Earlier in the year, Microsoft unveiled its vision for Copilot, a digital companion that aims to provide a unified user experience across Bing, Edge, Microsoft 365, and Windows. This vision includes a consistent user experience. The rollout began with Windows in September and expanded to Microsoft 365 Copilot for enterprise customers this month.

Many organisations across Asia Pacific will soon face the question on whether to invest in Microsoft 365 Copilot – despite its current limitations in supporting all regional languages. Copilot is currently supported in English (US, GB, AU, CA, IN), Japanese, and Chinese Simplified. Microsoft plans to support more languages such as Arabic, Chinese Traditional, Korean and Thai over the first half of 2024. There are still several languages used across Asia Pacific that will not be supported until at least the second half of 2024 or later.

Access to Microsoft 365 Copilot comes with certain prerequisites. Organisations need to have either a Microsoft 365 E3 or E5 license and an Azure Active Directory account. F3 licenses do not currently have access to 365 Copilot. For E3 license holders the cost per user for adding Copilot would nearly double – so it is a significant extra spend and will need to deliver measurable and tangible benefits and a strong business case. It is doubtful whether most organisations will be able to justify this extra spend.

However, Copilot has the potential to significantly enhance the productivity of knowledge workers, saving them many hours each week, with hundreds of use cases already emerging for different industries and user profiles. Microsoft is offering a plethora of information on how to best adopt, deploy, and use Copilot. The key focus when building a business case should revolve around how knowledge workers will use this extra time.

Maximising Copilot Integration: Steps to Drive Adoption and Enhance Productivity

Identifying use cases, building the business proposal, and securing funding for Copilot is only half the battle. Driving the change and ensuring all relevant employees use the new processes will be significantly harder. Consider how employees currently use their productivity tools compared to 15 years ago, with many still relying on the same features and capabilities in their Office suites as they did in earlier versions. In cases where new features were embraced, it typically occurred because knowledge workers didn’t have to make any additional efforts to incorporate them, such as the auto-type ahead functions in email or the seamless integration of Teams calls.

The ability of your organisation to seamlessly integrate Copilot into daily workflows, optimising productivity and efficiency while harnessing AI-generated data and insights for decision-making will be of paramount importance. It will be equally important to be watchful to mitigate potential risks associated with an over-reliance on AI without sufficient oversight.

Implementing Copilot will require some essential steps:

- Training and onboarding. Provide comprehensive training to employees on how to use Copilot’s features within Microsoft 365 applications.

- Integration into daily tasks. Encourage employees to use Copilot for drafting emails, documents, and generating meeting notes to familiarise them with its capabilities.

- Customisation. Tailor Copilot’s settings and suggestions to align with company-specific needs and workflows.

- Automation. Create bots, templates, integrations, and other automation functions for multiple use cases. For example, when users first log onto their PC, they could get a summary of missed emails, chats – without the need to request it.

- Feedback loop. Implement a feedback mechanism to monitor how Copilot is used and to make adjustments based on user experiences.

- Evaluating effectiveness. Gauge how Copilot’s features are enhancing productivity regularly and adjust usage strategies accordingly. Focus on the increased productivity – what knowledge workers now achieve with the time made available by Copilot.

Changing the behaviours of knowledge workers can be challenging – particularly for basic processes that they have been using for years or even decades. Knowledge of use cases and opportunities for Copilot will not just filter across the organisation. Implementing formal training and educational programs and backing them up with refresher courses is important to ensure compliance and productivity gains.

I have spent many years analysing the mobile and end-user computing markets. Going all the way back to 1995 where I was part of a Desktop PC research team, to running the European wireless and mobile comms practice, to my time at 3 Mobile in Australia and many years after, helping clients with their end-user computing strategies. From the birth of mobile data services (GPRS, WAP, and so on to 3G, 4G and 5G), from simple phones to powerful foldable devices, from desktop computers to a complex array of mobile computing devices to meet the many and varied employee needs. I am always looking for the “next big thing” – and there have been some significant milestones – Palm devices, Blackberries, the iPhone, Android, foldables, wearables, smaller, thinner, faster, more powerful laptops.

But over the past few years, innovation in this space has tailed off. Outside of the foldable space (which is already four years old), the major benefits of new devices are faster processors, brighter screens, and better cameras. I review a lot of great computers too (like many of the recent Surface devices) – and while they are continuously improving, not much has got my clients or me “excited” over the past few years (outside of some of the very cool accessibility initiatives).

The Force of AI

But this is all about to change. Devices are going to get smarter based on their data ecosystem, the cloud, and AI-specific local processing power. To be honest, this has been happening for some time – but most of the “magic” has been invisible to us. It happened when cameras took multiple shots and selected the best one; it happened when pixels were sharpened and images got brighter, better, and more attractive; it happened when digital assistants were called upon to answer questions and provide context.

Microsoft, among others, are about to make AI smarts more front and centre of the experience – Windows Copilot will add a smart assistant that can not only advise but execute on advice. It will help employees improve their focus and productivity, summarise documents and long chat threads, select music, distribute content to the right audience, and find connections. Added to Microsoft 365 Copilot it will help knowledge workers spend less time searching and reading – and more time doing and improving.

The greater integration of public and personal data with “intent insights” will also play out on our mobile devices. We are likely to see the emergence of the much-promised “integrated app”– one that can take on many of the tasks that we currently undertake across multiple applications, mobile websites, and sometimes even multiple devices. This will initially be through the use of public LLMs like Bard and ChatGPT, but as more custom, private models emerge they will serve very specific functions.

Focused AI Chips will Drive New Device Wars

In parallel to these developments, we expect the emergence of very specific AI processors that are paired to very specific AI capabilities. As local processing power becomes a necessity for some AI algorithms, the broad CPUs – and even the AI-focused ones (like Google’s Tensor Processor) – will need to be complemented by specific chips that serve specific AI functions. These chips will perform the processing more efficiently – preserving the battery and improving the user experience.

While this will be a longer-term trend, it is likely to significantly change the game for what can be achieved locally on a device – enabling capabilities that are not in the realm of imagination today. They will also spur a new wave of device competition and innovation – with a greater desire to be on the “latest and greatest” devices than we see today!

So, while the levels of device innovation have flattened, AI-driven software and chipset innovation will see current and future devices enable new levels of employee productivity and consumer capability. The focus in 2023 and beyond needs to be less on the hardware announcements and more on the platforms and tools. End-user computing strategies need to be refreshed with a new perspective around intent and intelligence. The persona-based strategies of the past have to be changed in a world where form factors and processing power are less relevant than outcomes and insights.

Microsoft introduced a second Vertical Cloud offering, last week – this time turning the focus on Retail, after having launched Microsoft Cloud for Healthcare in October 2020.

The Microsoft Cloud for Retail aims to offer integrated and intelligent capabilities to retailers and brands to improve their end-to-end customer journey. It brings industry-specific capabilities to the Microsoft suite including Microsoft Azure, Microsoft Power Platform, Microsoft 365, and Microsoft Dynamics 365 – and is aimed at the growing need for “intelligent retail’. Microsoft’s partner ecosystem will also be involved in the new platform to address challenges in the sector and future proof the retail evolution.

In The Top 5 Retail & eCommerce Trends for 2021, Ecosystm notes that while retailers will focus on the shift in customer expectations, a mere focus on customer experience will not be enough this year. From the customer experience angle, they will strongly focus on omnichannel, catering to ‘glocal’ consumption, using location-based services, and improving both their onsite and online customer experience. They will also have to work on their supply chain and pricing capabilities, as distribution woes continue. These trends are seeing a deeper need for transformational technologies and leading cloud providers are introducing solutions targeted at the industry. Google has introduced its cloud retail solutions aiming to help retailers get more from data. Similarly, AWS has cloud offerings for the retail industry leveraging its retail domain experience and cloud deployment services.

Ecosystm Comments

“Global cloud vendors continue to “move up the stack” to provide more of the technology landscape for organisations. The focus of these tech giants is on adding unique value to customers by tailoring the combination of the different cloud services they can provide to specific industries. Providing the full-stack will mean higher customer retention rates – as the implementation time should be lower than traditional on-premises implementations. Microsoft has a diverse range of capabilities. Having a software company and implementation partner that can deliver the full stack of technology and business processes should improve the time to value for organisations.

But I see three key difficulties in implementing systems such as these:

- People adapting effectively to use the new processes

- Migrating enough high-quality data to leverage the new capabilities

- Integrating the new capabilities into an organisation’s existing landscape.

This is why it is likely that initial use will come from Microsoft’s existing Retail customers as they expand the range of services they use. New adopters of these Microsoft solutions will find that much of the complexity and cost of implementing a new business solution will remain.

However, these value-added cloud services open access to smaller organisations. If Microsoft is able to work with their partners to simplify the implementation of these capabilities, it will allow smaller organisations to access these complex capabilities affordably.“

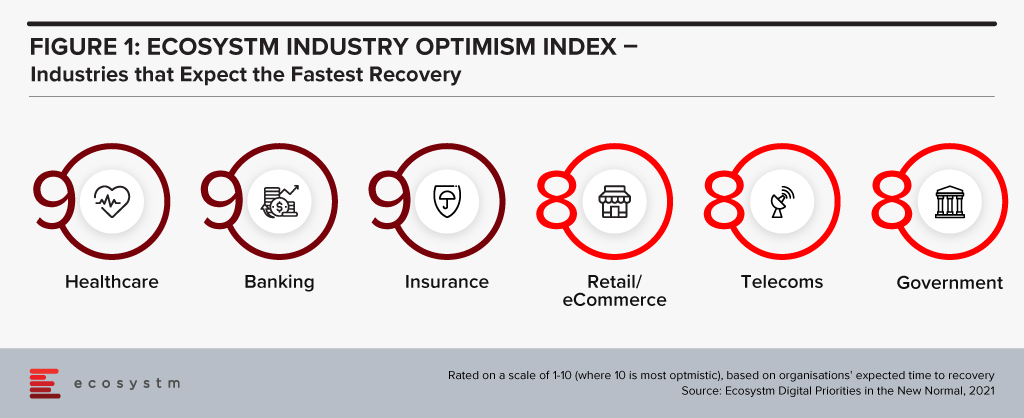

“The Ecosystm Digital Priorities in the New Normal Study aims to determine how optimistic industries are about successfully negotiating these uncertain times (Figure 1). The industries that are rated the most optimistic fall into two clear categories. In the first category, there are industries, such as Healthcare that had to transform urgently – mostly in an unplanned manner. This has led to a greater appetite for change and optimism in these industries. Then there are industries, such as Retail, that had some time to re-focus their technology roadmap when the crisis hit. These industries have a strong customer focus and had started their digital journeys before the pandemic.

Microsoft’s industry focus appears to be spot-on. Their first two vertical clouds target enterprises that have had to – and will continue to – pivot. The ‘modular’ approach taken in the Microsoft Cloud for Healthcare offering allows providers to choose the right capability for their organisation – whether it is workflow automation, patient engagement through virtual health, collaboration within care teams or better clinical and operational insights. As healthcare organisations across the world negotiate the challenges of mass vaccination, they may well find themselves leveraging these industry-specific capabilities as they revamp their workflows, processes, and data use.”

Get to know the right research, insights and technologies for you to be one step ahead in this new world of retail in our top 5 retail trends for 2021 that represent the most significant shifts in 2021