adopting pre-approved digital solutions.

Several organisations in Singapore – such as A*Star and Enterprise Singapore – have targeted programs for the SME community. One of the key challenges for SMEs that impacts their ability to invest in technology is a lack of internal IT skills. Initiatives such as the Technology Adoption Programme (TAP) recognise this and bring in multiple industry and technology stakeholders to translate new technologies into Ready-to-Go (RTG) solutions, aimed at SMEs.

Apart from technology, access to financing is a key factor that determines the success of an SME and remains a key focus of Singapore’s banking and financial sector. The digital wholesale licenses are also aimed at SME financing, especially targeting those that are unable to procure funds from traditional sources.

Technologies Enabling Digitalisation in Singapore SMEs

Cloud

As mentioned earlier, cloud is the key enabler of digitalisation, giving organisations the ability to access solutions anywhere and anytime. Ecosystm research shows that 80% of SMEs in Singapore use an IaaS solution, while more than 75% use a SaaS solution.

There are programs that boost cloud adoption in Singapore SMEs as well. As an example, SMECEN, developed by the Association of Small & Medium Enterprises (ASME), and supported by Enterprise Singapore, Accounting and Corporate Regulatory Authority (ACRA) and Inland Revenue Authority of Singapore (IRAS) is a SaaS solution with accounting, HR and compliance modules – integration with other business tools is on the cards.

AI/Automation

Digitalisation will eventually involve investments in Automation and AI. For Singapore, AI is a key technology as it continues to focus on IoT, smart buildings, smart electricity, autonomous electric vehicles and other smart city solutions. The Government is working to open up access to data and AI tools so everyone can experiment. It especially wants to encourage SMEs to adopt AI and work on government use cases.

Singapore SMEs are ramping up their AI investments, especially in IoT sensor analytics (27%), machine learning (21%) and robotic process automation (16%), according to the Ecosystm AI study. Their key short-term drivers are insights into the competition and enhanced internal process monitoring. However, in the longer term, they are looking at cost reduction and better profit margins.

Fintech

According to an OCBC survey in 2018, which polled 200 such companies, two-thirds of SMEs in Singapore are likely to go cashless by 2023. It is estimated that over 75% of Fintech transactions in Singapore are digital payments and it receives over a quarter of Fintech funding. Government initiatives such as FAST and SGQR, have opened up digital payment options for consumer use as well as for SMEs.

However, the UOB survey notes some concerns that SMEs have over digital payments adoption, including customer/supplier acceptance and security. This is an encouraging sign, which indicates that SMEs are not just adopting technology because of the hype – but are evaluating the pros and cons of tech adoption before embarking on a digitalisation project.

The race for digital bank licenses in Singapore is on as the Monetary Authority of Singapore (MAS) deadline for applications closed at the end of last year.

The Singapore Government continues to promote fintech initiatives in the banking industry such as the FAST network (giving fintech and non-banking organisations access to the real-time payments network) and Project Ubin (focusing on inter-bank funds transfer using Blockchain). The digital bank licenses continue in the same vein and will offer the same banking services as traditional banks but operate online and without any physical infrastructure.

“The biggest gamechanger of the app-based and shared economy is that it puts the power of decision making and choice in the hands of the consumer. It also removes entry barriers for non-traditional market entrants, but the flipside is it also weakens a number of regulatory barriers that were put in place for safeguarding the consumer,” says Amit Gupta, Ecosystm CEO. “With digital banking at the verge of becoming mainstream, it will help spur the app-based economy with the advent of more complete ecosystems and the added benefit of stronger governance measures and frameworks that will come into play simply because financial regulators in Singapore are driving it.”

Digital banking is not new, and MAS has been encouraging banks to offer digital services since 2000. Taking it a step forward, in June 2019, MAS announced their intentions to issue 5 digital bank licences in Singapore, opening up the banking industry to the non-banking sector.

Following the announcement, in August 2019, MAS invited applications for 2 digital full banks (DFBs) aimed primarily at retail banking, and 3 digital wholesale banks (DWBs) primarily for SMEs and other non-retail segments. While DFB licenses are restricted to Singapore based companies (including foreign joint ventures with a Singapore entity and headquarters), DWB licenses have no such restrictions, opening the market to overseas players.

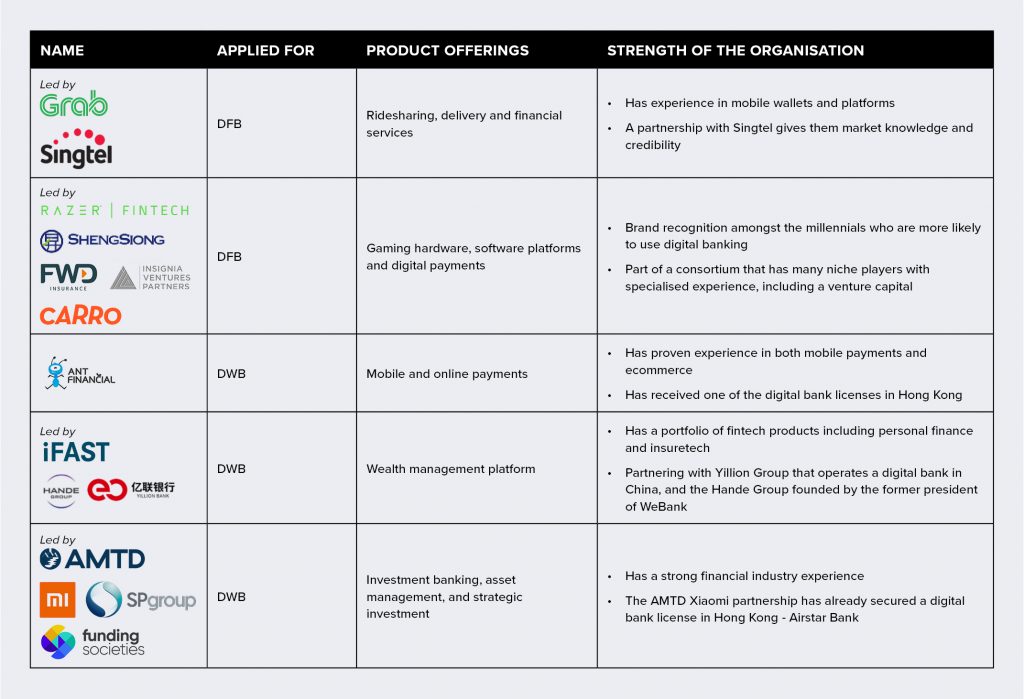

Applicants for the New Digital Bank License

MAS announced on January 7, 2020, that it had received 21 applications (7 for DFB and 14 for DWB licenses). A list of applicants has not been made available, and confirmation of application has typically come from the applicants themselves. The licences will be issued in mid-2020 with the commencement of business expected about a year later.

The race for the digital bank license in Singapore has seen several non-banking contenders. MAS has mentioned that applicants will be selected based on their market reputation, a proven track record, financial strength, innovative business models, and a commitment to develop the skills of the Singaporean workforce. The contenders who have announced their applications cover a wide range – from the Sea Group (whose eCommerce site, Shoppee has a strong presence in Singapore) to the Enigma Group (a financial organisation based in the UK). Here are some organisations that may well be ahead of the race:

“From the nature of consortium of bidders for DFBs and DFWs in Singapore, we can safely anticipate that the financial ecosystems will be aligned very closely with certain consumer demographics that make up the core target segments. As an example, Razer will be in a position to meet the specific needs of the millennial consumer base,” adds Gupta. “In saying that, it will also be important to evaluate how digital banks deal with educating consumers on wealth creation offerings and financial literacy, which is currently being achieved through personal touchpoints by the traditional banks.”

Ecosystm Comments

Singapore has emerged as one of the global leaders in fintech due largely to the maturity of the technology infrastructure, the banking sector and data compliance laws, as well as the tech-savviness of its citizens. The buzz created in the market when MAS announced the initiative last year is partly because a successful implementation in Singapore carries weight globally, especially in the relatively untapped Southeast Asian market.

Singapore also collaborates with the countries in the region empowering them with talent development and co-creation of fintech solutions. Initiatives such as the ASEAN Financial Innovation Network (AFIN) further promote fintech adoption through its open-architecture platform. Several countries in the region will take inspiration from Singapore and evaluate digital banks as a means to better financial inclusion. Thailand’s central bank has already indicated its interest in digital banks, prompted by the Singapore and Hong Kong initiatives.

Talking specifically about the competition in the Singapore financial industry, Gupta says, “Unlike some of the other markets, traditional banks in Singapore will continue to offer competing digital offerings as local banks such as DBS have been very savvy in building their digital offerings over the years. If their digital innovation keeps evolving at the pace they have been setting in recent years, they will present very stiff competitive barriers to the new digital bank entrants, especially given their ability to continue offering personalised service and touchpoints, coupled with compelling digital offerings.”