Banks, insurers, and other financial services organisations in Asia Pacific have plenty of tech challenges and opportunities including cybersecurity and data privacy management; adapting to tech and customer demands, AI and ML integration; use of big data for personalisation; and regulatory compliance across business functions and transformation journeys.

Modernisation Projects are Back on the Table

An emerging tech challenge lies in modernising, replacing, or retiring legacy platforms and systems. Many banks still rely on outdated core systems, hindering agility, innovation, and personalised customer experiences. Migrating to modern, cloud-based systems presents challenges due to complexity, cost, and potential disruptions. Insurers are evaluating key platforms amid evolving customer needs and business models; ERP and HCM systems are up for renewal; data warehouses are transforming for the AI era; even CRM and other CX platforms are being modernised as older customer data stores and models become obsolete.

For the past five years, many financial services organisations in the region have sidelined large legacy modernisation projects, opting instead to make incremental transformations around their core systems. However, it is becoming critical for them to take action to secure their long-term survival and success.

Benefits of legacy modernisation include:

- Improved operational efficiency and agility

- Enhanced customer experience and satisfaction

- Increased innovation and competitive advantage

- Reduced security risks and compliance costs

- Preparation for future technologies

However, legacy modernisation and migration initiatives carry significant risks. For instance, TSB faced a USD 62M fine due to a failed mainframe migration, resulting in severe disruptions to branch operations and core banking functions like telephone, online, and mobile banking. The migration failure led to 225,492 complaints between 2018 and 2019, affecting all 550 branches and required TSB to pay more than USD 25M to customers through a redress program.

Modernisation Options

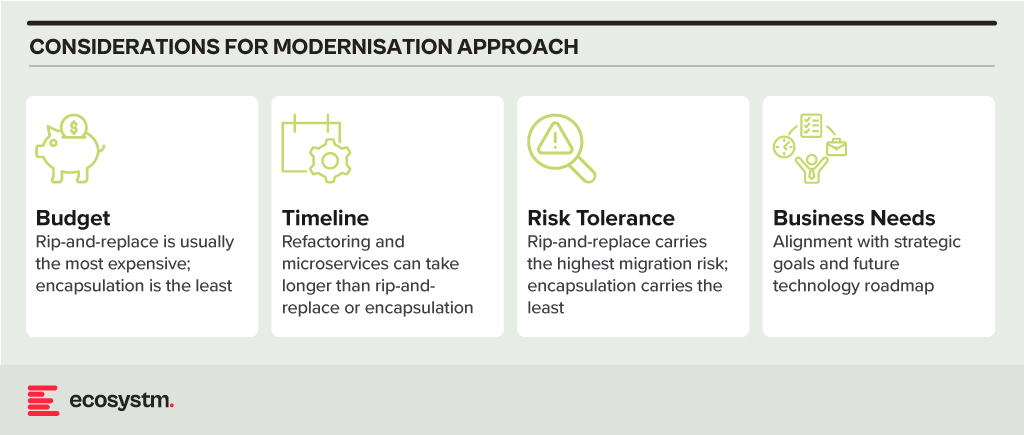

- Rip and Replace. Replacing the entire legacy system with a modern, cloud-based solution. While offering a clean slate and faster time to value, it’s expensive, disruptive, and carries migration risks.

- Refactoring. Rewriting key components of the legacy system with modern languages and architectures. It’s less disruptive than rip-and-replace but requires skilled developers and can still be time-consuming.

- Encapsulation. Wrapping the legacy system with a modern API layer, allowing integration with newer applications and tools. It’s quicker and cheaper than other options but doesn’t fully address underlying limitations.

- Microservices-based Modernisation. Breaking down the legacy system into smaller, independent services that can be individually modernised over time. It offers flexibility and agility but requires careful planning and execution.

Financial Systems on the Block for Legacy Modernisation

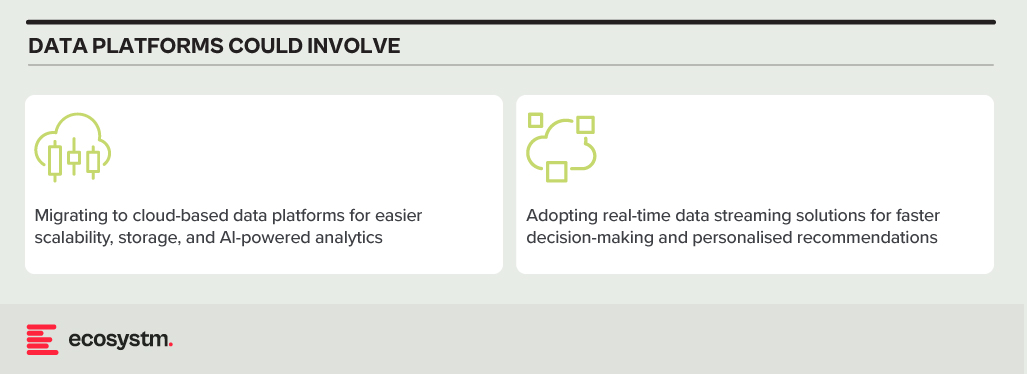

Data Analytics Platforms. Harnessing customer data for insights and targeted offerings is vital. Legacy data warehouses often struggle with real-time data processing and advanced analytics.

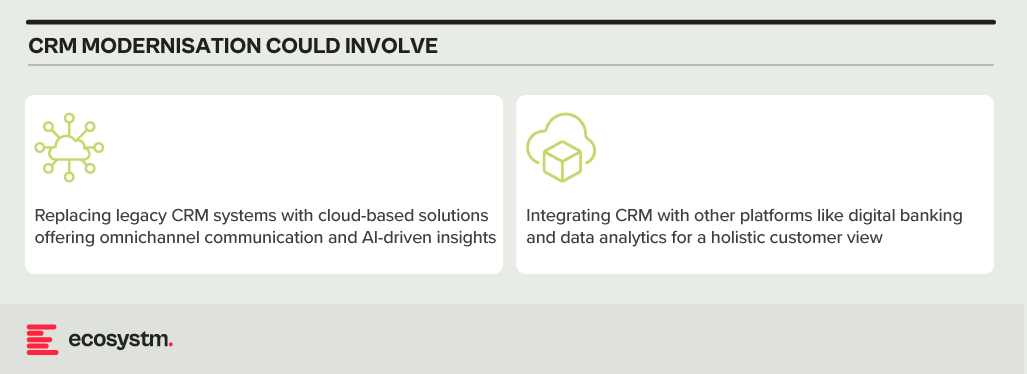

CRM Systems. Effective customer interactions require integrated CRM platforms. Outdated systems might hinder communication, personalisation, and cross-selling opportunities.

Payment Processing Systems. Legacy systems might lack support for real-time secure transactions, mobile payments, and cross-border transactions.

Core Banking Systems (CBS). The central nervous system of any bank, handling account management, transactions, and loan processing. Many Asia Pacific banks rely on aging, monolithic CBS with limited digital capabilities.

Digital Banking Platforms. While several Asia Pacific banks provide basic online banking, genuine digital transformation requires mobile-first apps with features such as instant payments, personalised financial management tools, and seamless third-party service integration.

Modernising Technical Approaches and Architectures

Numerous technical factors need to be addressed during modernisation, with decisions needing to be made upfront. Questions around data migration, testing and QA, change management, data security and development methodology (agile, waterfall or hybrid) need consideration.

Best practices in legacy migration have taught some lessons.

Adopt a data fabric platform. Many organisations find that centralising all data into a single warehouse or platform rarely justifies the time and effort invested. Businesses continually generate new data, adding sources, and updating systems. Managing data where it resides might seem complex initially. However, in the mid to longer term, this approach offers clearer benefits as it reduces the likelihood of data discrepancies, obsolescence, and governance challenges.

Focus modernisation on the customer metrics and journeys that matter. Legacy modernisation need not be an all-or-nothing initiative. While systems like mainframes may require complete replacement, even some mainframe-based software can be partially modernised to enable services for external applications and processes. Assess the potential of modernising components of existing systems rather than opting for a complete overhaul of legacy applications.

Embrace the cloud and SaaS. With the growing network of hyperscaler cloud locations and data centres, there’s likely to be a solution that enables organisations to operate in the cloud while meeting data residency requirements. Even if not available now, it could align with the timeline of a multi-year legacy modernisation project. Whenever feasible, prioritise SaaS over cloud-hosted applications to streamline management, reduce overhead, and mitigate risk.

Build for customisation for local and regional needs. Many legacy applications are highly customised, leading to inflexibility, high management costs, and complexity in integration. Today, software providers advocate minimising configuration and customisation, opting for “out-of-the-box” solutions with room for localisation. The operations in different countries may require reconfiguration due to varying regulations and competitive pressures. Architecting applications to isolate these configurations simplifies system management, facilitating continuous improvement as new services are introduced by platform providers or ISV partners.

Explore the opportunity for emerging technologies. Emerging technologies, notably AI, can significantly enhance the speed and value of new systems. In the near future, AI will automate much of the work in data migration and systems integration, reducing the need for human involvement. When humans are required, low-code or no-code tools can expedite development. Private 5G services may eliminate the need for new network builds in branches or offices. AIOps and Observability can improve system uptime at lower costs. Considering these capabilities in platform decisions and understanding the ecosystem of partners and providers can accelerate modernisation journeys and deliver value faster.

Don’t Let Analysis Paralysis Slow Down Your Journey!

Yes, there are a lot of decisions that need to be made; and yes, there is much at stake if things go wrong! However, there’s a greater risk in not taking action. Maintaining a laser-focus on the customer and business outcomes that need to be achieved will help align many decisions. Keeping the customer experience as the guiding light ensures organisations are always moving in the right direction.

For many organisations migrating to cloud, the opportunity to run workloads from energy-efficient cloud data centres is a significant advantage. However, carbon emissions can vary from one country to another and if left unmonitored, will gradually increase over time as cloud use grows. This issue will become increasingly important as we move into the era of compute-intensive AI and the burden of cloud on natural resources will shift further into the spotlight.

The International Energy Agency (IEA) estimates that data centres are responsible for up to 1.5% of global electricity use and 1% of GHG emissions. Cloud providers have recognised this and are committed to change. Between 2025 and 2030, all hyperscalers – AWS, Azure, Google, and Oracle included – expect to power their global cloud operations entirely with renewable sources.

Chasing the Sun

Cloud providers are shifting their sights from simply matching electricity use with renewable power purchase agreements (PPA) to the more ambitious goal of operating 24/7 on carbon-free sources. A defining characteristic of renewables though is intermittency, with production levels fluctuating based on the availability of sunlight and wind. Leading cloud providers are using AI to dynamically distribute compute workloads throughout the day to regions with lower carbon intensity. Workloads that are processed with solar power during daylight can be shifted to nearby regions with abundant wind energy at night.

Addressing Water Scarcity

Many of the largest cloud data centres are situated in sunny locations to take advantage of solar power and proximity to population centres. Unfortunately, this often means that they are also in areas where water is scarce. While liquid-cooled facilities are energy efficient, local communities are concerned on the strain on water sources. Data centre operators are now committing to reduce consumption and restore water supplies. Simple measures, such as expanding humidity (below 20% RH) and temperature tolerances (above 30°C) in server rooms have helped companies like Meta to cut wastage. Similarly, Google has increased their reliance on non-potable sources, such as grey water and sea water.

From Waste to Worth

Data centre operators have identified innovative ways to reuse the excess heat generated by their computing equipment. Some have used it to heat adjacent swimming pools while others have warmed rooms that house vertical farms. Although these initiatives currently have little impact on the environmental impact of cloud, they suggest a future where waste is significantly reduced.

Greening the Grid

The giant facilities that cloud providers use to house their computing infrastructure are also set to change. Building materials and construction account for an astonishing 11% of global carbon emissions. The use of recycled materials in concrete and investing in greener methods of manufacturing steel are approaches the construction industry are attempting to lessen their impact. Smaller data centres have been 3D printed to accelerate construction and use recyclable printing concrete. While this approach may not be suitable for hyperscale facilities, it holds potential for smaller edge locations.

Rethinking Hardware Management

Cloud providers rely on their scale to provide fast, resilient, and cost-effective computing. In many cases, simply replacing malfunctioning or obsolete equipment would achieve these goals better than performing maintenance. However, the relentless growth of e-waste is putting pressure on cloud providers to participate in the circular economy. Microsoft, for example, has launched three Circular Centres to repurpose cloud equipment. During the pilot of their Amsterdam centre, it achieved 83% reuse and 17% recycling of critical parts. The lifecycle of equipment in the cloud is largely hidden but environmentally conscious users will start demanding greater transparency.

Recommendations

Organisations should be aware of their cloud-derived scope 3 emissions and consider broader environmental issues around water use and recycling. Here are the steps that can be taken immediately:

- Monitor GreenOps. Cloud providers are adding GreenOps tools, such as the AWS Customer Carbon Footprint Tool, to help organisations measure the environmental impact of their cloud operations. Understanding the relationship between cloud use and emissions is the first step towards sustainable cloud operations.

- Adopt Cloud FinOps for Quick ROI. Eliminating wasted cloud resources not only cuts costs but also reduces electricity-related emissions. Tools such as CloudVerse provide visibility into cloud spend, identifies unused instances, and helps to optimise cloud operations.

- Take a Holistic View. Cloud providers are being forced to improve transparency and reduce their environmental impact by their biggest customers. Getting educated on the actions that cloud partners are taking to minimise emissions, water use, and waste to landfill is crucial. In most cases, dedicated cloud providers should reduce waste rather than offset it.

- Enable Remote Workforce. Cloud-enabled security and networking solutions, such as SASE, allow employees to work securely from remote locations and reduce their transportation emissions. With a SASE deployed in the cloud, routine management tasks can be performed by IT remotely rather than at the branch, further reducing transportation emissions.

At the end of last year, I had the privilege of attending a session organised by Red Hat where they shared their Asia Pacific roadmap with the tech analyst community. The company’s approach of providing a hybrid cloud application platform centred around OpenShift has worked well with clients who favour a hybrid cloud approach. Going forward, Red Hat is looking to build and expand their business around three product innovation focus areas. At the core is their platform engineering, flanked by focus areas on AI/ML and the Edge.

The Opportunities

Besides the product innovation focus, Red Hat is also looking into several emerging areas, where they’ve seen initial client success in 2023. While use cases such as operational resilience or edge lifecycle management are long-existing trends, carbon-aware workload scheduling may just have appeared over the horizon. But two others stood out for me with a potentially huge demand in 2024.

GPU-as-a-Service. GPUaaS addresses a massive demand driven by the meteoric rise of Generative AI over the past 12 months. Any innovation that would allow customers a more flexible use of scarce and expensive resources such as GPUs can create an immediate opportunity and Red Hat might have a first mover and established base advantage. Particularly GPUaaS is an opportunity in fast growing markets, where cost and availability are strong inhibitors.

Digital Sovereignty. Digital sovereignty has been a strong driver in some markets – for example in Indonesia, which has led to most cloud hyperscalers opening their data centres onshore over the past years. Yet not the least due to the geography of Indonesia, hybrid cloud remains an important consideration, where digital sovereignty needs to be managed across a diverse infrastructure. Other fast-growing markets have similar challenges and a strong drive for digital sovereignty. Crucially, Red Hat may well have an advantage where onshore hyperscalers are not yet available (for example in Malaysia).

Strategic Focus Areas for Red Hat

Red Hat’s product innovation strategy is robust at its core, particularly in platform engineering, but needs more clarity at the periphery. They have already been addressing Edge use cases as an extension of their core platform, especially in the Automotive sector, establishing a solid foundation in this area. Their focus on AI/ML may be a bit more aspirational, as they are looking to not only AI-enable their core platform but also expand it into a platform to run AI workloads. AI may drive interest in hybrid cloud, but it will be in very specific use cases.

For Red Hat to be successful in the AI space, it must steer away from competing straight out with the cloud-native AI platforms. They must identify the use cases where AI on hybrid cloud has a true advantage. Such use cases will mainly exist in industries with a strong Edge component, potentially also with a still heavy reliance on on-site data centres. Manufacturing is the prime example.

Red Hat’s success in AI/ML use cases is tightly connected to their (continuing) success in Edge use cases, all build on the solid platform engineering foundation.

Organisations in Asia Pacific are no longer only focused on employing a cloud-first strategy – they want to host the infrastructure and workloads where it makes the most sense; and expect a seamless integration across multiple cloud environments.

While cloud can provide the agile infrastructure that underpins application modernisation, innovative leaders recognise that it is only the first step on the path towards developing AI-powered organisations. The true value of cloud is in the data layer, unifying data around the network, making it securely available wherever it is needed, and infusing AI throughout the organisation.

Cloud provides a dynamic and powerful platform on which organisations can build AI. Pre-trained foundational models, pay-as-you-go graphics superclusters, and automated ML tools for citizen data scientists are now all accessible from the cloud even to start-ups.

Organisations should assess the data and AI capabilities of their cloud providers rather than just considering it an infrastructure replacement. Cloud providers should use native services or integrations to manage the data lifecycle from labelling to model development, and deployment.

In this Ecosystm Byte, sponsored by Oracle, Ecosystm Principal Advisor, Darian Bird presents the top 5 trends for Cloud in 2023 and beyond. Read on to find out more.

Download ‘The Top 5 Cloud Trends for 2023 & Beyond’ as a PDF

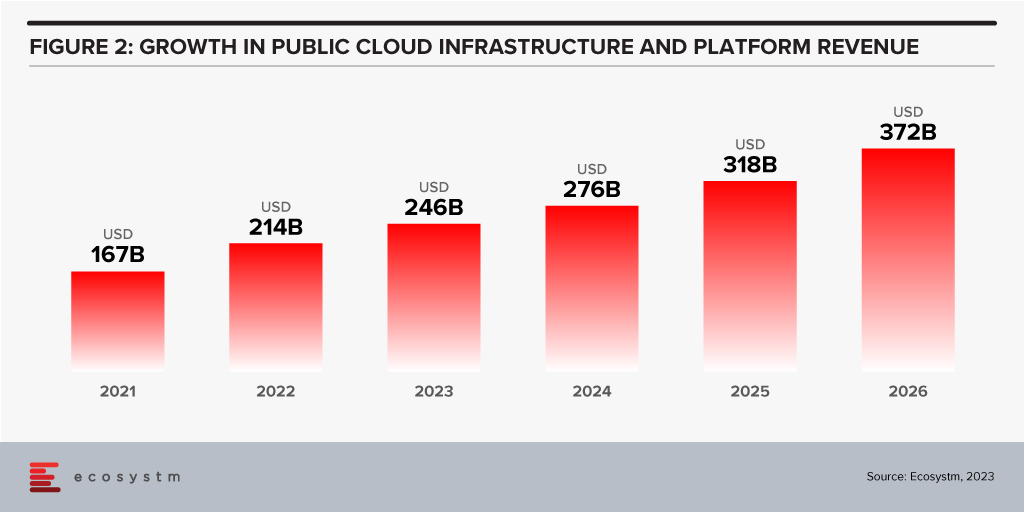

All growth must end eventually. But it is a brave person who will predict the end of growth for the public cloud hyperscalers. The hyperscaler cloud revenues have been growing at between 25-60% the past few years (off very different bases – and often including and counting different revenue streams). Even the current softening of economic spend we are seeing across many economies is only causing a slight slowdown.

Looking forward, we expect growth in public cloud infrastructure and platform spend to continue to decline in 2024, but to accelerate in 2025 and 2026 as businesses take advantage of new cloud services and capabilities. However, the sheer size of the market means that we will see slower growth going forward – but we forecast 2026 to see the highest revenue growth of any year since public cloud services were founded.

The factors driving this growth include:

- Acceleration of digital intensity. As countries come out of their economic slowdowns and economic activity increases, so too will digital activity. And greater volumes of digital activity will require an increase in the capacity of cloud environments on which the applications and processes are hosted.

- Increased use of AI services. Businesses and AI service providers will need access to GPUs – and eventually, specialised AI chipsets – which will see cloud bills increase significantly. The extra data storage to drive the algorithms – and the increase in CPU required to deliver customised or personalised experiences that these algorithms will direct will also drive increased cloud usage.

- Further movement of applications from on-premises to cloud. Many organisations – particularly those in the Asia Pacific region – still have the majority of their applications and tech systems sitting in data centre environments. Over the next few years, more of these applications will move to hyperscalers.

- Edge applications moving to the cloud. As the public cloud giants improve their edge computing capabilities – in partnership with hardware providers, telcos, and a broader expansion of their own networks – there will be greater opportunity to move edge applications to public cloud environments.

- Increasing number of ISVs hosting on these platforms. The move from on-premise to cloud will drive some growth in hyperscaler revenues and activities – but the ISVs born in the cloud will also drive significant growth. SaaS and PaaS are typically seeing growth above the rates of IaaS – but are also drivers of the growth of cloud infrastructure services.

- Improving cloud marketplaces. Continuing on the topic of ISV partners, as the cloud hyperscalers make it easier and faster to find, buy, and integrate new services from their cloud marketplace, the adoption of cloud infrastructure services will continue to grow.

- New cloud services. No one has a crystal ball, and few people know what is being developed by Microsoft, AWS, Google, and the other cloud providers. New services will exist in the next few years that aren’t even being considered today. Perhaps Quantum Computing will start to see real business adoption? But these new services will help to drive growth – even if “legacy” cloud service adoption slows down or services are retired.

Hybrid Cloud Will Play an Important Role for Many Businesses

Growth in hyperscalers doesn’t mean that the hybrid cloud will disappear. Many organisations will hit a natural “ceiling” for their public cloud services. Regulations, proximity, cost, volumes of data, and “gravity” will see some applications remain in data centres. However, businesses will want to manage, secure, transform, and modernise these applications at the same rate and use the same tools as their public cloud environments. Therefore, hybrid and private cloud will remain important elements of the overall cloud market. Their success will be the ability to integrate with and support public cloud environments.

The future of cloud is big – but like all infrastructure and platforms, they are not a goal in themselves. It is what cloud is and will further enable businesses and customers which is exciting. As the rates of digitisation and digital intensity increase, the opportunities for the cloud infrastructure and platform providers will blossom. Sometimes they will be the driver of the growth, and other times they will just be supporting actors. But either way, in 2026 – 20 years after the birth of AWS – the growth in cloud services will be bigger than ever.

2020 was a watershed year for the industry as they proved to be the backbone for the rapid changes in work practices, communication and entertainment. This has led telecom providers to embark on their won digital transformation journeys.

The challenges continue for the industry, especially as 5G has not yet delivered on the early promises. Telecom operators today are having to provide cutting-edge services and top-notch customer experience as they continue to be challenged by new market entrants and strong regulatory pressures.

In 2022, telecom providers will be driven by the need to innovate and improve their product and service lines; improve customer experience; comply with changing regulations; and to optimise costs.

Read on to find out what Ecosystm Analysts Darian Bird and Matt Walker think will be the key trends in the telecom industry in 2022.

Earlier this month, I had the privilege of attending Oracle’s Executive Leadership Forum, to mark the launch of the Oracle Cloud Singapore Region. Oracle now has 34 cloud regions worldwide across 17 countries and intends to expand their footprint further to 44 regions by the end of 2022. They are clearly aiming for rapid expansion across the globe, leveraging their customers’ need to migrate to the cloud. The new Singapore region aims to support the growing demand for enterprise cloud services in Southeast Asia, as organisations continue to focus on business and digital transformation for recovery and future success.

Here are my key takeaways from the session:

#1 Enabling the Digital Futures

The theme for the session revolved around Digital Futures. Ecosystm research shows that 77% of enterprises in Southeast Asia are looking at technology to pivot, shift, change and adapt for the Digital Futures. Organisations are re-evaluating and accelerating the use of digital technology for back-end and customer workloads, as well as product development and innovation. Real-time data access lies at the backbone of these technologies. This means that Digital & IT Teams must build the right and scalable infrastructure to empower a digital, data-driven organisation. However, being truly data-driven requires seamless data access, irrespective of where they are generated or stored, to unlock the full value of the data and deliver the insights needed. Oracle Cloud is focused on empowering this data-led economy through data sovereignty, lower latency, and resiliency.

The Oracle Cloud Singapore Region brings to Southeast Asia an integrated suite of applications and the Oracle Cloud Infrastructure (OCI) platform that aims to help run native applications, migrate, and modernise them onto cloud. There has been a growing interest in hybrid cloud in the region, especially in large enterprises. Oracle’s offering will give companies the flexibility to run their workloads on their cloud and/or on premises. With the disruption that the pandemic has caused, it is likely that Oracle customers will increasingly use the local region for backup and recovery of their on-premises workloads.

#2 Partnering for Success

Oracle has a strong partner ecosystem of collaboration platforms, consulting and advisory firms and co-location providers, that will help them consolidate their global position. To begin with they rely on third-party co-location providers such as Equinix and Digital Realty for many of their data centres. While Oracle will clearly benefit from these partnerships, the benefit that they can bring to their partners is their ability to build a data fabric – the architecture and services. Organisations are looking to build a digital core and layer data and AI solutions on top of the core; Oracle’s ability to handle complex data structures will be important to their tech partners and their route to market.

#3 Customers Benefiting from Oracle’s Core Strengths

The session included some customer engagement stories, that highlight Oracle’s unique strengths in the enterprise market. One of Oracle’s key clients in the region, Beyonics – a precision manufacturing company for the Healthcare, Automotive and Technology sectors – spoke about how Oracle supported them in their migration and expansion of ERP platform from 7 to 22 modules onto the cloud. Hakan Yaren, CIO, APL Logistics says, “We have been hosting our data lake initiative on OCI and the data lake has helped us consolidate all these complex data points into one source of truth where we can further analyse it”.

In both cases what was highlighted was that Oracle provided the platform with the right capacity and capabilities for their business growth. This demonstrates the strength of Oracle’s enterprise capabilities. They are perhaps the only tech vendor that can support enterprises equally for their database, workloads, and hardware requirements. As organisations look to transform and innovate, they will benefit from the strength of these enterprise-wide capabilities that can address multiple pain points of their digital journeys.

#4 Getting Front and Centre of the Start-up Ecosystem

One of the most exciting announcements for me was Oracle’s focus on the start-up ecosystem. They make a start with a commitment to offer 100 start-ups in Singapore USD 30,000 each, in Oracle Cloud credits over the next two years. This is good news for the country’s strong start-up community. It will be good to see Oracle build further on this support so that start-ups can also benefit from Oracles’ enterprise offerings. This will be a win-win for Oracle. The companies they support could be “soonicorns” – the unicorns of tomorrow; and Oracle will get the opportunity to grow their accounts as these companies grow. Given the momentum of the data economy, these start-ups can benefit tremendously from the core differentiators that OCI can bring to their data fabric design. While this is a good start, Oracle should continue to engage with the start-up community – not just in Singapore but across Southeast Asia.

#5 Commitment to Sustainability at the Core of the Digital Futures

Another area where Oracle is aligning themselves to the future is in their commitment to sustainability. Earlier this year they pledged to power their global operations with 100% renewable energy by 2025, with goals set for clean cloud, hardware recycling, waste reduction and responsible sourcing. As Jacqueline Poh, Managing Director, EDB Singapore pointed out, sustainability can no longer be an afterthought and must form part of the core growth strategy. Oracle has aligned themselves to the SG Green Plan that aims to achieve sustainability targets under the UN’s 2030 Sustainable Development Agenda.

Cloud infrastructure is going to be pivotal in shaping the future of the Digital Economy; but the ability to keep sustainability at its core will become a key differentiator. To quote Sir David Attenborough from his speech at COP26, “In my lifetime, I’ve witnessed a terrible decline. In yours, you could and should witness a wonderful recovery”

Conclusion

Oracle operates in a hyper competitive world – AWS, Microsoft and Google have emerged as the major hyperscalers over the last few years. With their global expansion plans and targeted offerings to help enterprises achieve their transformation goals, Oracle is positioned well to claim a larger share of the cloud market. Their strength lies in the enterprise market, and their cloud offerings should see them firmly entrenched in that segment. I hope however, that they will keep an equal focus on their commitment to the start-up ecosystem. Most of today’s hyperscalers have been successful in building scale by deeply entrenching themselves in the core innovation ecosystem – building on the ‘possibilities’ of the future rather than just on the ‘financial returns’ today.

One of the biggest impacts of the pandemic has been the uptick in cloud adoption. Ecosystm research shows that more than half the organisations are either building cloud native applications or have a Cloud-First strategy. Cloud infrastructure, platforms and software became a key enabler of the business agility and innovation that organisations needed to survive and succeed.

However, as organisations look to become data-driven and digital, they will require seamless access to their data, irrespective of where they are generated (enterprise systems, IoT devices or AI solutions) and where they are stored (public cloud, Edge, on-premises or data centres) to unlock the full value of the data and deliver the insights needed. This will shape the Cloud and Data Centre ecosystem in 2022.

Read on to find out what Ecosystm Analysts, Claus Mortensen, Darian Bird, Peter Carr and Tim Sheedy think will be the leading Cloud & Data Centre trends in 2022.

Click here to download Ecosystm Predicts: The Top 5 Trends for Cloud & Data Centre in 2022 as PDF

Last week AWS announced their plans to invest USD 5.3 billion to launch new data centres in New Zealand’s Auckland region by 2024. Apart from New Zealand, AWS has recently added new regions in Beijing, Hong Kong, Mumbai, Ningxia, Seoul, Singapore, Sydney and Tokyo; and are set to expand into Indonesia, Israel, UAE and Spain.

In a bid to deliver secure and low latency data centre capabilities, the infrastructure hub will comprise three Availability Zones (AZ) and will be owned and operated by the local AWS entity in New Zealand. The new region will enable local businesses and government entities to run workloads and store data using their local data residency preferences.

It is estimated that the new cloud region will create nearly 1,000 jobs over the next 15 years. They will continue to train and upskill the local developers, students and next-gen leaders through the AWS re/Start, AWS Academy, and AWS Educate programs. To support the launch and build new businesses, the AWS Activate program will provide web-based trainings, cloud computing credits, and business mentorship.

New Zealand is becoming attractive to cloud and data centre providers. Last year, Microsoft had also announced their Azure data centre investments and skill development programs in New Zealand. To support the future of cloud services and to fulfil the progressive data centre demands, Datagrid and Meridian Energy partnered to build the country’s first hyperscale data centre, last year. Similarly, CDC Data Centres have plans to develop two new hyperscale data centres in Auckland.

An Opportunity for New Zealand to Punch Above its Weight as the New Data Economy Hub

“The flurry of data centre related activity in New Zealand is not just a reflection of the local opportunity given that the overall IT Market size of a sub-5 million population will always be modest, even if disproportionate. Trust, governance, transparency are hallmarks of the data centre business. Consider this – New Zealand ranks #1 on Ease of Doing Business rankings globally and #1 on the Corruptions Perception Index – not as a one-off but consistently over the years.

Layered on this is a highly innovative business environment, a cluster of high-quality data science skills and an immense appetite to overcome the tyranny of distance through a strong digital economy. New Zealand has the opportunity to become a Data Economy hub as geographic proximity will become less relevant in the new digital economy paradigm.

New Zealand is strategically located between Latin America and Asia, so could act as a data hub for both regions, leveraging undersea cables. The recently initiated and signed Digital Economy Partnership Agreement between Singapore and New Zealand – with Chile as the 3rd country – is a testimony to New Zealand’s ambitions to be at the core of a digital and data economy. The DEPA is a template other countries are likely to sign up to and should enhance New Zealand’s ability to be a trusted custodian of data.

Given the country’s excellent data governance practices, access to clean energy, conducive climate for data centres, plenty of land and an exceptional innovation mindset, this is an opportunity for global businesses to leverage New Zealand as a Data Economy hub.“

New Zealand’s Data Centre Market is Becoming Attractive

“The hyperscale cloud organisations investing in New Zealand-based data centres is both a great opportunity and a significant challenge for both local data centre providers and the local digital industry. With AWS and Microsoft making significant investments in the Auckland region the new facilities, will improve access to the extensive facilities provided by Azure and AWS with reduced latency.

To date, there have not been significant barriers for most non-government organisations to access any of the hyperscalers, with latency of trans-Tasman already reasonably low. However, large organisations, particularly government departments, concerned about data sovereignty are going to welcome this announcement.

With fibre to the premise available in significant parts of New Zealand, with cost-effective 1GB+ symmetrical services available, and hyperscalers on-shore, the pressure to grow New Zealand’s constrained skilled workforce can only increase. Skills development has to be a top priority for the country to take advantage of this infrastructure. While immigration can address part of the challenge, increasing the number of skilled citizens is really needed. It is good to see the commitment that AWS is making with the availability of training options. Now we need to encourage people to take advantage of these options!“

Top Cloud Providers Continue to Drive Data Centre Investment

“Capital investments in data centres have soared in recent quarters. For the webscale sector, spending on data centres and related network technology account for over 40% of total CapEx. The webscale sector’s big cloud providers have accounted for much of the recent CapEx surge. AWS, Google, and Microsoft have been building larger facilities, expanding existing campuses and clusters, and broadening their cloud region footprint into smaller markets. These three account for just under 60% of global webscale tech CapEx over the last four quarters. The facilities these webscale players are building can be immense.

The largest webscalers – Google, AWS, Facebook and Microsoft – clearly prefer to design and operate their own facilities. Each of them spends heavily on both external procurement and internal design for the technology that goes into their data centres. Custom silicon and the highest speed, most advanced optical interconnect solutions are key. As utility costs are a huge element of running a data centre, webscalers also seek out the lowest cost (and, increasingly, greenest) power solutions, often investing in new power sources directly. Webscalers aim to deploy facilities which are on the bleeding edge of technology.

An important part of the growth in cloud adoption is the construction of infrastructure closer to the end-user. AWS’s investment in New Zealand will benefit their positioning and should help deliver more responsive and resilient services to New Zealand’s enterprise market.“