In this Ecosystm Bytes, we focus on how the Insurance industry will look in the decade ahead.

The insurance industry is looking at full recovery in 2021, and it is expected to search for growth through the adoption of emerging technologies, new service models, better focus on customer experience, tailored products, process automation and Insuretech partnerships.

Ecosystm Predicts: The Top 5 FinTech Trends for 2021

We look at the key trends that are likely to impact the insurance industry, its market, customers and offerings in 2021. Want to know more? Create your free account on the Ecosystm platform to access The Top 5 FinTech Trends for 2021 from the Ecosystm Predicts Series.

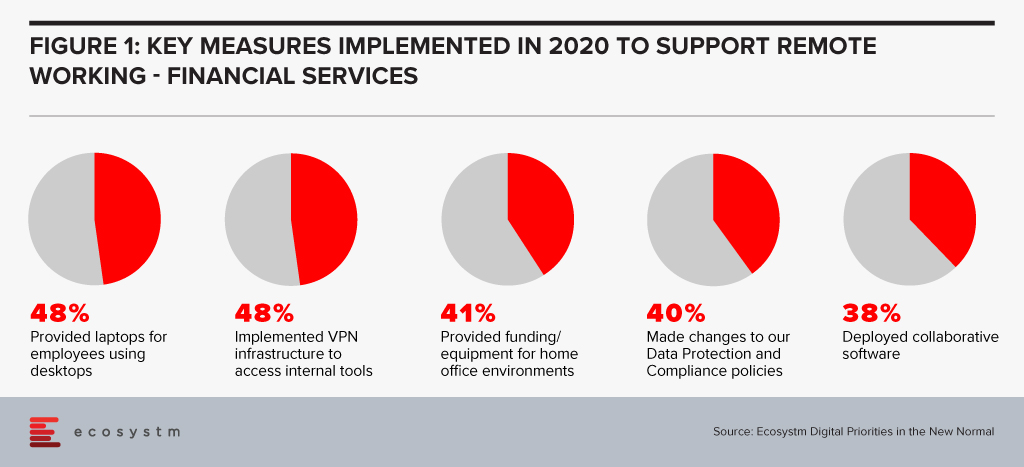

Financial services institutions made a fast switch to remote working when the pandemic forced widespread lockdowns across the globe. The adoption of remote working was nascent in the industry, and there was a need for a fast pivot by both the organisations and employees (Figure 1).

However, this has also exposed the industry to technology-related risks. Ecosystm Principal Advisor, Gerald Mackenzie says, “The move to a more virtualised working environment has been a trend taking shape for many years and like so many trends, it needed an impetus to make it a norm; in this case COVID-19.”

“Many, if not most, financial institutions have been shifting to more cloud-based and modularised Banking-as-a-Service (BaaS) models and these trends will only accelerate as we need to manage risks inherent in conducting financial services via remote working environments. For example, critical capabilities such as Advisor to Client communications need to be verifiable and auditable whether they are happening inside or outside of the office and I predict regulators will be pushing financial institutions to ensure these standards become the norm rather than the exception.”

Singapore Addresses Risk in the Financial Industry

To manage and mitigate risks that could emerge from the extensive remote working adoptions by FIs, The Monetary Authority of Singapore (MAS) and The Association of Banks in Singapore (ABS) jointly released a paper titled Risk Management and Operational Resilience in a Remote Working Environment. This is also in line with the previous collaboration between MAS and ABS in May 2020 to establish the Return to Onsite Operations Taskforce (ROOT). ROOT sought to strengthen and implement safe management and operational resilience measures as well as endorsement of industry best practices.

The paper seeks to create awareness amongst financial institutions on key remote working risks in the domains of technology, operations, security, fraud, staff misconduct, legal and regulatory risks. MAS encourages them to take pre-emptive measures to adopt good practices on managing risks.

Mackenzie adds, “Of course, some of the issues are difficult to solve. For example, staff accessing client data from their homes creates inherent vulnerabilities and the ways to ensure staff have suitable ‘in-home’ working environments to effectively manage these risks can be challenging and expensive. There are great opportunities for innovators to adapt solutions to solve these problems in what will undoubtedly be a growing investment area for many Financial Institutions.” The paper also examines various controls on the people and culture leveraging examples drawn from the experiences of ABS member banks to address evolving risks. For instance, FIs can implement security controls on staff infrastructure including their personal devices, verify in-person meetings against original documents, timely response strategies for recovery teams, legal risks and more.

To keep pace with the changing trends in technology deployment, risk management, and cybersecurity, MAS has been regularly working and engaging with experts to introduce guidelines, principles and best practices for financial institutions. In February, MAS issued a consultation paper proposing revisions to enhance the current requirements for enterprise risk management, investment risk management and public disclosure practices for insurers. Similarly, in January, MAS issued risk management best practice and standards to guide financial institutions in managing technology risk and maintain IT and cyber resilience.

Get insights on the technology areas in the Financial services industry that will see continued investments, as organisations get into the recovery phase.

The COVID-19 pandemic is debilitating industries, and economies around the world are facing the prospect of a recession. Malaysia, like many other countries, is focussing on front-line medical efforts and security services to save lives and contain the deadly, rapidly spreading virus. Essential services such as food, water and energy supply, Telecommunications, Banking, eCommerce and logistics are working overtime in this new order to support basic functions. The measures put in place to mitigate the spread of the virus are obviously inhibiting other economic activities.

Until enough people develop an immunity to the virus – either through a vaccine or naturally – it is hard to envisage lifting these movement control measures and return to a pre COVID-19 state. Malaysia has a total of 4,987 positive cases, the highest in Southeast Asia and a death toll of 82 as of today. The number of the population tested remains low at 81,730 as reported by the Ministry of Health, mainly due to limited testing resources.

The biggest challenge is that this epidemic is unprecedented, and it is unclear when we can put this situation behind us. The Malaysian Industry of Economic Research (MIER) has predicted about 2.4 million job losses as well as the GDP to reduce by 2.9 percent in 2020. Public debt rise coupled by reduced income due to lower crude oil, natural gas and palm oil prices and demand, will hit the Government coffers hard. Interest rates are expected to be low through the current lockdown stage right up to the recovery stage to help support the economic recovery.

Government Initiatives for the Economy

Like many countries, Malaysia has announced economic stimulus packages to ensure help for the poor and needy, that workers do not lose their jobs and that companies avoid bankruptcy – albeit with an inevitably reduced output – to keep the economy functioning. The stimulus offered is short-term covering a few months, and more assistance will be required should the epidemic linger and for the recovery period.

The Government announced a stimulus package on the 27th February worth RM20 billion (US$4.5 billion) and another one on the 27th March worth RM230 billion (US$52.6 billion). The packages comprise of direct fiscal injection of RM25 billion (US$5.7 billion) as well as loan deferments, one-off cash assistance, credit facilities and rebates. The focus of the stimulus packages is to assist people in the lower-income (B40) and mid-income (M40) groups, aid for employees in the private sector and for traders during the movement control order (MCO) which is to run until 14th April 2020.

An additional COVID-19 stimulus package worth RM10 billion (US$2.2 billion) was announced on the 6th April to address the challenges of the small and medium enterprises (SMEs) that employ two-thirds of the workforce and contribute to 40 percent of the GDP. The wage subsidy is to benefit 4.8 million workers earning less than RM4,000 (US$915) per month. In addition, SMEs will have access to interest free loans of RM200 million (US$45.7 million) from the National Entrepreneur Group Economic Fund and a further RM500 million (US$114.4 million) via Bank Simpanan Nasional. The Government allowed 750,000 SMEs to postpone income tax payment for three months from 1st April – companies in the tourism sector are allowed to postpone income tax for six months.

Impact on Industries

Banking & Financial Services. Banking institutions will support the Government’s stimulus initiatives by providing a six months’ loan repayment moratorium, corporate loan restructuring and conversion of credit card balance to long term loans. Banking and financial institutions are focussing on business continuity planning to ensure minimal disruption to their business and customer support. Many key business processes are now being put to test in-home working with scaled-down office operations. Digital Transformation (DX) has been accelerated as a result.

Contactless payments have seen a boost and many financial institutions have increased payment limits for such payments. Early last month the World Health Organisation (WHO) and the Bank of England had issued advisories against the use of banknotes, as it could increase the chances of the virus spread, instead recommending the use of contactless payment where possible. This might give a boost to the use of Cryptocurrency and cross-border payment services in Malaysia. In 2019, cryptocurrency start-ups received an estimated 12 percent of Fintech funding – but, only three cryptocurrency exchanges were given conditional approval by the Securities Commission. The current situation may well see that changing.

Insurance. The Prime Minister announced that the Insurance industry is to create a fund of RM8 million (US$1.8 million) to cover the cost of RM300 (US$68.6) per policyholder to undergo COVID-19 tests. In addition to this, insurance companies are to offer a 3-month suspension on premiums for policyholders whose income is affected by the pandemic.

Agriculture. Even prior to COVID-19, there has been a brewing narrative against globalisation, favouring a nationalistic emphasis as reflected globally by Brexit and the China-US trade wars tension. Food security is key, and COVID-19 has further highlighted its importance with priorities shifting to local requirements over exports. The Government intends to distribute a food security fund of RM1 billion (US$228.8 million) to increase the local production of farms, fisheries and livestock. According to the Department of Statistics, Malaysia’s food and beverage imports amounted to RM54 billion (US$12.3 billion) in 2018 while food exports stood at RM35 billion (US$8.0 billion) resulting in a trade deficit of RM18.8 billion (US$4.3 billion). As countries focus on internal supplies instead of exports in the current scenario, Malaysia needs to address this risk by producing more locally.

Impact on Industry Transformation

Amidst the gloomy outlook, there are plenty of opportunities, especially to the country’s Digital Economy. Malaysia has been committed to the Digital Economy vision with the Malaysia Digital Economy Corporation (MDEC) estimating that the country’s Digital Economy is worth US$3 trillion. The COVID-19 crisis may well be the key driver in achieving that vision. DX efforts are being accelerated with businesses adopting more cloud and mobility solutions. More workloads have to be digitalised and there is greater adoption of Cloud for storage and services. AWS, Microsoft Azure and Google Cloud will be beneficiaries in this area.

I have already spoken about the Financial Services industry – other industries are also getting transformed out of a necessity to survive this crisis. The Education sector has seen an increase in access to educational content and traffic to education portals and blogs. Some schools have implemented online lessons and group chats between teachers, students and parents to ensure education continues through this pandemic. Many universities have used their e-learning platforms to move lectures online.

The Telecommunications industry is being appreciated more than ever and it is the backbone to normal life, in both a social and business sense. The Government’s stimulus package includes offers of free internet to all customers until the MCO is over at RM600 million (US$137.3 million) and an investment of about RM400 million (US$91.5 million) to improve coverage and quality of service. Leading operators Maxis, Digi, Celcom and U Mobile have offered 1GB free data during the MCO period. The Axiata Group recently announced a cash fund of RM150 million (US$34.3 million) to assist micro-SMEs within the ecosystem providing eCommerce, digital payments and related services.

Video conferencing traffic is on the rise as it is the next best thing to face-to-face meetings. Microsoft Teams and Zoom have been the biggest winners so far. The home working trend should continue in the recovery stage and beyond, due to improvements in the telecommunications infrastructure and the impending rollout of 5G.

The eCommerce sector should see a major improvement in Malaysia with physical channels to the market being suspended. Malaysians have not embraced eCommerce like mature economies have, and it has significant room for improvement. Development of the SME sector and eCommerce are twin focus areas for the Digital Economy vision. Statista reports that the average Malaysian eCommerce shopper spent just US$159 on online consumer goods purchases in 2018, considerably lower than the global average of US$634. There is huge opportunity to provide for necessities such as online grocery, food and delivery of goods. As a consequence, the Transport & Logistics sector will have to adapt their business operations in order to ride this wave successfully.

Video streaming and gaming has also seen an increase in consumption in these times as they provide for entertainment for millions stuck at home. Netflix, YouTube, Microsoft Xbox and PlayStation are among the winners in this sector. YouTube provides for a primary news source and commentary on the epidemic for many. There provides a tremendous opportunity for both telecom operators and content providers to increase their number of services in this area.

Malaysia, like all other countries, will have to ride out this wave. It has made a positive step in the direction with the stimulus packages, especially for the SME sector. How well the country rides this wave out will depend on how targeted the future stimulus packages are and how fast industries can transform to handle the new world order that will emerge after the COVID-19 crisis.

The global insurance industry today faces several challenges – starting from the shift in the demographic patterns and the disease burden, to managing an ever-growing agent ecosystem, to responding to customer expectations. The advancement in technologies and their adoption is creating opportunities for insurance companies to modernise and reinvent themselves through new product and services offerings and by evolving their business models.

Drivers of Transformation in the Insurance Industry

- Global Competition. Over the last few years, leading insurance providers have been looking for a share of the global market and are no longer content with their traditional domestic markets. They especially want to get into markets where there are fewer players and/or larger population. The Indian insurance industry, for example, has seen a number of new private entrants over the last decade, attracted by the large population base and by a high percentage of young population. Many of the leading global insurance providers have partnered with Indian counterparts for a presence in the market. The story is similar in several emerging economies. While the presence of insurance providers is good for the future sustainability of a country, the market is extremely competitive. Investing in technology can be the key differentiator in capturing a larger share of the pie.

- Customer Expectations. Today’s customers are tech-savvy and expect a certain level of service and at their fingertips too. Moreover, easy access to the internet equips them to do basic research to evaluate their best options. The Fintech revolution also impacts the customer base, as they expect services such as instant approval and prefer to purchase items only when they require them. This ‘on-demand’ market has fueled the microinsurance industry and opened the gates for smaller providers.

- Regulatory Requirements. In the aftermath of the financial crisis of the previous decade and with new entrants in several countries, regulatory authorities are working on an overdrive to bring better accountability to the insurance market. Moreover, in most countries the regulations have incorporated market conduct guidelines aimed at consumer protection. Reporting, service level and fraud prevention requirements will see an increased uptake of technologies that can assist in fulfilling compliance requirements.

Key InsureTech Technologies

- IoT. The auto insurance companies were the first to leverage IoT and telematics to enhance navigation, safety and communication features that could help customise the premiums payable. The home insurance sector has already leveraged it using sensors and connectivity to assess and reduce risks to the properties they insure – large providers such as Allianz, Aviva and AXA have been working on their IoT ecosystem. This has immense potential for ‘usage-based’, personalised product and premium offerings in the health and life insurance industries (provided they work within the purview of compliance requirements). Ultimately sensors are not the most important technology in an IoT solution – the analytics solutions that can derive intelligence from the sensor data are. IoT+AI will give that much-needed edge to insurance companies.

- AI – Machine Learning. AI and machine learning make it possible for insurance companies to mine both structured and unstructured data. The use cases range from underwriting, claims management and personalised offerings through behavioural data and sentiment analysis. There are examples of early adopters in the auto industry – but again there are obvious and wider use cases, that can benefit risk modelling, pricing, customer acquisition, and agent and channel efficiency.

- AI – Virtual assistants/Chatbots. This falls right in with managing customer experiences. As customers expect more self-service (yes, the future will see less agents!) several insurance providers are using chatbots at several customer touchpoints, covering departments such as Sales and Claims. This will increasingly be the norm as smart phone (and app) penetration increases and the target base becomes younger. There are online-only insurance providers where clients interact with chatbots services and they are able to cater to a larger, untapped, mass market. There are more advanced adoption examples such as USAA’s use of intelligent personal assistant equipped with an NLP engine that have been trained with a deeper knowledge of policies. Virtual insurance agents will become more of a norm in the near future.

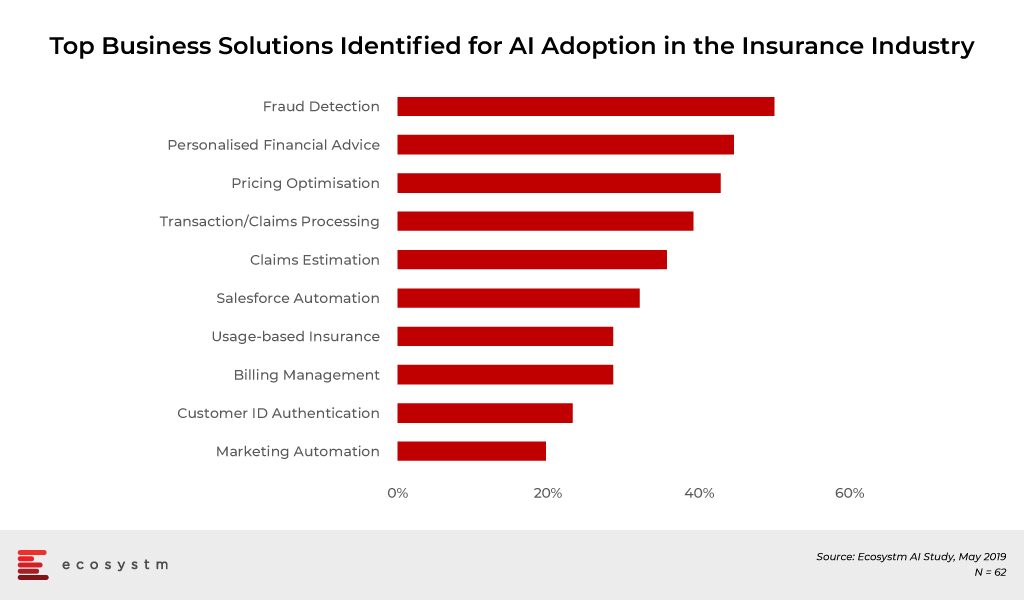

Which brings us to the important question on how insurance companies are planning to leverage InsureTech. Multiple stakeholders could benefit from InsureTech adoption. The Claims department appears to be a key stakeholder, focused both on fraud prevention and automation when it comes to transaction and processing. Sales and Customer Service appear to be next in line, where personalisation of product offerings would equip the teams better for a competitive market.

Challenges of AI Adoption in Insurance

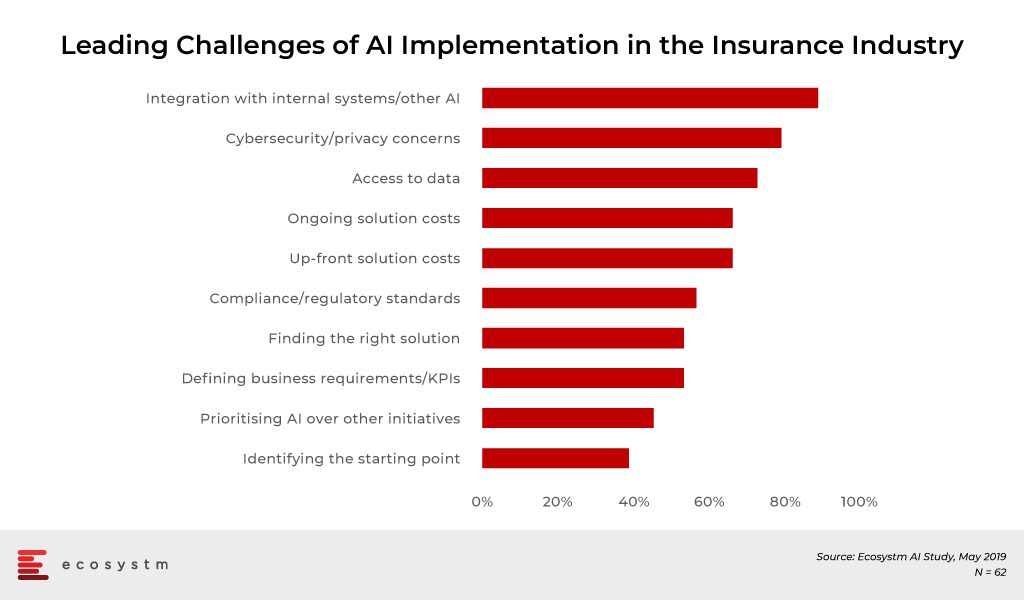

It is obvious that the insurance companies are still at a nascent stage of adoption of AI and InsureTech. While cybersecurity is a recurrent concern (as it should be), it is a common concern across any technology area. The biggest challenge that the insurance industry faces in adoption of AI and other data-driven technologies is the actual data management – from access to integration. The industry may be data-intensive, but the data exists in silos. In the end an InsureTech implementation should benefit multiple departments – Underwriting, Claims, Sales and so on.

Several insurance companies will look to consulting firms and systems integrators to create a roadmap to their transformation journey and enable the data integration – especially as technologies evolve and when internal IT lack the right skills to manage these projects.

The technology that will be the key component of InsureTech and transform the insurance industry is AI. In spite of the challenges of adoption, the industry will be forced to transform to survive in the highly competitive market. Companies in emerging economies will especially benefit from investing in AI – in fact, India and especially China will see a surge in InsureTech investments.